By Antonio Achille and Daniel Zipser

In these uncertain times, luxury goods companies must take action to “navigate the now,” plan for the recovery, and shape the future.

Amid the coronavirus pandemic, every company’s first priority is, of course, to protect the health and safety of employees, consumers, and business partners. Indeed, luxury companies have pivoted to address urgent public-health needs: factories that produced scarves and perfume now manufacture face masks and hand sanitizer, and many luxury groups have made monetary donations to hospitals and other not-for-profit organizations. At the same time, with millions of people relying on the luxury-goods industry to make a living—from factory workers and retail-store employees to small-town artisans and craftsmen—industry leaders are planning ahead and wrestling with longer-term strategic questions to ensure the survival of their businesses.

In this article, we discuss the impact of the crisis on the luxury-goods sector. We then recommend two sets of priorities for industry executives: short-term actions for “navigating the now” and longer-term considerations for shaping the future.

A hard reset or a short-term blip?

While it is too early to quantify COVID-19’s total financial toll on the sector, the pandemic has certainly shaken some of the foundational aspects of the luxury industry—and some of these changes could be permanent.

Wholesale Darwinism. Even before the pandemic struck, independent luxury-goods wholesalers in Europe (many of which are small, family-owned boutiques) and some of the large North American luxury department stores were already struggling—in part because of luxury brands moving to vertical integration over the past 20 years and, more recently, the growth of ecommerce. This pandemic might force some of them out of business. The damage could extend to brands that have not yet fully transitioned to a vertically integrated distribution model, as well as to upstart brands that need wholesale channels to reach new customers and to finance the development of their full collections. To survive, wholesalers are likely to adopt aggressive commercial and discount policies—which, at least in the medium term, could hurt the luxury positioning of brands that don’t have a concession model.

From global traveler to local shopper. The luxury sector appeals to a global consumer: 20 to 30 percent of industry revenues are generated by consumers making luxury purchases outside their home countries. In 2018, Chinese consumers took more than 150 million trips abroad; we estimate that purchases outside the mainland accounted for more than half of China’s luxury spending that year. Asian shoppers buy luxury goods outside their home countries not only to benefit from lower prices in Europe, but also because shopping has become an integral part of the travel experience: buying a brand in its country of origin comes with a sense of authenticity and excitement. With the recent travel restrictions, an important driver of luxury spending has come to a halt, and we anticipate only a gradual ramp-up in international travel, even after the restrictions are lifted. That said, Chinese consumers remain the biggest growth opportunity for the luxury sector. Brands, clearly, will need a new approach to attracting luxury shoppers. To reactivate Asian luxury consumers in their home countries, brands can focus on creating tailored local experiences, strengthening their digital and omnichannel offerings, and engaging more deeply with consumers in tier-two and -three cities. The latter will be challenging, given the limitations in both retail infrastructure and customer-service capabilities in those cities.

Shows without live audiences. Fashion weeks and trade shows have been essential ways that brands have maintained vibrant relationships with consumers and trade partners. While we expect some return to normalcy on this front, we also believe that the luxury industry—in close collaboration with fashion-week organizers and trade associations—should explore alternative ways to deliver the same kind of magic that these events offer when there are restrictions on international travel and large gatherings. Industry players might also consider pushing for a coordinated revamping of the fashion calendar, with brands simplifying and streamlining their presentation calendars.

From ownership to experience, and back again. “Experiential luxury”—think high-end hotels, resorts, cruises, and restaurants—has been one of the most dynamic and fast-growing components of the luxury sector. Millennials (those born 1980–95) opted more for experiences and “Instagrammable moments” rather than luxury items. Baby boomers (born 1946–64), too, were moving in this direction, having already accumulated luxury products over the years. While we expect the positive momentum of experiential luxury to persist, it will slow down in the short term as consumers temporarily revert to buying goods over experiences.

