Marketing is key to reviving the fortunes of brands and retailers as they struggle with evolving consumer behavior shaped by the COVID-19 coronavirus pandemic. Image credit: McKinsey & Co.

Marketing is key to reviving the fortunes of brands and retailers as they struggle with evolving consumer behavior shaped by the COVID-19 coronavirus pandemic. Image credit: McKinsey & Co.

With government-induced pandemic lockdowns being lifted and businesses reopening, the expectation is that a return to normalcy is next. Not so, according to management consultancy McKinsey & Co. “During the months of lockdown and self-isolation, we have been, in fact, writing a new future,” McKinsey said in a newly released report titled “Reimagining marketing in the next normal.” This rethink on the consumer’s part will affect marketers as they try to build lasting relationships with their audience. “Granular monitoring of data and trends in consumer behavior has always been important to planning,” McKinsey said in the report. “Given the unprecedented nature of the pandemic and the profound changes it is causing, we believe that harnessing imagination may be just as critical. “Marketers will need to think hard – and differently – about what the consumer in the next normal will think, feel, say, and do.” McKinsey consultants Arun Arora, Peter Dahlström, Eric Hazan, Hamza Khan and Rock Khanna have observed six potentially key changes in consumer behavior in their joint report. Some are accelerations of existing trends and others are newly emerging. As McKinsey’s lays out the implications of these trends and what they mean for marketers and how they should respond, it offers a caveat: the list is not exhaustive, and nor is the duration of the changes. Shopping: Catching up to the great digital migration to expand digital borders Consumers jumped five years in the adoption of digital in only eight weeks of the hard lockdowns in most parts of the world. Indeed, many got online for the first time. In Latin America, 13 million consumers made their first ecommerce transaction, research showed. “Across all countries measured in our global consumer sentiment surveys, consumers are turning to digital and reduced-contact ways of accessing products and services,” McKinsey said. “As we look more granularly into the U.S., this digital trend is magnified for Gen Z, millennials and higher-income consumers in general. Social commerce is on the rise as well: 34 percent of people say they have shopped on Instagram based on an influencer recommendation. This shift is likely to stick, to a large extent simply because ecommerce is often more efficient, less expensive and safer for customers than shopping in physical stores, McKinsey said. Moreover, as social distancing and protective measures remain the norm, consumers shopping from their couches will seem even more convenient by comparison. McKinsey’s ongoing consumer sentiment surveys confirm that customers throughout the world intend to increase their share of online shopping across most categories. Net intent to shop in physical stores once the COVID-19 crisis abates has gone down 7 percent in both Italy and the United Kingdom and 8 percent in Spain, research showed. Not surprisingly, Amazon reported a 26 percent boom in sales in the first quarter of 2020 compared with the same period in 2019. “For marketers, this means rethinking how to connect with consumers,” the report said. “Clearly a stronger emphasis on ecommerce and digital channels is crucial, including consideration of the role of direct-to-consumer (D2C) ecommerce channels. “One European retailer built a functioning ecommerce platform in 13 weeks. This speed-to-market is one reason that digital has become such a crucial component of rapid revenue recovery for brands navigating an economic downturn.” But marketers will need to think through how to manage this new wave of data and how to use it to better personalize offers and messages to ever-narrower customer segments, McKinsey said. “Analytics will need to play a core role not only in tracking consumer preferences and behaviors at increasingly granular levels, but also in enabling rapid response to opportunities or threats,” the report said. “Existing analytics models may not be as accurate when predicting behaviors in the next normal, and they will need to be rapidly “trained” on how to best use new behavioral data. “This baseline of data can help brands expand the borders of digital into the physical world to create more convenient and useful shopping experiences wherever the consumer might be.” Another, potentially larger, implication for marketers will be the need to redesign shopper journeys for consumers who may be in a different state of mind, the report pointed out. “At home, shoppers are comfortable – they want to see loungewear options in their recommended products, they want to spend time browsing through add-ons,” McKinsey said. “Consumers seem to be in no rush – they can “add to cart,” then go back for more. They may be shopping at different hours during breaks from their remote-work schedule. They may be shopping for their whole family across multiple product categories.” E-services: New “service platforms” to help consumers take care of business In past years, McKinsey has observed varying degrees of e-service adoption. For example, banking has had relatively higher penetration, along with media and entertainment. But other services have been behind for reasons that range from limited options to suboptimal customer experience. During COVID-19, consumers are not only increasingly buying online, but they expect to perform other tasks and access services as well. McKinsey cited healthcare as a case in point. Telemedicine visits have rapidly increased, with, for example, those going to Teladoc Health, the multinational for-profit virtual healthcare company, reaching 1.7 million in the U.S. in the first quarter of this year, twice as high as in the third quarter of 2019.3 In the U.K., 38 percent of telemedicine users surveyed have started using the online service during the COVID-19 pandemic, data showed. “For marketers, this increasing consumer confidence in the use of e-services suggests a potential surge in demand and an opportunity to create new connections with people,” McKinsey said in the report. “One area of particular focus should be on developing partner ecosystems – both public and private. As services proliferate, it will be important for marketers to think through the role of their brands in interconnected service ‘platforms.’ “For example, food marketers can partner with e-health platforms or online fitness companies to cross-promote the benefits of each to a wider audience. “In another example, a ‘home-buyer platform’ could include real estate, mortgage, moving and bill-forwarding services tied into a single experience.” Home: Finding a spot in the new “command central” for all activities The crisis has made the home a multifunctional hub, a place where people live, work, learn, shop and play, the report pointed out. “This will be especially true as a growing number of global organizations and employees attempt to sustain some of the advantages of working remotely that they have now experienced,” the report said. “People in the next normal are also likely to continue devouring new home-entertainment options. Net consumer intent to spend on at-home entertainment has remained resilient in many countries, even when consumers cut back on other expenditures. “Our consumer-sentiment research shows that across Europe there has been a 10 percent increase in new users of online streaming and 13 percent in online gaming, with high intent to continue for both – 60 percent and 44 percent, respectively. “The popular video game Fortnite recently hosted a concert that was ‘attended’ by 12.3 million users.” For marketers, whether the at-home activity they cater to is digital or physical – for example, cooking at home has picked up as a family activity – they will need to engage with smart devices and interfaces across the home, McKinsey said. Issues to consider: How can brands seamlessly deliver a message to a customer’s phone, tablet and TV screens when he or she is using those devices simultaneously? How can brands market on Amazon’s Alexa or Google Home? How can marketers start two-way discussions versus one-way marketing with consumers in their homes, without coming across as intrusive? “Marketers will need to rethink their media mix across a larger set of channels, such as videoconferencing platforms, virtual reality, and – for the right segment – video games,” the report said. “The key issue for marketers in navigating this ‘homebody economy’ is in integrating it into the proliferating service and products anchored in the home. Doing so effectively will require an ecosystem mindset.”

