By Ethan Chernofsky

Concerns abound about the demise of the mall, impending retail apocalypse and the factors driving these changes. From urbanization and ecommerce to a lack of innovation, there are numerous elements influencing the struggle.

Yet, while some tiers of malls are certainly in decline, this fate is not universal.

According to data from Cushman & Wakefield, the change is largely affecting weaker malls, while the strongest are actually getting stronger.

Cushman’s data shows that “trophy” malls and Class A malls increased sales per square foot by 16 percent and 9 percent, respectively, over the last three years.

On the other hand, Class B malls have seen per square foot sales drop 1 percent since 2016. However, if you exclude 18 centers that invested in significant upgrades, the overall decline would have been 7.8 percent.

Class C malls have seen a 13.7 percent decline.

In the words of Garrick Brown, vice president of retail intelligence at Cushman & Wakefield, “Bifurcation is real. Strong getting stronger. Weak getting weaker. Quality wins. If you are Class B, you need to become Class A. Reinvest, upgrade. Boost the experience and consumers will come. If you’re Class C, time to start thinking of radical redevelopment.”

And this is exactly the point.

We are not witnessing the end of the mall any more than the retail apocalypse heralded the end of in-store shopping.

Instead, we are experiencing a fundamental change in consumer behavior that will redefine retail’s winners and losers over the next few decades.

So how do you stay ahead? What are the tactics to truly understand consumer behavior to succeed in this period of change?

We dove into the data and consulted with industry experts to examine some of the key trends.

Upgrades and renovations

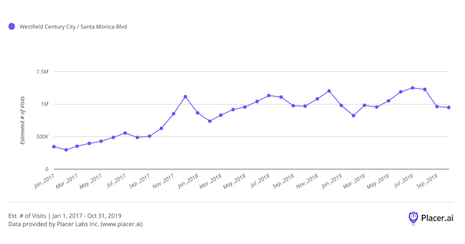

When discussing massive renovations, it is hard to find a better example than the Westfield Century City Mall in Los Angeles.

The mall went through a $1 billion makeover to help attract more visitors. And thus far, the return has looked incredible.

Since relaunching in September of 2017, the mall has seen nearly constant growth in visits.

Comparing visits from September 2017 to the year after in September 2018, the Westfield Century City saw a visit increase of 92.7 percent. And while this massive number is largely due to the launch and excitement surrounding, even in full tilt, the location has enjoyed growth.

Comparing July 2018 traffic to July 2019, there has been a 7.9 percent increase in visitors. This speaks to the quality of a renovation that not only drove immediate excitement but has been able to sustain interest over time.

Traffic patterns at the Westfield Century City Mall in Los Angeles since its renovation two years ago. Image credit: Placer.ai

Traffic patterns at the Westfield Century City Mall in Los Angeles since its renovation two years ago. Image credit: Placer.ai

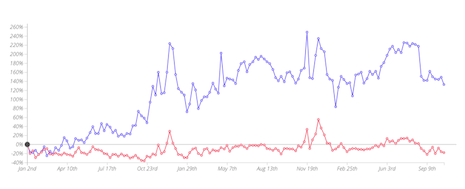

To put the move into context, we compared it to the nearby Beverly Center which went through its own $500 million renovation.

Comparing both locations to their relative baseline for the period beginning in January of 2017 through October 2019, we can see the impressive visit growth for the Westfield Century City.

Looking at their respective weekly peaks over the period, the Beverly Center had a massive 55.2 percent increase on its baseline for weekly traffic as a high point in December 2018.

Yet, the Westfield’s growth is so staggering that it shattered this mark with visits that rose 234.8 percent above its baseline for the same week.

Even more impressive, this was the second strongest week of the period, with Black Friday week driving an increase of 248.7 percent above the baseline.

To be clear, this is a comparison of two of the top shopping centers in the entire country.

Based on Placer rankings for the period, the Westfield Century City and Beverly Center are in the 99th and 94th percentile of all shopping centers in the United States based on their visits. And it was not just visits that spiked, but positive attention as well.

The renovation helped the Westfield Century City come in as the center with the top retail experience in the country, according to Chain Store Age.

According to Ben Witten, vice president at Trademark Property, there is a lot to learn from Westfield’s success at Century City.

“The Westfield renovation validates our assumption that people want to spend their free time in an environment that is activated, inviting and engaging,” Mr. Witten said.

“Successful projects are allocating more resources and spaces to chef-driven restaurants, hospitality amenities, entertainment and emerging retailers that resonate with today’s shopper,” he said.

In terms of measuring a shopping center’s relative performance, Mr. Witten said, “Sales productivity has historically been the primary indicator, but with the emergence of Big Data, we are adopting new ways to quantify and measure success on a relative basis. The implications for acquisitions, merchandising, and programming are profound.”

New tenants, big impact

The changes in the sector also bring up fundamental shifts in the types of tenants we would expect to find in a mall.

While department stores such as Macy’s and Sears have borne the brunt of store closings and changing retail behavior, the ideal replacements have been surprising. None more so than the rise of co-working spaces in malls.

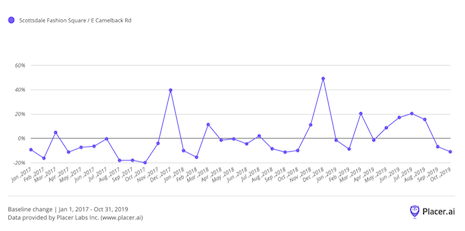

Industrious, a top player in the sector, has made this type of engagement a focus and it looks to be paying off.

The company has a location in the Scottsdale Fashion Square mall in Arizona, and since launching in February, there have been strong initial returns.

The five months since it launched have seen visits to the mall increase well above the baseline in each month except April, where Easter holidays limit the work month.

While there are certainly other factors contributing to overall foot traffic at this mall, the value of co-working tenants cannot be understated.

Foot traffic trends at the Scottsdale Fashion Square mall in Arizona. Image credit: Placer.ai

Foot traffic trends at the Scottsdale Fashion Square mall in Arizona. Image credit: Placer.ai

Co-working spaces do not just bring regular visitors who come a few times a month at best. These are individuals who are making the mall a central part of their lives, and this does not just boost traffic – it increases potential visitors to food establishments, retailers, pharmacies and more.

The unique promise of a co-working tenant is to leverage a space that is not your core retail asset – as they want a large and quiet area – and to use this to bring in a regular and ongoing audience.

Dan McCarthy, assistant professor of marketing at Emory University’s Goizueta School of Business, believes co-working spaces could mean even more.

“Co-working spaces aren’t just a boon for A Class malls,” Mr. McCarthy said. “They could be a significant source of foot traffic for B and C Class malls as well.

“As remote work is becoming more and more common, more people are working in areas with a lower cost of living, but lower traffic,” he said. “Co-working spaces could be a very attractive alternative to working from home for at least part of the day, especially for remote workers with families.

“Capitalizing on broader trends such as these will be essential for survival, particularly for C Class malls.”

Essentially, the combination of a rising demand for space from co-working and growing availability of space in malls could present a unique win-win.

Power of the mall

As mentioned above, there is a serious concern about wider macro trends impacting the viability of the mall.

However, there is still a huge opportunity in this retail channel, and as Cushman & Wakefield’s Mr. Brown noted, the strong are only becoming stronger.

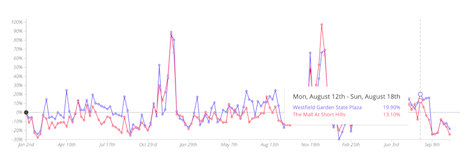

Two New Jersey based malls – the Westfield Garden State Plaza (in blue) and Mall at Short Hills (in red) – have shown steady traffic volumes from January 2017 through July 2019.

The graph below shows visits to each compared to their respective baseline for the period.

While they have seen year-over-year growth in some periods, and minor dips in others, the visits have kept coming for both locations.

The Mall at Short Hills ranks among the top 2 percent of shopping centers in the country, while the Westfield Garden State Plaza is in the top 1 percent.

Comparing traffic patterns between the Mall at Short Hills and the Westfield Garden State Plaza, both in New Jersey. Image credit: Placer.ai

Comparing traffic patterns between the Mall at Short Hills and the Westfield Garden State Plaza, both in New Jersey. Image credit: Placer.ai

Yet, the impact is much greater than just having large scale traffic. It is the type of experience into which a visitor is buying.

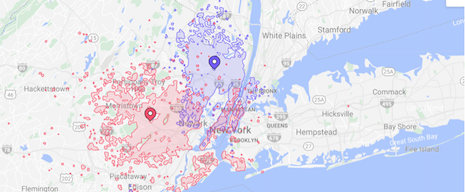

Around 30 percent of Westfield visitors travel more than 10 miles, while that number jumps upwards of 58 percent for the Mall at Short Hills. This is especially impressive when considering the malls have minimal overlap, even allowing for relatively close proximity.

The Mall at Short Hills and the Westfield Garden State Plaza, both in New Jersey, are in close proximity to each other. Image credit: Placer.ai

The Mall at Short Hills and the Westfield Garden State Plaza, both in New Jersey, are in close proximity to each other. Image credit: Placer.ai

And herein lies the potential of a well-devised mall.