Hyperpolarization in performance. Even before the crisis, it made little sense to talk about the sector in terms of averages because growth rates and profit margins were so widely spread out. Even within the same segment and price point, luxury brands’ growth varied from 40 percent to negative percentages, and earnings from 50 percent to single-digit percentages. We expect further polarization based on three fundamentals: the health of a brand’s balance sheet prior to the crisis, the resilience of its operating model (including its digital capacity, the agility of its supply chain, and its dependence on wholesale channels), and its response to COVID-19.

Another chance for “rare gems.” Over the past decade, European luxury conglomerates, private-equity firms, and, more recently, U.S. fashion groups and Middle Eastern investors eagerly snapped up attractive acquisition targets. As a result of the current crisis, some of these acquirers—particularly those that are not luxury companies themselves—could find that they have neither the core competencies nor the patience to nurture these high-potential brands, and thus might be willing to put them back on the market. Acquisitions that were once forbiddingly expensive could become viable in the post-crisis period. Such developments could result in further industry consolidation or even the formation of new luxury conglomerates.

Time and again, the luxury industry has proved capable of reinvention. We are confident about the sector’s long-term potential. But some brands will emerge from the crisis stronger, while others will struggle to preserve the integrity of their business. Much will depend on their ability to respond to the short-term urgencies related to COVID-19 while simultaneously planning and executing for the future.

‘Navigating the now’: Immediate priorities

Many luxury executives have demonstrated caring leadership during this crisis. They are prioritizing the safety of employees and customers and proactively communicating with all stakeholders about their new health and safety protocols, crisis-response activities, and the steps they are taking to keep operations running. At the same time, they must take quick action to ensure that their businesses weather the crisis. Here are short-term actions that company leaders should consider taking.

Review 2020 inventory and rethink 2021 collections. Sales for this year’s spring season are as much as 70 percent lower than last year—not surprising, considering that consumers had little opportunity to explore the spring and summer collections in stores. Decide how to phase in the 2020 fall and winter collections and develop a plan for dealing with unprecedented levels of unsold 2020 inventory—without resorting to steep discounts, which jeopardize brand equity. Stay informed about wholesalers’ and e-retailers’ plans to clear extra inventory. In some cases, inventory swaps might be preferable to aggressive promotions and discounting. One way to use extra inventory could be to reward loyal customers with gifts or other types of giveaways to surprise and delight them, while also whetting their appetite to shop across collections or categories.

Enhance digital engagement. As stores remain closed in many parts of the world, ecommerce is a crucial channel for keeping sales up, communicating with customers, and forging a sense of community around a brand. Accelerate your digital investments and shift media spending to online channels, with a focus on customer activation rather than brand building. Aside from enhancing your own Web sites, also consider partnerships with reputable e-retailers. Digital marketing could help not only boost online sales but also entice consumers to visit stores once they reopen.

Manage for cash. Set up a cash-control team, with representation from the procurement and sales teams, to examine spending and identify responsible reductions in cash outflow. Review lease contracts and all operating expenses, including marketing spending and events. At the same time, prepare to selectively support wholesalers and department stores by extending accounts-receivable terms and arranging inventory swaps. Work closely with government authorities on a country-by-country basis to find ways to alleviate cash strains with public measures.

Take a “cleansheet” view of demand planning. Review your 2020 budget and inventory plans, assessing COVID-19’s impact on each region and business unit. Adjust revenue and profit forecasts and create incentives for business-unit heads to set new targets. Resist the temptation to push sales at the expense of margins, as a sales-focused approach will likely yield inaccurate demand projections and, consequently, large amounts of unsold inventory.

Assess the strength of your supply chain. More than 40 percent of global luxury-goods production happens in Italy—and all the Italian factories, including small, family-based façonniers (a French term that loosely translates to “contract manufacturers”), have temporarily shut down. Luxury companies should assess, category by category and product by product, where the impact is likely to be felt most acutely. Potential short-term actions include moving inventory across regions and channels, privileging geographic markets that are less affected, and making sure to fulfill online orders. In the medium term, luxury companies should help production partners recover by making prompt payments and restoring production as quickly as possible. If Italy’s façonniers do not survive, a signature element of the luxury ecosystem—the craftsmanship that is the result of excellence and skill passed down through generations, and the source of the “Made in Italy” aura—could be lost forever.