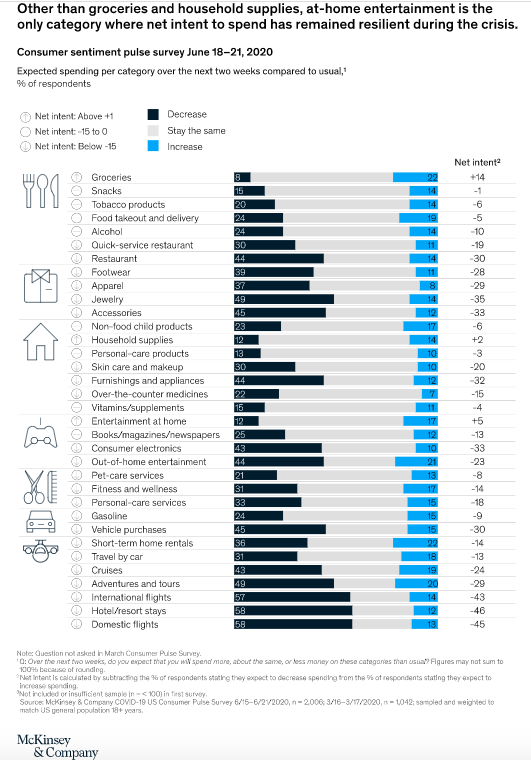

Groceries, household supplies and at-home entertainment are the only categories where net intent to spend has stayed resilient during the COVID-19 pandemic. Source: McKinsey & Co.

Groceries, household supplies and at-home entertainment are the only categories where net intent to spend has stayed resilient during the COVID-19 pandemic. Source: McKinsey & Co.

- How should the brand’s vision and strategy be adapted to emerging trends and customer demands?

- How well does the brand know its customers at a meaningful segment level?

- What analytics capabilities does the brand have to not only identify opportunities, but to act on them quickly?

- What kind of working relationships will the chief marketing officer (CMO) need to forge with the CEO, chief information officer (CIO), chief financial officer (CFO) and the rest of the C-suite so that reimagined marketing drives real growth for the business?

- How can personalization drive the next order of customer experience in an increasingly borderless environment (home, stores, local, global, services)?

- Which channels and messages are most effective in reaching and influencing consumers across their decision journey?

- How can prices, products, and services be customized to changing needs?

- How will the marketer’s organizational and operating model need to change to be quick and flexible enough to meet consumers where they are going to be?