Visitors willing to travel to come to either location is not just coming to hang out, they have a clear intent to shop, eat and enjoy their experience.

This is further emphasized by average visit durations for both locations of more than 90 minutes.The pull of such a location and the quality of the visitors it brings is a critical factor that will keep the top malls performing and growing.

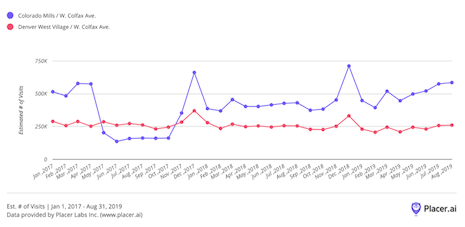

The draw of a strong mall can be so powerful that it can sustain interest even in incredibly difficult situations.

The Colorado Mills was forced to close in 2017 following a devastating hailstorm that had many questioning the move to reopen at all. Instead, a massive restoration project helped the shopping center rapidly return to form.

Looking at traffic below, compared with a nearby Denver West Village traffic, the site was able to quickly return to strong visit growth with new locations opening throughout 2018.

In an age of “mall demise,” such a rebound should be impossible, but the story speaks of the continued power of well-designed locations to drive value.

Comparing foot traffic between the Colorado Mills and the Denver West Village Malls, both in Colorado. Image credit: Placer.ai

Comparing foot traffic between the Colorado Mills and the Denver West Village Malls, both in Colorado. Image credit: Placer.ai

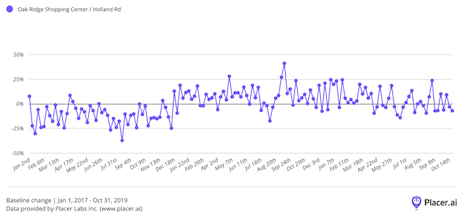

Tennessee also enjoyed a similar success with a massive development of the former Oak Ridge Mall into the Oak Ridge Shopping Center.

Since the sites relaunch in November of 2017, there has been consistent growth with 2019 visits growing quickly into the peak holiday season.

Foot traffic went up after a renovation turned the Oak Ridge Mall into the Oak Ridge Shopping Center in Tennessee. Image credit: Placer.ai

Foot traffic went up after a renovation turned the Oak Ridge Mall into the Oak Ridge Shopping Center in Tennessee. Image credit: Placer.ai

New data shows that this power is unlikely to dissipate.

According to a report from the International Council of Shopping Centers, 95 percent of Generation Z respondents said they visited a mall over a three-month period in 2018, vastly more than the 75 percent of millennials or 58 percent of Generation X respondents who felt similarly.

Key takeaways

The mall is not going anywhere. It just likely will not be everywhere as it was in the 1990s and early 2000s.

Instead, interest will likely center around those giants that are capable of creating a powerful, interesting and engaging experience.

From adding food and entertainment to introducing newer players such as co-working spaces, there is an evolving landscape that will help top locations improve on their existing strengths.

But what about the smaller players?

There are a variety of strategies that could help these locations grow and thrive, but they will center around similar principles: can an engaging experience be created surrounded by a wider environment that suits a location’s specific audience?

While the big players will consistently push for the massive audiences, there is tremendous room for more niche approaches.

One approach could be leveraging cross-shopping data to create a very cohesive and targeted shopping center around a single theme or type of shopper.

Others may focus on creating complementary experiences to nearby powerhouses.

Still others may look to more innovative and boundary-pushing types of tenants.

THE SUCCESS of the top class of shopping centers shows that there remains a strong appetite for top malls that can serve as a destination in and of themselves.

The question will be which approach do different owners and operators take, and how do they align their investments and execution accordingly.

Ethan Chernofsky is vice president of marketing at Placer.ai

Ethan Chernofsky is vice president of marketing at Placer.ai

Ethan Chernofsky is vice president of marketing at Placer.ai, Los Altos, CA.