Adjust merchandising plans. As consumers’ social routines adapt to lockdowns and physical-distancing restrictions, we are starting to see changes in buying behavior. For example, some luxury players report that, in terms of price points, high-end and low-end luxury items are proving more resilient than those in the middle of the range, perhaps due to a combination of “revenge spending” (a phrase that refers to pent-up demand for luxury items during or after crises) and a desire to maximize value for money by purchasing functional items. They are also seeing handbags and small leather goods selling better than ready-to-wear apparel during the crisis. Children’s wear seems to be doing particularly well. Millennials have not reduced their spending as much as other adult segments have. These are the observations of a few luxury players, but clearly there is no one-size-fits-all merchandising plan. Brands should carefully analyze sales data and embed consumer insights into their merchandising plans.

Shape the next normal: Longer-term considerations

Stabilizing the business during the crisis is crucial—but management must not lose sight of the longer term. Here are strategic actions to consider taking during the recovery.

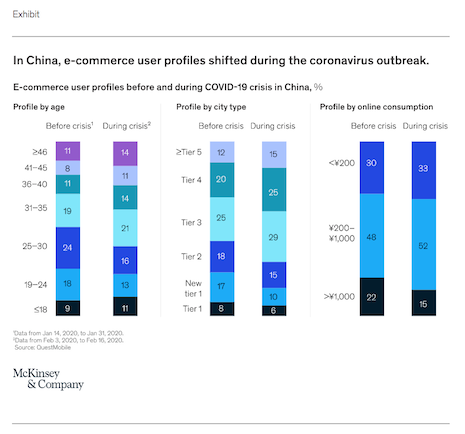

Put digital at the center of your operating model. For many companies, this crisis has been a catalyst for developing and executing an online and omnichannel strategy. In China, ecommerce has attracted new customer segments and markets; we can expect a similar pattern to play out in other geographies. Start by allocating a greater share of investment to the online channel. Explore new ways of partnering with established e-retailers. Step up your personalization efforts in digital marketing. Luxury consumers are accustomed to a high standard of service in stores; the emphasis, then, should be on creating a personalized digital experience of the same quality.

Ecommerce user profiles before and during COVID-19 crisis in China. Source: McKinsey & Company

Ecommerce user profiles before and during COVID-19 crisis in China. Source: McKinsey & Company

Build competencies related to resilience and transformation. For the past 30 years, the luxury sector has created value, thanks to its creativity and innovation. In addition to supporting core competencies such as design, marketing and merchandising, luxury businesses now need to build the managerial talent to support the CEO in resilience and transformation. One possibility is to create a new C-suite position, the chief transformation officer, to emphasize the importance of these competencies.

Boldly reshape the ecosystem, including through M&A. Crises can create new avenues for growth. Companies should ask themselves questions such as: “Are there companies we could potentially partner with, both to keep them in business and to allow us to expand into adjacent markets or product categories? Are there moves along the value chain (such as vertical integration) that have become more attractive? What partnerships or acquisitions—perhaps in the technology arena—could we pursue now that were less viable before? What brands could we acquire to complement our portfolio or to initiate our journey toward becoming a larger luxury group?” As companies seek to form partnerships or make acquisitions, it will be important to consider not just economic rationales but social rationales as well: For example, could an M&A deal help a supplier in distress, save jobs in a struggling community, or strengthen the luxury sector for the longer term?

