Despite a stabilized United States economy, many affluent consumers are still financially weary and on average spend more than two months researching a product before making a purchase, according to a new Martini Report.

The third volume of "The Martini Report" provides an in-depth look at the goals, attitudes and digital behavior of affluents in respect to their personal finances, an aspect of wealthy individuals’ lives that is often misunderstood. With generational and socio-demographical differences in affluents’ approaches to finances at hands, brands and financial advisors will be better equipped to service these clients through offers and promotions that make them feel comfortable.

"I was most surprised that the affluent population, considered to be the most secure financially population, still have fears around their financial future," said Erik Pavelka, CEO or Martini Media, an Evolve Media company.

"In fact, 70 percent of affluents cannot adequately estimate the amount of money they will need for future life events," he said. "They fear outliving their wealth and because of this, most affluents (63 percent) wish they had started saving for retirement earlier."

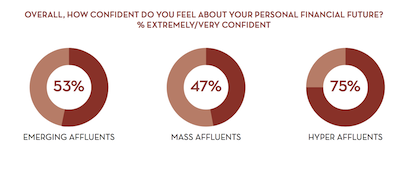

For the third Martini Report, a survey was conducted online by Ipsos MediaCT from Jan. 5-12, 2015 among 1,068 adults ages 18+ with at least $75,000 in annual household income. The respondent group sample included 98 Hyper Affluent consumers with a household income of at least $250,000, 659 Mass Affluent individuals with at least $100,000 in household income and 311 Emerging Affluents with at least $75,000 in annual household income.

Super savers Although affluents account for 70 percent of consumer net worth, and 73 percent of total financial assets in the U.S., this group’s relationship and approach to financial goals are often misunderstood. Many consumers outside the wealth bracket may assume that the ultra-rich and affluent do not have concerns about their finances, as the average U.S. consumer might.

But, Martini has found that there is a strong fear among the affluent community in the U.S. that they have not properly saved for retirement and may outlive what they have set aside for the time when they no longer are working.

Sixty-three percent of affluent respondents felt that they should have began saving for retirement much earlier. Even though many felt that starting to save for retirement would have been a better scenario, 70 percent of the affluent population cannot pinpoint an adequate amount of money that would be needed for the future post-retirement.

The Martini Report infographic

Respondents also cite concerns about the growing costs of higher education for their children, an issue that is a topic of discussion across economic levels. In the survey, only 39 percent of affluents feel that they have sufficient funds to send their child(ren) to college.

This negativity and frugality has translated to making purchases not based off of impulse, but off of need after careful consideration done online. Well-researched purchases also extend to financial products and services to ensure the best quality.

On average affluents research financial products for at least six hours in a typical month across all forms of digital means. For affluent millennials, about half do their research for financial products on tablets and smartphones.

"Affluents are a highly informed sub-segment that take research on financial services very seriously," Mr. Pavelka said. "In fact, affluents spend anywhere from six to nine hours a month researching financial products and services, including the fact that half of affluent millennials are doing so on their mobile devices.

"Affluent millennials are more likely than the wealthier segments to take a self-directed approach to their finances," he said. "Our research revealed that affluent millennials are less likely to trust financial professionals than the other wealth segments."

The Martini Report infographic

Millennials' “self-directed” approach to financial and wealth management is likely a result of the group’s digital-savviness, which has also caused a decrease in financial professionals. In addition, millennials are also much more willing to work with new and innovative financial companies than their Mass and Hyper Affluent counterparts.

To this effect, 80 percent of Hyper Affluents prefer to work with companies that they have already established a relationship with in the past and 20 percent have an interest in opening a new account within the next six months. Only 69 percent of millennials, on the other hand, share a sense of brand loyalty.

Brand loyalty, in all sectors, is thought by many to be fading due a plethora of reasons.

As the global economy unleashes new opportunities and risks, executives for global companies are increasingly optimistic, according to a report by Bain & Company.

Seventy-four percent of interviewed executives are confident about their company’s financial performance, and 75 percent view their ability to adapt as a key competitive advantage. However, as the global economy continues to open up, unforeseen risks such as business complexity, cyber-attacks and faltering loyalty are sprouting (see story).

In digital we trust To foster and facilitate a relationship with affluents as they conduct research online before making a financial product service, finance brands must hone their marketing strategies for the online space.

The Martini Report offers the following best practices to engage with affluent consumers for their financial needs.

To engage with affluent consumers for their financial needs, Martini recommends providing targeted guidance for achieving their monetary goals while having an understanding that wealth differs by economic standing and that not all affluent consumers have a realistic understanding of what is needed to fund “life cycle events.”

Considering extending advertising flights is also useful for a financial firm as these decisions are weighty and a final commitment may take several months. Implementing decision-making tools, especially for millennial affluents, may also be useful to aid in the financial arrangements.

Since emerging millennial affluents will one day mature to become hyper affluent, establishing a sense of trust during this time is important in the consumer’s life cycle journey. This is especially true as many hold distrust for financial professionals due to their experience with the 2008 recession.

Also, as with making a luxury purchase, millennials rely on the opinions and suggestions of their loved ones over a sales associate, or in this case a financial professional. In a digital world, and for a connected consumer, making financial data points easily shared will be appealing when addressing millennials and assisting in their goals.

For example, finance and business forecaster Kiplinger and technology company Vestorly are helping investors and financial advisers connect through an online Wealth Creation channel.

The channel will be a digital library filled with actionable content created by financial professionals for Kiplinger’s 3 million readers. This new vertical on the site enables finance professionals to speak directly to readers, creating opportunities for directed advice (see story).

"Financial firms have some great opportunities to work with affluent millennials," Mr. Pavelka said. "This population wants to work with technologically advanced companies and insofar as a financial services firm can tout their technologies, the ease of working with them and their advanced tools and services the better.

"Affluent millennials' top financial goals are related to emergency funds, followed by retirement savings, vacations and second homes, and then credit card debt," he said.

"This primary focus on emergency funds should help the financial firms consider the timeline for investments, the tools for making money on these perhaps shorter term investments and how this population can take a DIY approach to investing these funds."

Final Take Jen King, lead reporter on Luxury Daily, New York