{"ct":"TnGWXx4PTmEy+8Zn5epJD5LZRrW0ZLjBl1wGIt4viBHhMq0nGrx4EjvslSHRjpliFgWUwN2aHWm5fIdU70QG6CT8\/J79zLcBsYcQgNW0p3d3bSXY\/fxovIPV1mDnq4IkUE8toArvpvXVvSOfYoOavVpQ9xJQdx2dttAc2VVrnc6BWujHrUpcovZoErJcH3y2taEwugAYnn+sa2tRDaWYLd7ZaatY+c8Tt0eTGVRnjUX1EazNs\/NRjiiPma5gY4VXW97C3XE9DH7+AyjuryNQp4+2idpZniW4hvBYqpC0DXk3nQlKXyyCxkuwKaCtik7rFMaIq6nC09qzeFsdcwUDsHO0a+2is0jsXwcsqtxKi\/6us\/IZVBOFRvQS9d3NWIj5343GNGGQ5ajLne889owTBfV9XUEWkMHaH83s8a8f3lUm1NRjIMcoddK92DS\/G62BFPto7oCmpesE0BCmPNo3CPXXjKCugRksizT3vdfnm0xKCGQhw4R0OlL2Vqlz7Mtwc4DnqYwn56FgPHuIWOWaYCJSjpIRrXAYAQ+Xa1RQjzQZGudoBsKJQ2FHB88lSN1+KUjTFqln0Omdg8EWlsKZBd7JJ1j\/PX0N1BnJ4bcAeAPcAjz8w1hUb6+ivSwabmS3ocg0FDCgFXlDE7isNYHKEjO83rMZG4SD28pMmP3D4fswcT9BkunMuUVAIguVeW90vn6iCExN4kdGrUHqxQv8HkADU\/jkbmV5XPE41jAhC\/XOFcrRvfuaFy2mYjRne+JrLS0lhqaHrqDMZ7NIK4R6RG3bViGKbIwSFhdeR8A75EJfDfq0sWfuew0VyMTW1LKYrEFIEusOddGT8UFhlVpH4R0EHPc5V9wz9g4aFE9VVk9v7c7ETrUrVhCjfjRMKEL3nND9XQFbmCg6jVSNHX0M4mC7SQHfobPGy0cMS3BvmFIqzjr+MY6vPwTT2V8pz3+19Nw3Kp+4eBw4prZ5NCo1OwYjlx3Yn9691vgmOqOF7CHF7LkEb\/xF3FqD8NpIq0NQYeRKk\/pVljTOGso66gYmlEGcOjCAUme4pcO5NTvnLAVtcpEky10plDySUOaOs9k3mXHSZQEh3VE93bVBaID\/bDtkNyXwFUm2OqOWvbtbKir2scG9t7L3LVWaPXzqNFTtBrPfGDczpy0nx4e8ch1bLikuHCqrMM6+UCKzJfzbiVAQsdL5JUiY0P42f18WUAOAnpj4P08NoOmxm5+v\/YFsUNkm7WITGfE83E\/kEX4bsY3X\/mOtfF7MIYlpPTSehmTgSA1LWxMX0P\/D9orSakd4nd3vQElcXua4k2sjkUckYFP4RqXh1tsh+T5id8m\/Tp8D1yR6iIR68U9+11Ix9QOi1AxjvHYLgM3bGelvya+AsFl6JLO7DVonJnsvGuXFzL+Q2LBhxeYCPaMtzImzeBbp3pTTC4QJUbwzTYq87vJTlIBzO7+XjXVczScx0oo7QgDxcvgXOqQGpImpFUWNsUQhC09\/8kf0w9PHcSEilHCZHYh0DfrWs0qepqjiGY+qKhDUUqJ6HTQVqC\/T80Af9kaCWHGaymZatIFgWehYcXOYhPuOlMHlfrRIjaDA7QOxa67IiqKIJfO2qhaHNpg4iGbDMA5yyfBPpyn\/q3AvBR2kRaUw9UpQ1ujGlVGG6l+1z9qyXN3DrKf8FMnz3K\/rfe8i24t1LQnsT1ZtxbXJ0vHNx+ueZNHEowNubi1NVWUFhyQHC8MMDmfaRZbx401Va\/6jdCTnYxv2522c\/6io\/P0Ex9vSqceExbu8FJuKv3iZdHtZ2ItlbwVIdRGq1qzkIupCKnlqRjGNyGBz7M\/SLwv2tVwtq+EhDDSzURx05vft6FmbDOD9\/3NgwhxWEWEyLM3MXHnQTWPzaCCG3TR\/1TrYzPzclBxF2bxFW3q1fQtIhGMAhCVzJ8G4Ih4C+scJWCaZmhSCC0x1xdR9No5aaZmdyKA+GTujLI6jgsPNVIVY+ba2yer5AgCV8VzuBSnHDudnagzaLBXh\/VPcX0\/BnbP+pXAYgT+czc7AlTsZIIMhGlzfOEs8KNbWBWd9kURp8KLtkxWRVd+BerSbK5kjTegvugcY8+Lv3ArDtF7vSz4E4Mup5g3Wwghaw6u1PleP1\/P6CkL3O4+8jrUeTN2PPURoFKVwV0BF\/7thOKcM51mI9sm3UKODo4Kt+MwHhxbEhqRjorl2eHOfj\/ugCSijJT4lkMuW2e2eZvWOi6zfw0fqAN1qQv6OTR4HrEemAUpq1P+jqi6k4Es7cda1Nsv\/1i+xCTIpluDYgH8COMu2fSShP\/eHfMGtpulILZbgE75BG+7j2OyhZMlsvo7tQPp+tROIQoS0DM0iAxU0WC\/h\/aG2DJ8BXJpZnTwZJCP0ktBmP6+vJq96eCHZwDnsaXzJ\/eJCDtukRBPKN4mo+L78h0RU0ZybY58G\/OkDaBcVrAktqJGeXJeo9AzRtHYxX4jxwANd8D1OkduICCWqOSveEUf4Mcrm5shJRevwoxWPspX6UccXlGwx6DmydnSkmJGxhaaGjHe9f2xwxPPTifda1dhKbGikM\/z3wT9ClQg19BFDqkOh8ZwWTp7mnHt5D\/8RRgDoHbZ18Ycvi5ATwXSG6hAijhy1xRU53O5+Wuw6rOQMa\/e713QvkFxQ0EtTxZAcXFMwQpU1jePq9WrgtUZmbt3MLzBS1SUaGVQpwAtO+6Sd2DTpxNOGxarmYGiwUT2Me8rNvrFY2mxcg2IxLKFC9xCo0H4ca7FT2e6i37\/fzhz4ErKIp5\/m+wieU9ezBQIjAt84flgSd7H4LVrn9CXVHUsNN+8Ww6uidkOYDpxNgiFnsLD5qYFaRpJIUJJy9\/pg5GfujD5a9FYxhXHAIGUu8vVJd3PPfbgTltG7kQf7dNFw+KMnMZd\/M+8t+5adCRK4PybYjXiRgZMEqkNM1cnXCJtPqvwPFGeYVKtEBlmqkjgqOBPcwcbo5J6JIv0JnH5DYO4FngitgJheQrDjTaqD\/DJDssKr7adLtq7tu4I31YYuEwC+DoMeT6DZFA4wfSYD3uIz08\/snk45jwAKMtCXUtr6OJJ3T1Iq9R1TbQnryvm1b6gJQ6D1V5raFDLlMaN+IcpiHcFM311A+nD9\/YzdcF\/fHZfsswktfhAvuV2+Zwvmdjpja6gw\/YcUH8cdueNO4HOjFgCb2BnOgAR5MEscLIc21t5NBImi24BCMNv0vTnm5vgDeQTAoyebipuTmHufNN\/clkAhjt4qn5dF4cjKrgGpgBHUTTt6BHJv\/eL9kNQ7XeOZkqOuBidTP7X2p+VelIWqRuDYbCF8CabDvSGFLM6aaF3Bg7JWif\/PlRulUIqKqGxIv1HZ7xrHd+5Q\/1jROJuV5ENhtIKzeI4n7Ikpchs8Ie2ZlkwCrwNMW2eQqDCUqIscH6\/bqW12Svn9Gysv2BiRerFqmMGuiSii6UHSse41V3YC87wcUu6ZlpB3Mxi+JqUG0TWLLz3abWehpkjI+YbLgv1pcVW6zpbhEj0zHTaJ6yRZMfqRqlUsE6gnusMUcVa3nWM6hvqvNsk8l7f9xUmF9Tfid6iHvShN0JMNKBB97x9fxAAV\/tN955LCfMZxDfhlTvBuclICuMR3kTsKti\/eQSDUj7uY4h+9WrEkrnEl7VvIyeJkusfC3+oF9U+YapVgMZ58RUHpm226JrSkZb0GEfJj+SzktviCqXliQF1b+uaH49lXfBxtiU3JbT27zzPwGio4UNw5Zhrg6X6L4BCdmmZ9mKxnVGkndIPkAlaNAu+VM+2rYTWH6RftXr1E95c2qNHi2gE0vKVElGeMgCwD4IqX\/Tgm4\/A4ijXlPOQ6YwE96IjIaWGjtVp3Qu0rKBXwm0y\/GTNSdd1uiTD4lXfl+FIP3bEI0LO5\/QqstNW+iFpclFQD4CF\/qnI4irXh3ftz9YmWivVezQ9S4jdWTakQTD0IBGmMj3IX\/2soT2o4sg7sOQD46GQD5itZcwSODuVK941Vdc1qqjjL4CKQ2dNgaRrVGrt5ntfJIGKAedKhbdM4hm3f58QPB2y1a0NQcUSa6m4Y8rf5QjURoJOLCWdcJB1HmkWu+ZtCh8M8Ri+8NyqE1WsLdyVTXGneIPg5wH0RSmigCDPLzayUkEh0N31PGtfTTCuTeYSG7SYZv3vothtZGRqUjl8SGqJqMKJMIIHxolNpZaghkEr1KDUFXrItgN\/CfanGyk8yekjKuuOq3UCd3nd+WcfqiYslE5Ans7Q96aoRpX34ix\/8xVIzUGpibph9M2OSBU9GYNh2LYwn0kU\/mZZppYQh+A1TE2w8EAJnDSTQraWSaGHES4rm8CQA7b4LEdhv5ffQmXzT1wDC+XjVbwjdI6gZsVCkb5YfXl5htj4Rg+ZOGaQyJUhCQACHIXqv6syOgG4U0WLSArUsMUGfhKMRqJ9\/DyiYB60iutzmzXCNkjkWp2oWBYkkpC901Mz0iTpDp5IGJEP83UkH3XJTu7PDHEIm4Y3Nh3eMqFMpTNGkPVTEOVCKSfHcvF9Z3UREP49MSTIZTH8VGEBNvYK+Wf6ECI\/YGUtchc5Xc71pUgosW8C7CHE6bEw3MQRADnKMpI1pJgYiPL+XkARXpPewxvRZ6Y4gSStrilH28Kmwv29bZtDRwke\/RWspY8LMSI\/DOQxm0cpsLKWmJg2iQpnaOg9hUbwaM1833VpE1Nf2ms6w+iNggc0Dw3LSDfRkXIDhWjn6jrF8CUvjD0Sb6bsSC+dDDxpsQ7qn\/700zOItQvuOsjlyI4wlFcsVEyxpZpD42k03W3QjHQP6ANIUaMHovIj69zvWCr46xKYYVCbvJDanpWgf0Yb7GlGrMCatTq2VN\/htRQfZvnFDgqXWk2NwSApPvfnqdUzNj7xRhC6RJXb9MQasu5a9IUx\/lHn80A80Dka43zLAzJblrmpmxp4\/zl75\/med9un8cq6Xpz9migm10zYJBEplW1HMuCXXKHnqEioJRDqu8goJPC5\/eBTIIr1rcHnEWp8b6tLb+iRZcB5cT3exZ54t8stccQym7Oa231m12zKP+sujrK3CFkzRzF9ztmxQ2\/rs7t+aB\/NnyeCOdslJSfxpc06+nLczEVvRg2KXkhwa\/eUWA168hU2tCw+Gv3ERUDvbu+7dmZJJBlU4k41gdiT8OAgh\/WfJYAXdkUye4zPXHKLm3ryODCYEmrzO1iZ25UE8EBcb63HKgv4Rqc\/7LgH4yi455hqQjTxqaOxkX+cdZsnFjMPFj+gV+5X+joHeY9RuRiAF5dDYo5jrb\/btJQZP+4TxJE74JbHgXZ9hMuirxHqkRIrkRQOMVBkTOYjuJa7fRoWyasOyeqvDoCqqvP32FVqhf4vnc0mc7x2mdznmg4QflPLSPNLFeC5V7B6FXCcjYbQ0wlV2bEPZQDzEZELvkb3Zh3VuXxUjlPnHj76dr2Cz0zjbi6i3fmCRWMLEluHWHVKXrmIZHpweJWKuvlK5Mbi8RQQqy3\/l3AoEhu9l2aOE5XYXDLAONzt4cbpc6CihGIM366K+9kcxFLNA1zuCXHPYcQ7AVRzLVlCUXrkwOB8onDf5AcQpFgKutiXc81OyU4787epU0VP23WdCMPE9LaKCe0qgk\/HD5S0hEfdVztVOAzIE6tHHuQ3u2pSULD1z98zKU3igwbyydOWrALWuFV4P6qlgh+\/dHXCpCD+3QOPBSfXmawsrwxBH0ogJFZZdvmzo3YLl3M2a1NtdRypBGmYCMa4a+KMjFUlBTxGbAfqaXuLo1MwD\/ok1Yy3CDtVyHD3yAi5Ul7JKl7RKajMRJA8v99Mc4irIxnrNf2cMXtKPLWFy8wzIZt4o1hM5tzN0OvbkE6s4g6xSSY3\/UX7c\/6X7WGpSOvHOxh1veTML7tf3oLegxgcaImwc01DuCKrtB4\/OyxoIgCA+0yoOjdb40tX0ucmH6KyjR2atoErox9ghDDsFQA5xnk7pPjvxaKqA\/SXZUCxFNGRKPCGQmLwLgangEvYsLL761YIjpTj474wzGj8ivsEnav7Ne2SYIyAGz59fs9Z4gcZGtkAL0GVEn7CfCdIAWECvRuUFFJ4wff5K\/qrHOTWoPkpEaNLPtrXKbRmCdceZd0\/xuk3jijXOiufMHq7LmPGXATk17C8lDAyEHIl1CSf0pdVOcrYL0VRsQOvKIlZSMY0S6z1oxIuY5SZ94qHOlQjadCV3q3sXBPOLP4tr8cdyxFpyakTkT4qKPx+CH1IyQ11yJj65nJK5lUXIlhZdczgM0qSkKxCUw1V0K\/c+YvNEockxi\/T6S1tzeaEUe6st9U7np8YKcnrecR1rPrQNiLOEKqxjraZkL\/fxoxH\/0t5vpzqjoJ8wpqzKocwMJWMQMxdQTOYTlBfAzKQOxjYdVRixy2w2KuTzibTfoxoqBfFLBhWkX4GDCQ2QO5qdKCI8NKeZnC351npp7gxFxslXWN5oa7bmLA3+IlCLV7Xm0p1fZqzkBZIbG8Q82HyFDc7eNKhpd8yXwBz5y\/Dfkhv1NSjOqIPuV7cA5fbm42NhiVTnTmyEFqeVPDSzEUWUlARCC8p7fxxQvYAPnwgBxHi8Mbx62SeyGJTIpBXLn4nvkGr0bjeKaIakw9iPLYvqCWLfDUli+HoHVHvq5UUB3\/S\/J+zYwlZ0sbi6bsC0gd\/FcM1\/Fu\/DTZ+JOrnHG8iYxCfr1hPtsTQSDzAzTIHX34OSLZ0DCJlDfW4zlnwOtMQPQUPCaq1Jqum9Qwfx1Q6NROxxJyWJSrWa38QGaGt7K7JBDg7\/G1wtXE5Ag0CGQxGdAQXgQ1EDvh2szIYYb86hWd2vkt5SYqceD35DBYBrjoIzb4gcBME018oDB9a3s\/3SRNwaHT5mPYxavps0pkmA51DlrcOsYuvUr9UWT2deQKS\/wdH96FxTi+AypfPB0UWVGkjIZYsG5+vvBj7HP+\/KbL1a1FOmma4q5IN9l2RRAbTM\/m\/0guUM71jSubXF8drnOZOjlU9KNxrdmlcV\/oSl7RC2gTTNF613RNKmwPiOsVCe\/ekqy7aeke7FJJ7oVqSjD5qGTCWIZvCRXjTUDa8QJvuK8pt+k43U5wbnk6drJ3M84pUxy52TzxdXCsIOjKYeUyYza+xTNdy1SQyTX3ZVDW2ZUX+uJYIm5dfFFOMg3voOCbiRVKvg1wHkSDwAsW3Vp3WAsLMrqCFREqU2bnu4DMTRfGJP458V2eK6nQp4V\/r9fZzC0qYhudqYJX5Htc2OrPvWi70pfLNPhiNJYDfef\/9R4PuWoVLu2pkt9wGLExmflmOCWFmZXCj2F2KaN+INx0sNE1H3b30MNnHgvYkfBNKItWJS+86h7+16yaWtiS\/3E2EdH6guNcbS\/a0hclC4XNy6vKHvk5juBlt+U\/0TtIcogY3NoCq3mafF3GlOulG5CA+OobrdWGfoddpRlufm5ENSGy0tfBwre0ff1Ai77u5YY7B+TvUSOtDvUKa+pNDEOVEc3EQ2i7GnXW2Lq5vdPpThFFDO4hHR48xRO70nPSWgtId3j7QjrzUL8Tjv+7y\/fsBWY\/AG67JrzPCXd1yvgUTDoEu+ZYQ\/6u3o0S+dpwHqvjjrJ3FmVZ1WlUpHZ0Mj5fYvlgeoHjMTsClGhIEfEPoDooJhbtTWmdM+QMdWrN0JTXhOXFUfb8Tzw7l1rcF98vJryAc07GAtrjXqxlFLK7K3XYukgFZY1OGKzMpCqyQtymJRFCAiWKpDRbDDRKlbSXYy9C4K\/3k9X1hp14msLkZW4raOYLJRcuzDP9K1tz73W5RagMDz+jPuDtN9\/WR7uLvE909YhOOejMp1saoNAsP9BtAjFAUYREtZYyKUeIsYwD7\/OlngO+gi2vwJB8hXS0GqHcvguj1P0\/5bY8q3amFlHSQq847bXKkY5O2W7yY\/TNVcfa+F3\/h0NFRlR3EnNYx3amgwMmmoRWOzo9FLAHflzMMMdTZ\/+0ddRntG2kKZ7JRk8waqi9F67d+nojm\/1BQf+nQxW4MR7eKCO4CJdE5zVKNhR8TVBJzeOLh+nBsgJdQ5jWyawoGKg7Y3yoK8SLLdf8IMJwSB\/Q0cE15rjNzIpV3QIAKkp72ahypcP7wcbZWcs0H6i9NKKJN0X9lEBfrOUSeaKg9cFb2\/10fyH0F1d1S0Wg2NO+fCX\/dNnRbF6HUKaOsFdp8byQwnBSk12ypso9uGDQv38Vhc3nxA7UsoehH5hHD\/OopA3gZxUo6MxTDAyTsB67ftF8z4TNHZFq0L\/r\/pgLD2GNzpvxJ6IKiQ\/d9vPfKpdWLfxWU6HI66+n0rXDG3+ioQQefrxIcIIpg9d3vtN2cUEXZFOTnUtAXeYDq2gZrL\/BVK1UlvnfQT7jL8T0+1KAhwAC5yWD02z4i+Idlhq7gK3\/y+kF0nFCFeBCiCJfO2jAplRkTr2La1fH2i7dIw+61GWjQ8MSc8+GjGaK16Dc8tSyqOn7Lc9FXFIGeAxz8ZWBVeCkpwH0uvIHTCGsr8igQMAsVmP6owfD6TNzj7s2FNOfxynJRe70M1WtrgzYwhDVipQPCUon0dkSindYzhtvA3s0a6WYCqoJNMg4x7jAbfXW01k9lH3Nj0mc5bCOlp7DhhqdBEFRLqiwdxsnzukKz9FDVloil9L50NT6B05HVduMdQ+WCfoWS1zlJalpp5VZ0IEv7wUviqIw\/rcpoibktWTLmN9SPUsd44W4\/XUCc8v9697UzqbIVcOiA5YKfg4Z4rjtk0lTM+Gwmx1eNJ5YAG3My\/Nbdv+E+8Pi5yMDJpZaOglCWq4f93DbyLoItJOmEYTzMU\/IrFQ7I3xX\/yD\/detPIm3QFG6r\/du9FM3icTgIkZcY\/fBbeg5K9OjmAw2Sk3MuiczJb3pADIllhyVj0DhAVj2XveMS6Q\/eCcYHoTRdNVs6lsq11gR\/cz5ESfk8CRsRxAt6bO6\/2l5CGiU5pgIYIK+\/WjTXo3MmpbLu0mNZjojfk\/7MnDcdJ159WTZsUtlLRXKt6nlXH8ackoddA1GG3jEPZFnZt1YoZcUC0WeCNjXltav4cs2\/vV32lDsifNsCmBwPGnpq8faCJimFycWDwyAuOPH3+qur1tVArOerkgAyd4E9d\/RpemqTl1\/PKZnpcwCB9JcapLSjqLqpP44ftMLxOJpoUWqNRh\/7mQMG6wM4fOduDHf0AimuafWb7Y4nG\/WWIO6bfqI5l1u3fn1Z6YRfBzbztXcD21QAYs44GRWbwvM7EDs33T71vPaWGsyVklKUl31pn5B1Md9jC5FMS\/ftfxrSTT5cOW3\/YQVSdjg3wtic62THnxQDWoNSRWbE2AaAQydpUz2JVjkD\/j5d9DT\/AfhNL+oWvRutnABA\/2Yi7kTm4F69eyHwW4gCUSSMbpFQUSS5Hp4rNkDGtCqZD70EyzaG\/zRh+avEiplRSvYq+qlD3be8Ew3pYJ2pQSH+Kd5+TAZizwJvGoycEvAmCyjq\/l+V5w3YQMbWDcc7DtIpUq2EAq3WJ+9xrtrFIZ1Gzdp08sk7YOFGisyVQxQYXJr3OB\/1fE3zKy7fo8VDxDBL7+VgR1WZVItHO7hEsaLIa3rONnW1GurTbgI6ibGJlyKjv+JB7\/0CRj4gtF0xTd3b6ik65KeRvLjfupiIC9LM3XxWGpiAyukzrYUEx+lVt0S8fmJFFaQwFHfgFLBxLw4A\/QnGU6GkeZaB\/J0lfaW9ad+K6+XokgKybt7D1f59c2JrvpOzRXLWaOzWw9bmtBzKjBxz8dcdd\/p9VZdtbZ\/GtEqyJVUT+crw1fnp29IgtfQrzECv75WzsGvT8iBNW4P+Ba5kMRHKSQGTM9Ey2xbdgCztU\/IsuW0+DIxX3a8E9UFbGxulzkSB56mM1uBL\/l3YUOwyS9aCaC1Z7xn8AZVWTZzzyU\/6rCKCrHDlGicQcRmiJVT73Ix\/RDdZ2lVGsvVKMkKR\/\/DwB\/5fhtEGJaaUtf5pYWQKgEKucazp9e2GMvnf+oPBdlmwCj7xdjTiglJFa2ANVboY4LYkHjYws7KC+b9Otpxjtx7mgsJNeYYqjk2BxfuXGLB6EtEdvNl10A8XGGVmZIEsNTYGHAyjRiAxcZ6vsmG3dBQuI08I5MtSKYP7+dI2O22T0bdNakpeaVHG48OqLnJ7h+9xoaQrordc3JnWrfGsV1spXTPzi3EsN0TdAxJhgmw1qSF8LzpsdoC1JrCgfI\/tJvCR40lg83TuR+mggPyaJ0jksAUs4LovGE6wtroSn5zgZ\/Ccj+cO8qAd+o\/FjDIROAGuHjKQUbc6tu+C+PVbNaxtGeQii7GpHWcdIRk+vwrb4joQshh+qTmygaPvHCD+TxRceWoXElsdnvkMEKusRmUsPMqyN3Qz2JeMhg8WxeIepQL02I6jf8vN4zdVEtC+GWOUNc7X9PuVE\/WVLVFrCSMGl36vjbBxEzdRlTVZCzem3srqxpk5lqXm9XQ\/Pe\/DefSLETTIePcU2Y1Silxu1e7ThqFV3rCfD61h4k9dZzJqnTHz1X+3VjVhbAdAMOXnHN1pqYQTx1fl10dNf1Lvf8bs8hZ5gojJmyVlDuxV+5oLBBoliEvIzctZN0\/jGFwM\/SMMMWRIJi75KNtne5Yy0rarUKIzCfvI8Jg1VB154dZUhwspSVY4gazrYEYah2syxqYzZ1P8q+YUkcXW23y6eTA8QMdRMQ\/A+ruZUUKBKbPh+iztPGnYQWKIpc6ogzo1rrN\/yOwoC63utCXIw9kbPU9JnU2UMc0VcRQ2932KOwLsANMmCB6K\/FU1m3oZF9hfbM1oy9i3Re3hjYcbqS35nc7H5DUEpc6b2PWYc1fSbtk23jOvEVTdE5fxafibJopb0IlRwAOE5tgzY9Q7bAKqjMyK40IuvANvaRYjIS4a8lt2GrcplivOnUR6+jd0V4MZrjeDTWQFGoZjAN4mhk+A8Qxojtmmb5hwtrLNWEtNbgsMTRJw+WHTkJeMmFfxtQiP\/rksq78XEdpDjtk45ktQSjaQkw6APMJA7H+hdfP4ljsImcN781DVErK8vwRsnJ2mdRw4CZcHvHl4jBTneFCLYyuOOAA8ALG+SU+XKas5q+YhLPi7BvRJDfXcNbZBFqsD7UDEFVeKM7vHOmYExMqbUpmluOTc+LTZic63gtn7TevuPdjoGBUGOTDd40+a3amKmfKgj4hTVi9MzkUscL7K6ou69Zr3cbmvKGCG+RVeuF5z+ZRqt0YDaO7clA7cQLAQHmOOHQNbagDI67bfr6rTCLY5aYny8TWjZFhA8NWLP9zZrWpj+bB9Ccjl1CwW0FdZQKQL1FxUmhPSeqJXP0AoRRylX72V5E7c2Q6uzLN+fzcUlkvDlZ6+d0SY36W\/XtqPspUyG5vIj1W7+Wt5zNCunTPlkGbdy84O1Qui+REuFUKwoymmqr74+M0L75hdJZrX70h6PvxHGoGNZSGWcdoZViwQ9VFlAGFj12f\/4Yx352LW3kroRWCfu+UXMYCSTQi6Hku3ZZaNaq3K2sTiyQsqsKGLBcem6bYelAP7Ag2SM3tQGEZc2J45O1HGop0l3Dv46S7mRpMCPTZE4TJGvpCThi\/wvTAyzRorFTw+DMLl\/0rcq6gJUAvosPB\/nSg9OfXpbkvt97l6ma2SUVulbmI4Tt+BS+x+ovRlrgnlSUV9HB05Qufd+Lphf0bpANZRAwMJxCGg9c5hbKRftBhoA3xv\/vBLxHSoUQ1e\/ygD3NEC9AQVAPQqyB939i5yxypYwhXHCOFKFXKLc2zVpqqGNpXZq\/M3SGeBzwZoAxmVKyYJcHfJ0MwFHXLc2AabmrQkmEjGGx+cOKg8Av7HHZl8RFXJWuQx2VP4p1P2n5mjLkdmWWBQal5AoTXeZLZkZQLDi9TiMBRCVKPa4nF\/Jh67A3RWEUMGhAMYa9bvmFqkIwlBExjbT976jdTq4w6LoVCqrrD2614sINV\/2zgC2hQPN013efEZoFozQ+h4xPNp5HVopUfZSJE4a1uWtvssHFbIZcUgEf4E2cGWashPQfwqh094tpuVszGIQFXKyV032GVszHUgJqnnR6irjk0HYrggwYkhEcCHRBIu54W8AaePI+Et05JS1y9N2ygWcr\/clo8bPfZy4qRT1YGzIgIW0YnturtvisV3EOAB72uwFtJWgby\/iPkBd9MMxF+tpTRE8FDqiXjeqn60EIreUSqE2mN+6DZeFP2CsS19iTK3z6O3KCf3ikK7Jdy9J0bvTAUq+ou6xwQ0LS\/nx8LOfRDsidHAGqd5c6WHD9yWs4bE7OIDIJJ1RqoJrSeFTiHnhJXuKZZAUXuawglWYYNWI17qNqC+3ikL75NSMVP2c49O5OeTFdg68TAsJbjwgMgDbCxg2kMP9xOdDoY153JQcyhm2\/+btVaqk5+fwxZg0scCuv\/\/LgMROcCcn4v584y7IgHqOQ920PsJixoGlWdRyy+dNIUeE0vrbrWfsnQoG79M7mSSfB0U1SYDxfDsFSB6NIa9MqW+FhFM6BQk7YG+c2ScAjNKWsx0XKq5AA8jet3DhFR0oieH2TTAGtGs3aXeK5vFsUPwv8OqwA7Rldi06kZggNEJnMiMJr36++I6ZI+qGfnwfFl0WxfwzW7hbFfX8f1O4dlkHgAbrfhztgAceOMgvrxA\/qjcQ5MQX9IgT9Z4OS\/H74R4IFSuD9UrxSmU1XWI7jZSVDE6QLremgtMvt0FR5pRiRzFUUfPccBqQ2MUArHePYU+0Dll0ZNUl0CJ7vjfI\/KEvT\/SASJOxaaGiEGnsWsqWHX6wq9awaHnG3EJ0s1BnVV31LAZN6L2oPVwjUQ7n0\/QR0Qo8Zxua3wIxZjW+ava9uSaTFLNZttutQzeDuMVGZrR0dDCis6XmkrWpissAEG5X0VNYySZtR4L4bNqAHzloTBo056Kz4t1UwJrVHU8QTH\/tUTQFg2W29ny5ytym8IQDncHbrAcCMmqTKkdr3E4nMBlj0L0u0ruk3ivN5i5TyJY625orTnpBPIKoqYUqKQnR0e5fLZ18mdcg9UGF1tykDP\/kQr0XQ62GbFiZhVyR51BtaQgFHq71c3hoLl1siaFyq70GZGXVon2q9eYEQ5ChtHAf8WwZJsCtzuYZKtDdtKOry8yT+4gxKPKZplzP3cxkWI00BnnxHa\/rJa8p49R\/gK0M5fPO2ztcOl5o\/H+xnIB6vUr7MRSj7ZzbrxbDOHlCJshl0KZgkwoMLSmOwajO40sgf05ISj7Z00aaHZzZV\/CdU6w\/Z+QuckZTtkkKys3t\/Oxc5xmV5e0KWL7xpfEyNngUXdkSjiDzcYdmltfOsc1YM6pDZnv+fd+hVHFPZyhRdIsDH\/sQfi12mXACR9N5xuMtI2UoSshVKQBNwp1AeWpufu9XJaxNG7d+BnWRoShFt7ak2NCifJ+bWn1JxotckOW+y16ORrEoLyTUp0JcVKYhBhAhJy\/+qigBrS5fLboEaFcAAdNTSC2NvynLoothNl\/JiDtdBefLvlttcUkKNHT54E80JLuG8lquvrnLTCYdBuBrGYQ5\/HwJqUNdQlLNagyk5a9wOrkxPpU+La3FsjfsL4CEj32ARdxqk0Dx+tABpMcPAtTlZ8Q7Uy4+1\/oBLzrwquW0xbcn53M1oyejT1wWBqNiq01o4YsFfrh1Zn29hvKAXNjngv0Kp2zJAUiKGMKY0z0UnhUYmT\/MhOmXpVR53DwIhV6aT58C23Xe0fo7Gc+lQJplHW\/SuP9bvXxN6TIEcvFOxmha7sCao55cR\/UKQN077b+RGq2uTHEDZtfesqbQoxqXTCDRwI7cCsxv2LHRWP9jN1kNytIb4ZANm06uNjI\/svyl+ZZmJayLkY6SnXjsQJoif2TTMVBzKyAZKQrQMHROVhAAU82qKAPxbZUorAhCrmFJz02WoXHmX9vdgBMJ6Te6ZXutILTjq2Zwb3c\/Q4r4\/C5ryYCoo9qe2HzL+VX3MUldPdwI\/WMLBboVod8xDtW\/RcXFL5CFH7mWBz2mRQBfp8tc1a14q4GLBGVELqFFTgIWn7ftSAK\/gQ0ZftfRAcBNLMJh67gD46c1iGBq05z\/gXX0NEjHwpLLdqKPQ0GZ7TuG5IPwnxnyy9CyGZghM79M\/aNqTn81CC1hk4x\/o\/hkSODbj8MB6Mg1vkT2Bdg7gb7HXD\/umzIMrVmtEHiSX7IAY4gvF815F8EwG9ZnsEHgzJLT+fpL64NZVwbr2WtglgCGoKOctA48HAGHU6S0m6ByhOJaQ7UhZSnawPSIUSvyMULQq34CnPjuxUDang+txqr6g6ZGBt5En5TzmRoipcfGJUcwyJlDQrOuGI36OH\/9YSLm36iSPgml1E8bJCOVn0HCsdMZ94Hc+DpQGemCwBVr3M6pQq3SXJ5sH2kEo0LyZM\/Cd+XAxKtw68NtiQLi38KmuTp78+D5knG33rCXHExZyPMP2XyozvQRmlDR4eLxMvtCIhLSrc8WxzUaCIp66f1iNqDOvukTmh6eXbM1MiNUyjv0L9DvgIHH3YJWapeba944yBcBdIxW58EtA0l7zchD72CItCjUl+jRqwDp3gzodjCoTmoX5EJ6qT983BtGCC4y90y8yEVfoPYDeeNbOYAJqR4ikMjWU7PdwSFuvVSOYJYOIVomc17og\/QfMTVVEX+Ecofxw0iS0SsB9rT53pg6gxmdVgJTCd1pX20FWmSD15Pb86CGkEAbYDDiihYIDVSSQh3xvSjUM+Bfo\/m8+Aw0uGySmm5LIhkp+cUY0u2SrWv0Zjgp8rxIJD1iwBMN3e8Zb3err4SHuaNvbzeKTpcSd7MbuJHvBDkGy62ZyXcIg9CLj7VPiuJqsu1OSas5BsqUjs+qKqXMQhUhEpg0LzHf1wS\/LAsKXzgkDePqtDfO6QhTQXPYXeSNqH7HxnRrO7zbyK9izonpnzpDL+vejYdVsstM69FpRBB34ymkJjMk88monpF7m9CzNbAHX6O09su3IVDEpVMb6IDyTNvq2KhhVTk0pFK4lDOlwxWyJkE+ddZots8k99r+TA5SADmYLYsp11KjxrsJvoHms77K50eBMx2LYdQRG078oNKSF72y1ufWK69ns2YqfQ9JRVUTv9kYO16Pz2LreEF\/fXPfT2qwW5D8l4nD+v55VXKDajuvNSFhc09Q\/0qtfHP9IyA\/l0T0YlCFW0gqmn0BnJ8Ggzztg0hI5atT52nYJKLzmpJjSSLeaYPPpnOZnd\/J5MQ4In2sejVn3Jv9M9paaI47aXqNGt1HYkdN3D9KjFKSpViDFn\/+RAbQOCvTeGkIHv0uLIK5gTVJHxkY6rPqkF+92mPdaOZitcFTgzinyK2QjGYa9q36B9ATJv8OND\/ayPcCjIs1kRa6lVzxW\/6BmJBefq+z6sk\/vlEJokdtKPUg6wI3Bfebz7rr8sddM5FY70uZgtZIuBEVCO5hHJBeuHEusPxPUWp31Xlw5M\/s6XI0GB5\/2rLhoR4Uz4CdzdFDI\/UFHs+cVOM+cY7fKrTViSxvXkWomGhP6isaV7DRxrFsUWpDoq\/WK+xGsQc2vYYEGMKnEbaUp8Z74Gh9RU7A5ONQQL00S8IWC+gUlv7VCcUaAlbQi1MJbNeaWHHM2h9tYJFs5POLJZeslEb7AgxrFNmYi+5An38R5nDGUdurIrHS5kAtmVA0Grq8h94y0hC+hOglKXSkIFF\/FMI\/27T3G13Lx6VqVX2aLMP3iGR4IYRjKVvhHp1gDvojMBGb8G+y82X0EcuBeyCCvdKc\/mT13NaZVYiU87vR+NtjKI1PnJoDzNyDbcoJjwvXpflgA1PBwVXxP5DJJd1O09neTRc2PqrCtQ70d1EZfkK51mHI0Av\/ocE\/1\/GBFCo3Nc1nUZQS58K2c1KdzsWwM+q5RyXuBx3noVD3o0n+0dm8tajQq8qhxOkWM643\/h9+XOtdI2k6ibOe4OvC\/cRuwAF+fixRHpW+BrvLm\/SFPmWtH\/MQxbnWpwLdnq6N2SLnx5hqEuaFx4VpnEq02XGH5ww6J6gmBOaOzuvIlcOCANKIpLO3kGbqJrKUMHvroqpnBXIa49\/vCHRln2R+T3fBP5K87K4DOeIoL5caVngWdFhfn8VJ3yy2LAm6WEN3EHnBgwUUV7uhalyx+V7rOG+T234DpviP22CAePhNBcdp8it11Pkw8FwZZTxg9iYDm\/Dgmc8Enh18qIEVaS8315Oes34tajrvFErmKliWQgDgfS1dExvfmAZBZW0F4\/3zYh3UX5rg8n9pn8OKySpgjH1+R1+RHpLnd8nBExKdIiAR7K50hj4\/O\/c3hYv\/9ZvwzkEPUacqY+GEx55KS\/tDU5szrUxE9uPtdRHasQ2gdDGm9W3vBMzV+slrUcPtFtJp6GGkE+YuGTJuReDgQhNVwDncGrpjW5BfGRCt+5fkhbslxxZQFLg5RKzsy0uSTkgibpvH3Owm\/zjkj1odBuA4ZpmDdEmjSg1Y9Gv4S\/gI4rd8U155+FSBAJl1Fu\/SmJ4jigOCFP10sM5gcGkqsRoaUncnSiBkk+MmcJtLL2TzD0hhHU+LR33E17HhidUlZGvjgSM+dAhi3Mw\/Sfk9xUdKpZUvykbm7qFx+l3Hf0WXWquKhllI8HPEu9qgH8CZSNeIQ3QnLUxV9yYgqrIOwbaGZ8PCSXRYA2arfyLAEgqwhDT82sQcsM3vmNARLbXdP8DIE\/BQVydBC+hhErcKCGeyFYGM3tw0x2EJtBq5xCLpYR+o0nAQ6j8MlcC+8RWUNDRL6wmJw60cFFSTaqDb5\/FPzzzfBmjpwHFSJvPyOGLAzd6d1XPlF0o1IPVjmeejaleDWxNKRvlNT2JSg9GsZcMFpapq6Z\/L5nfhcoSN6xu2heq7JaSUM3L5LKS25KE1V3dJSIed0SOuyipFqnzxWHMZ5X21IVa+lF7OOPibxFwjhAMjvRwtALo0anyoeb