Anticipate shifts in consumer sentiment and behavior. Consumers are the ultimate shareholders of the luxury sector. We expect that, once conditions allow, consumers will want to resume their normal lives. However, the next normal might look quite different; luxury companies must try to anticipate and respond to whatever that next normal will be. For example, in our recent conversations with CEOs, one trend that is likely to intensify post-crisis is the trend toward sustainability and the desire for more-responsible consumption—reinforcing the need for companies to provide clear, detailed information about their processes and products. Experience also suggests that, after a large-scale crisis with a heavy emotional toll, consumer preferences could shift, at least for a time, toward “silent luxury”—paying more attention to classic elements, such as craftsmanship and heritage, and less to conspicuousness and “bling.”

Digitize the end-to-end supply chain. Technology — from remote-working platforms to virtual showrooms—can help luxury companies maintain productivity during the crisis and, perhaps, even improve productivity for good. In addition, the commercial elements (such as virtual showrooms and digital prototyping and sampling) will be valuable in maintaining strong relationships with buyers, even during times when travel restrictions are in place. Digitizing the supply chain from end to end will, of course, require investment in innovative, leading-edge technologies.

While the COVID-19 pandemic has made for a challenging 2020, we are confident that, with careful planning and deft execution, the luxury-goods sector can successfully weather the crisis and emerge even stronger. The actions we have outlined here can help you and the other leaders in your organization navigate the challenges of today while building and strengthening your business for the longer term.

Antonio Achille is a senior partner in McKinsey’s Milan office, and Daniel Zipser is a senior partner in the Shenzhen office.

The authors wish to thank Anita Balchandani, Achim Berg, Raphael Buck, Aimee Kim, Emanuele Pedrotti, and Althea Peng for their contributions to this article.

Published with permission from Jing Daily. Adapted for clarity and style. This post originally appeared on McKinsey & Co.’s Web site.

Please click here to download a PDF copy of McKinsey's "A perspective for the luxury goods industry during – and after – coronavirus"