\/IhIQmntemGCdyYtlKIW3GUwuTJUp\/GtG7Y03YRhVhjjhCZgL9cray\/ogSQ5XGbO0Udf26+JTjOUISJwqqBML2vttxcao9BG9PRGSibc8W+V73Vy9OZgEOXyv++NTbvNvDqdmK1GfpCrdOjgbVzmTaWoJgq3WFX+LyvTXG3zGh9CfAZqA10RfZryFCuHnpxBqcEbAf6zYfisxrPk4eCBpzi7R5aqQGzSuumNFI0lFAlkmDob75\/ZhEnz1P7pPX5YgTNGHLCveUdIezCS5JO5XPcsjTVLtKjv+vnhEGHH\/sQyROIOqrtR0evEmKRcvvIw66bAf7sMkkw7RkXCUXkTzMrbkPBkQqgJ3dPkCF+I4XxaRSAczpYfKbD43BAeXUep2\/2Bw3npuK47sHrin7Cg0oZZ7yxWKcDnvPmQNV1ppXPfUqdy3TD0jYT30Td+p\/w6Jci7Hroi5kvtXnlFQkl\/m4UDC4uULOiEMQTjsGPo+xOfoK3pMqIe1VieVZkK9oX78KOGQiyGqDJrlAF3EplXP3ZGWp1dUcYSiIZLyuJqS9jcXafv3aGreqj+Qt1FHQJIt8pQw\/PWZjV\/uz7Gznez+eO\/e0A4vw4k4tzdqQT1KN+V9ly7CKB6FDi2oyl5rB6I2zRK15TxHOyMr8ZgmfTp7+BRFqRcJDy\/aZUhUz5aUkC7J1GcQ\/gWMh2JAcIJwe1gKNat\/1N5HivvllNQn\/alWrP0Gz1PEujQKuBgkwUBQ4n1DmMy2gLK6lQYCipshFKPlCyhVxmf8G9CEYVdxd6yf16wwKTS3XRuqeedUUudWKzlg7M2ieojNJOlL6FcneUFdjUzTIpoyDVGc0dNz\/ZkgkUB\/pI2NZjcMber2QREXcRq3se\/ylNoiCM0SfyS4LVTcDVs7dXGne8+4KBWI47nI59hYPNAqrl7So\/8uYgbVH8e0SmiToxKWGQF1HuxHtvk9yxgy0qAsiPazk\/uNgVH3Z5xrIq2dmeTDLJ510pkYO5w72LdhPd72kCjEIMnvE8fs3l6vH\/qvsC9OJwIyFjStb3nmFWNlttYO7oQb+iMCyMmkkQecLfnRjBFEpKYlPBC58ZaUmySo5AmXw+V3t+vbLoRN2Iq0XTyaE62Cb158h9KP+x17p7MW6Jkr4sYFHSI+E5o1HXdF0p1enHxBMpEg6CjnsNNC0HIWO9Ak1R6fI023PJ7gypk\/DJ9jlpXZo0OmaJQrqdCTOkgE3ZLzJJm4Gm0MH6ZJ+8UebMq+Jop4sf8bjXCOGM\/Jb5dz5IlcvCuLtziAFTe8bGeccpt+C6LVslcsmxZUwdnvSGGMIcdSJx8rh2Pjzf+JqfcgCCpMuFBj\/r2H+rahkXqmShR6MX2OW5OBkdXjlBOdSVq0ObNkBtLlx1L3Wp8FB4yLAtpg0lQd+H\/9zyeraM8sBZgikX+9lmvkWEfj2K6Wylf8VbTLonuOA9XXNLnyXBYibhFPTP1jiKHxGM1X7fnmfcmDZam38xQ\/wdaLzjnvkqZHbhwKOYZw6OyYJorhx7Z34e+ENCnkZvCofdOP+cbdN6zs+Tpj7ZMgO69S9P\/8DRf9\/bIVkiDHY5PnrR3KONXn21pBqjH0dGLIbZ2fjzGPQBxdouLnvEjYZZxK5a98hZNtuQ1R4x5KLBZXaudhb6K3kfne4TSFqa3zqQlDa70lw3SethUyGSXpIAq2m4pjACbghL+NNOjskfbIVBu\/Rqea7ZfVWkgpsDUle28SnYL13AbCunv3saoa\/NqcOAAvc7kquCwtx2RZ5aVOeZCXFtNE5Rq+C3YccOgEhjd9iei6T\/eFU3LtW9BpAAWCzdiSIoezgB3mgslleZyr\/EuuqmEDF4DVjwheaRGyUHfqRAb6gHDTvmri69qQpx05L0Jk2aR\/HdShbkgJ6nY+XtPy6NRretwvvZTA4MzXfb8bNGk5YSSuZUc3r4JGyTMZXCL0b\/1+tqTM3qWJ7HTxZcIc2t586P+BanbrR+Sm13JoNzfe\/JEBem\/XqE2T8Px982litS\/b4xCuasHELuk1mFSmnXtnRNOSqEi2jVEtWYJkL03RB+9lf4Ifzr9ocMa1LlMjDv2vqZXpgkJwa3QWsUT9+T3gP2m6YiHQDTS5B70pHstadmzXemBY\/piBtmnTp7PqxP8D7MfoRqToOsUqeVAM\/Qg3JPusAuI0CnpPxe9hS7kUqZyjDvT0uOyn\/ZfppkdXwwwwIwxw2Y6AWE5VeI+j6jbf8WDWSLYLcrDH9YcvpYmC2fTbMpgj67E\/haC\/Tg1VncWobIoFhJVMnTRein1oEAkAaRqWGAPuFS4FkpMCMomTL\/6OpRDBXaPn9OsJFnwpVmUHzIKHHsAjVxYTAgxpDX23OMhoQNBWXnbVRSKFipsm0fFwfp3b8U+OYj3myr+breF2cb8Omsu\/Uc7LqI4yQiL4AzHF0dS06sOPnwc5ZguL7ndA0FNgynVWcXD5Zk1mFZxURchg1N1RdKfo06IUm2NtB25R0bW8UyV1k9XbmqeP8JJjuJMp6S37NW\/RfB7htn8h+T22Nm2JygqsiD1FB6RMqLWazc9DCcLsgTg+sIZvoi5jdyJo\/ZXi8OiyX\/URxJgEmWeHneTbkKtVImyLT01sndBhR7VK6zG6bKFpfmsqWmfLotrDDHBM\/XF36iOfUJ+Hxi6hRsLJD9XsuQ5GeJRPOlGH55A5bjCc9FF2+b6qqtkS40snATE3idldELXx8J8gzWKap1wAfdbhTQlDZie++U\/5laphaMmpzcVVhENojXTEcwJISuC7zbzATuXrIHK2JTDkdxgOo7tyMpvX8CU9jd92qKlvJy5aqvwzOm1UJoe5ot+g0UOQ6ecud6IMjGRBgzBCYn4WK9\/J8PWX6qu7cdw8fU28TGODJwb2h63qSinlejO+Fzsxhf8impcREa65A+TuBW\/CC04Gie27ZwtdQZkHWp8kWodSoMMrheaOiix2MYvXjizjI6rfn9lXPlApZGbgCoNgq5iRBlcV\/yo0CYgnTPl4IYlMYiK76SoxcaCY7BR6jW+HMRCzNmDhe1muWI8vK3RfOjoATG64y9c2JWTsyUuBHDOWO5NrGl\/oFa\/VTj58bSb\/KTkBIxtVkeN1ggaF2XA4DuFttq7lzKf9of1MsnqDeb5RQIR3XoY0pJ6vayF2bzA6cbwLVPsrxx14ffLYfIgBKXmKrGwaXCOoBCB2ZHOD4PNlLL2nd07NhNrXiLur2IUo6KcSHJj4LTvbFC1SmG3jTflBpkLUMFwRlTcmIemoNrgLUTCXtDx\/9GBqZ+lPfMmYLyzK4UnLfpvAHkyclSYSUGnGiYFIrBMZ\/U\/xMMzPDYHtYgIgpnNwHmjUXFbtJr5IFranBXnZxiGH6B5uCFbHzsxkM3X2CZxEjlZQ0sUCvnjfGx2CXkWGNyRZDBnY90VLARqJX3uiDlqdm+Wl6t8eRu1Ex2w+ugw30wkW1s5k3z8DlWxo8m7j7vDSDHNNlq6stwp4m4XJlUM6ka0Pz5W3oKdshbtAUwI6FH0n7qLH0LLXVlFjQvrOfnPIsATK7bL4VMnC2CnfRKWj8vL7f3tewehqFcQ48Y0OvaDJeTD2FBLn5f3e49qQ5gEM5ePJz89mGPYfPCUYobvl6a8Bmfe3np9TUZ8LDrCCfnGoHjomoHk\/q+bGEJWdoOfvrsbAVlwIT67Fn9DanMSiA21AXB5AbpG9F56xnJubBXIvWTcAPRMxQE9rKOZQjIa2NLltq2aAiOMN59Bt0LS2fwbNcrPSVv13XddKp4B6ubxgF+pdpj+u2S2EnsQL3QpZUpg7AFG4prYqDqev6RgoBiNhmP5HgqTNW9rGG+KR96F7f6\/R\/IoI1AJApFugIn2LIUBge4rfW6q7zKPTrM\/AzdDMB86dS2rGUERgqcdOudXYuMecqVMhLWoXrNlOiKgBK\/ZAZ3eujBmP\/jVvfdMEKzGIhBqjWXvkAedXD8YnMP0Y1lKR0C6\/SLkf+Tao9U0abEKiKhQBzD51SIqm4feFEkWtDjatGKrh59ZGKGUmBZcAKLKbuvhL\/2C11KujkegjJdPlsQ1WCi70W48OMMMZUN+9ymu4+sPScMyelKPq7YqUWVg09DOrQustgeUzpWX5GuUI3Te8gZb7PGw9x9snaF\/R3CT8Q2aWJG30znbnUegQ4uPYGxhtbdHt1OcQp7k0Y8Bxl7+YnaMWc75fSh+L12HAQV9V6Jvn2oMMu9+wLt8GYtcyOWTl59pJKcYisIKVjO1qAPBgKf9JZB1\/YYBOOlJjHt7Vckq++NUHFCDt1b9ccwZh+GbFUiHkNKyGsY0iA+Ogn6REPsFPKnyVCWlMQp74fgH1OOTjYI5BdMVGADHepelU5470qPlRvZiaie1txBDW\/vjS81fjwmc7kzSKSgBH55YfvVZB\/ErWk0RPRzhKHH9x9UrNfIfurvKp5wdjlSnbknBUgnfe25z9\/s\/OScixRaWt\/Ali+CeWulQ8F\/XHTDVFqn5whnZQkkk2ZG\/yha01lcP3b4SFZAd6M1zfY3BL37vKYDBtuFlz1drcg2IbzFYW1yrSxWF9mh9Y\/o5ENz390Eu7rnIiVrV5IGExkyinGGw6hGyGwQvribqpwXxdD7Um89pAhGdxSkvyJPJV6qah3mtNog2P8\/1XZd3Gdk5niVzvrDcitb2dAYxbCOuwkRiy+OpEwnwqCtk6rzwBQRvDOZ4lDCf6y6cdrfcR\/DUhiQwJeLH\/BiEZqkvOnqKhaf7y6ysgV2thrfDmn6HwR+d+sK6Tv5SaXbh+YlmGwHStCzjawmfsKB5TUJyP49y5hrwbB\/zwuczcYz2QLW+8svRC\/g67HlIz5gbzt9LJEGtOvcqhbbnLkvY62RJYV\/k\/HS2+I3gdQbTnuP5WC5cxDC7pB8pkUq2+PANpVl+yDh9UKdOltVOetm+b1wP4h+g+3+f+XhsnASHuMRNAY9Ee7WHpoYrzkC+9y9k+9G1IRh8xeLeQ5YwcPOoR3Y5+6b6stwcclT0Jab5cnSxDbETzvWlhGlcgWDOTfe7VhYCLRTLSERg74xcRdP1o3ymocypk7bbRDqc+WTkykMfixQsl6IhbVcrdIXmX9dns\/CnflDl6d8tksMKCoL6NK9AeqqOy9I7pZo2w\/ea91+eN2iMTYDv6WTT4L\/QzDn4TQPY5tN6GFdp1V1QWs6dRjs5TfAwHOhPeBJwLwBNC4HsEq6QjEREGC+uxmIVKO9PNJOgU4nmBRxhqYuQq0uLoCsxPwl4BZBOY15ROFEaFGdWYb17FqUCtH1qQYgn6I5YnbjWZR\/Gxhwj5gSPDjFGTM3H21Q2BvZtjS\/i06TrdEcKUbhDBzygb6YYlAWLhVNMFxpAgizIXB0YNKwdXJ4dBfBGdHMprtX0btjP4XHOtHv73P2GS71rCQQMm6Z0kS2Ee68530lbndv8+\/oY+RruhSmo0bb+1Rvwngu1\/UubUGcAfJ4MnVq45K0ALR3Zgt\/2xP\/gdmoXUOvyWJAq\/37b4QjbdENSWygS5gZNHIvl+N1FYeZhEQANsGMcEie8UlHcOFIk70OQl7s3qkS71mHFfwNz23vNkZvnFB5VfWUciKCwllHjcOx0UVag7NpkSttyaxAnMaUrg4b2o8F6jKOvbfnTbkolbvghagv8UO0Vr8I72+GRK\/elCTLwBawQufP0Q0zjJolphC8xw4EJGwa3dG4DdA8ABtkVJlXoAUEZOVMuIhcHaqGCD++v9qaJ4ubKxPhZZx67J08TparZ4cW3msGvCVfKHZuJNUncMhMJmJ3zAzAkXs3eWUzbjG72Vf4D7SC5NnKEVai+OYYl\/F35WB0qVjrL42uS5Onj7JR74MGlH69cUgNS3eWf4j+6jrEuc8w4R+IdcwFPgcrnO1I2zzroquqkfv37wdDD7vV4ujf9h6bTrLJp6IddaeJci3ADyLbVh1lWNMidgr1YbrJXy+q\/JTCZVVJTqQXOqk6ddeNqB9hq9IORoRKzUxcGwGasBAR02Y70e3aGmAQ+Si9sgsBosscfo4C58DAO\/KumUu9ycWb6mEm+mligVJ\/0mI71B1d9x0w6zBq6mU5fSc1xh8116ODpaZKz5o8EcgJX6p7Fj+TZ3Flaur27TmoyCbiM8rP2\/wUXl+7oR\/ACKGwQwqOuQK\/Q7DkaUKZsUXnSmviFbCdqAdqQbSUpYKnIVogSnoJAJ1Wp8dJdT6i3keSF2KOjMeINSVIXZXQ7TFutLjYQTGovIxYNT1hENIcyuHYc6TbuEybogn3w9HZ8ONYHh80CA3RQPnqSY0sCps2tKjsCAaX4ipJkPnFZStnVPQa3pTb+lhiFgCnaHyE6VseNvlNmNd4LDUF3HOqwRh6\/pDX8yA1VY8pObAgfI3imSR6M2b\/sEdXGRkYCfS\/A41hozfsDQBAPtyz4MvTIYIEt1F48ZTyLSKh12F70hngbwYPMDKlqVzctvm7iJ+pcZ1aep1ISTHCD72PjGtgTSLxmMY5D8ugNzgsbWKL\/RXhCDiXkRBSLfGrBktXExnLuogepp2LYWvtGC5Tvtg6LTjo29fukOtAjp1Ca4doSdwKc9\/ar7fX6+cXKEIUj2sK6FoSj6Brf39Tu3N\/ebkBrzr2Xa2iZonNJ6uTA10NXqY3+dPJhkyWloZ9vm23hkDGLWzq5w43KpjZBz72y0LZsA\/vMTaMTcCgv\/HyHFwsVZoLfsnh9+XP4ao8tROPg89b+GqpEJPkSJzkX9bg7uBMjG3DifyRY051\/e5QG6qAtu0PWAAp052JEu8xhRhEZogqvYxGJep7lMI3uUuijkpj7WroID4rDcJj9\/rg3kgqaJgVReG7+0EIifKgUg+JBwksmKVzTdqEbq7MlWCMkhvFzakSROxNd9TchEnhLIgE0dFt0hGGUIxb5tz1BVsuztakC8rcvyWRi2m1EjEUnd8uPy5n4yAbY6Q1ieIRr6WZu5seP51MV5Gbu+eZgsdBAXd5cnIMjRY8lDvLLp6rjcdFIvn2sU7jjw3c8dh1tvotFeKSBKjam5jVqDMfM\/B+yZuQ4knwcdHqqthu7rmOfr6gmAZzqO99b44MQUxNHk5BmluuzmLzsVu1dC87A0VIgSLYbgA4iByhGVuKfYogxT\/Dtmaff\/jyUtnVgLXxVjDFfvC7rllDcEs1wasIITZNeRjEimwOtAj9Qi8x6U8Wy7M+yOTEtWqN5s8Vy\/eu43ZTEi99cy2kmmarY2Gc7e3jrPZGgWrdgEYSRgIkIg1EKf93ofXM+PvFwDHPawad7dUkfqdQdPByVSlC1tS2ly7cQAdBYDZ9VE\/8F5gLmuic\/hZicdpCdno0yY9pyosSGcQFKtF6+bl5\/hyADBf9W1Q\/lTgvT\/xMLyJR3wnSdTfEigVIn81U1hgancEh2lEmR7mN\/zNkDJyKS4Bkp+tkvC3ORYfvnhJuJLoRw5lr7eGW8OE8R+nZfUjELytRekaojL4UqKhH+SSLMMtLkB0S1jyld4qeaLOL0UE4n7dEmiPo+fbTnwuDHHPR\/qi7bdrkB5WLDCCJFqhAnSjyBcycp3uy0kgqYySZKJ1Ot0nkLwTTbRb3TmYn4TlmeLOfEWGO68\/tBmdGxgn8vxVf01Y9iIJgCm3GiHjUjjADbW8AtYTJ6EdQl39lhWQdTbmQTdfsFreRZV4y3c8BHrDiWi7UwqW6xCNqaGKrIXsE6mXZui0XWzTtQdwHE3L7XdDQoQdL1VK3anUQwDR7L4kDav1kCCXD6jL1WMHHLQ9xVMOs+ALT8mh161wTOIoJcs+lqY8wnW94DwVCACnTxOWMdFUYfxw6EoKAfuR6xOXEeUSV2YzTr4G\/W6tSOZl8l6ziAwOJs95TIcfUIB68y4pMug7+kHoF62ZF+4sro67wn7iccIAaudrKB+\/eValMH1hyGzIXC\/+xkt06hSlWDChs8xl7XCXm6mNqLrvF6Ti\/GnwlDlHHgHkw6oaA0p2Y1ZwAROd8IBTnsDLXv0fSGg\/PpW\/y1ZEwym7HWvni0bYgWtXJRk+1BolPy6e+IWwE5DhaCEYeL+itXGHPjgZMWu0iOHpAOHcshBGfP\/SVyWQMc3InAIk3b6B1NtcDZGFx0ljaZeFA4HSs3N\/+Sf5WJH1i69C9VKGZM8lOCqf6cr4dcnOQjJUi4Ez\/9xUT\/UL5kd2bLLwt7mVsqnEuJuKAoxZOuGDJ0By9Sao1c94YU8FY771AIzZMnzwzgjyyzMQM3T2JpmQpZL9bWNt7XpoWpIWwQXqn\/y09lVtWGA00OtEwcIRCL\/Q5aOoJ8TggbpcmfNsU1rc7a+Qa6DLIggFO0\/0UX7I3JuIB62YPpuO4ttm2ITuzeZxfCzs1KFG4yxjczrwZFoKCb5Knkp3ZHZLcQ9Ob2dlL+cfkHyJpGPWlS\/w1heE=","iv":"f38af58784c831143dda187bc44afc03","s":"368a0b25315a1985"}