{"ct":"knR5gfafo7LMmXmbXIxnYn7MWb6EMTrbV9XDhaUFruXNn4BDqWuR62GMtx\/b6NOlmnIDF1LU\/NNLWS4xhY0U2vrEm8z3d\/4Mt5P2ZSzYWhJfalEUWNhqGUzWCTt3P4x+k6frd6LaMSxsYUcKxZAeu2SoNtouR\/kqtYOvwAUb\/1CRPL0JjPAkGc0sRbXoxQQ5mKB8LLK\/UjgSCw1DSV5mS0S1rhmVbCHAaVu\/Drwjt3xH5kHk7O+mTLqPYe9KwxLdCkl\/YQYWq4BD6DfRRboMFH8byuMVi0fibx2vzxCIvWe71bCfWbSlbhnpDW8cuXnP\/0L9XSS5iY68moUbLTTcWq4fcLvQ6fi+JBkVnrjrLPEvTMORPP0ZMLJrJaWwdH5XE7VfsTVsIhDI81vbcjZh2MqKcVeRl3jlmywsVSBXHFTF5QV6xz63Y5wMiPRr2DH8xF1pVoW\/4SX1IVUGkFaJz\/Wx5yEdq\/Z7pNMFc14qreCb0auJ9uDX1hhZJaYuM1KwGemZLNpV8fUDpgNRFfH5OjPsC0PI7iO0PP0GK\/U6n8Rq+OsnHjm5z1D1NETrrmn6IGPIRjirZEmt0P+Ev4b4Riz\/SSS5GJsvlcpwreyY+kgpR9774eV17ykX8oMKe3TYDEJl2tToeC+lP07W6\/1oj9kVV3cA1a27EwHyWhiVcgoL4gUyeLxRMUSdylopIZnMuiCTXwgad6zaBd9h6A1ikTtr3yv+4gv1izdjHNC1mXQaVa5BaqMOFTWg18i3urXv3wjFTvUR+oxaRvZqd5gTSgYmduB7pTIcyFSi9vErNOKlXXiAFbVPFGVm5x\/u\/WcD\/WU8U3rYY\/3lLUjL2yXKYv6Op9Uc3JksfDdDAiKmBjHtPboOH88J7Ik\/rLByUZsJ65ssiSPs+v+Bp0Txula6Kjifd7IGWfKggl6JxKz\/uXtOOaSPHUoK55U05rcXdn7g2p9YOVfFbASwK3PxOzwogRao2tvuICTkjPE9yDrwswntoxa47uCrc9crHoEb44tDFgPlA5FRGCflEZjj+h1Szjot2Y1LauXtfNB2zj4U7xFQKGRl3wJn7BLoCIEaEky1tSjGZpY09iKRaURKxON0xFR7pQ2jljltXBj6xcV8TuIdvdGXLEfxIjIvkTr4O9WajMaHWjBfpJ\/MeFGYX6ZzlreB8bDY96d8AyO\/eO6x7pMCgCLCgKF3nuFgiuR8tR4dViWT\/ci8BR5E08nq2wbgm\/PuMWnOpSyWzn7tMP+REuPdqCh5IcX5a9EMoiQ2rhs44PE9IKC+NGbcHlKUtuTReqF4ot7Ts+lbeQbWskRcUS60SmwcNpE\/HGvY+tlMtA3KfRsrK7e8xqhsHC7ZbgxZ+XsjkYUC54FhrRdAFg1ohS1dPQ\/HEA4lk2ZvputpSYV28XZLYQZ62J7mM2BrNwjeC7f\/Pb+RZeLzYUJG8cmwhR9zmwJ7iLohvJ2iFdxeSGY7bOipn\/nOjlV1mWeqDPJyBgDGNONrm31yTEL7TiI2ZRMK22aTE7l+6oi4b46JC\/efwYvi1uyju1vQWdH00tJJQdIkjvLXh8ykABb9Ihy8SJLcts7foBWNoiVVxo0VMcmiXzQg+gJz7L4NuLVhbbYZ9+dor1t3JF+\/QmkRHRvMC3WAyo0njskC8s919\/l5oBnfF\/2hKnMQAQkyzticFdQYi7QSuEeebrcuIUHx8SEObbjElQedsEBRBUGNMxXB\/lwGl2XtVAabEUXdWj6Vda5diN8PSlqh6zJxI2Aa51jM4rPjE+4IBnntH2e0n07qIl\/0GG9wGFx\/6jkU8inDpdd8NQqrVc+J2g0IIGocdXwHb2lg0ZZ1J+UucMfbFP8YN1MdBoJ0GpWgqo0MO4zQob1t0E2xD4SNBzruVCJH+VERui1YnMbu4M0ilSD3VUL2njMgtoWtOhUHeKO7YQgKxOfCozA+knU1Wh90zhV1vaVUzyV8HqiWcw7mrQdGGZHwYFRGAoF4oJjuAm3lI\/ymGcsekJ4w5N1bEvqRGtNFOuF85yBI95T4X2S2WaEwLK+rKe86xI4pRX4NU\/Nf0gqijZAMPF5DnS81KzBRFC2Nk1XuUaHKkYy9RhUkHlhNsfLwshPK+sI\/6W6lx2lsn8u4Hf4AgpvANMG8Wqcng1nxLodZf2g6x2Gz+nTCKRKgFM2v0rbeboSxyyyqN9G4NvWa79fVD+uGexLfcQD1rxHTiUFRvbYbnuWnnDztfE3UDfV6EWUmsJ5KCfdXqZGO5gCyKsDvwHSrUf3VJUUKUHsZVOf+vnU4tfv8hNAZq\/SArM5hIC5IEkU93U8oUV+8R0UMfGZ949P2nDO03IkhFXNN9QWNs0Qvx\/6LKbIR4Uq4dhjhQhhiiOBMU9gWtRQ7iqzUjAOPgjqPnZo1qgqIJ+\/+kBjQMymwpEie171EB+hv4Q\/DwIKxZ+410QnNTv5OYPVG6qH8tFWuXMqwxjLgMZtWqO7rooOi6Hlieh72Olx7V6eWA+dqG2PoP04ImhjdDJJuTX07zpA+6GPCMotLjQtZRdzFwMPhrs4Ovk7Jtpgc4AHjZ2N1aeAY6EN+bCRHBRQgT62slHmcUsHCKs3iDqhOkn+oR66webQOVnHQsJM\/xOGfz29pikkh1K6DyS0u1cij81MlaulCqOp9lA\/NYRxAdoJYmOCtoJrE5qGGuwU9tVBjoScE2fRqQp+YGMfxnbaV4SYJtK94SZNDCVIQHVGdKDUMWjKCh5b81g6rv556hN0+IN0babOW6eJ+YWEmsIjf5+tQ3OZ2qeF4zjzidfx+0OdJAcG+bClXH1hGsYdJ+jr5V\/Ymtn6QjfWIw2wfOy8GnOG2aKHHVFYROYoB5HD2adm6XY8sAlRn45o4vXsH3eBwkGL8cbADiuCCsSGtWHeCujBAnF479oVNp4OjNSQ2cTx6pxL1CukPDIFve2l7nwpOv2qRdjT+VcoytGKFEmqMDuFT7X5IrIN4n1k5q4LPaxN0ASkGOg2A4H\/y\/w3wD\/MVhTjLcPqvlGNDZOC8nD7+th6BXUB1kCBLOKqhg9Ymlz9VKCeujk38jn7KUb4Ni8Nrkl38HsQ20aaBwQ76tyPWU\/rZjKLQFWZ6zmX\/0py\/33cVC+t5bDjG+Oe+XdkmhA+sVzTNxsubCYWQudaxyqMigh0KQQwjY6kbBSLzcZlTYkS9rT2+prncr1c3zC1S9Iz4vlz3Q+R4BRHcuY3LopFJOdJNRfhunlQMyw76f5sp2u7uV9EOjV3VGseQRf8arTWfUN6NYueJGp+hGOGP5aJsawvc0ebXQraaCcIeaXtt02k5jLxN1vE251lcLBFEx\/PuMTiOwXIwKAhuZYIKrxOKtrguc3RHKglyS7HKU6cfTrbo1vc8K7y\/9yf+1aPhMIaKdi\/EdyyUMZ\/NTCpFhTbWVqrKotEK0nOTDHDZnDoy1Sp\/pb1F0OHCOKoZHLW+DcA5ZZXE6zVCOyjwzt8tRK78+FAm2YRN4cihjxOq3\/L\/RQyYzHqah6cMxS+Dqeqj7GB0dWKsh3CAjTaWHDfyblI6R3r4c0YIhgHDUan3qDOJccNJHgYs6tCS682GurqVHK3KoyZ0LhUdsjWwYd9n7t73Eq\/lWYebdoq7RPz6Cs21VHZ8hfsKu8bAdnZfpur\/Ow8FrInL1DNSTJSBwUL7pIblCU08Gf+ZJpANOXkN9tTjeAOMBuBhv4FWRqSRLWrrRYRCb\/8S0hkTJfu4ELCuH3GElWSsBP8DJgspMFNmOqjmyQ9w8P8NdbtkXuPgiKQNQNsY8YACLb8ra1KkrTPlMLWjCSzMSYmvtwWcGOShNq5QArMNGTq00YCmZL6ULemM8t41MEDTJ85OjwONzpjhcKGRBWetZmF++WHvmIBbIqKHFWPu0nhrdAbqPW7ntQV6kDcc4Voa09hU4NTUsDzsSYTvSHfaxfUrCEmRk0XPdfUxXZELBZ7hYzGQpLU41Es+0\/DXei9ZPzgrf4IRG4OE7Ma+pq\/gStBbmdJWb614vKxbAB5u5FHIfvBGbA4yzP\/R+wNJTYZbnhXyyCEIFPIGFNXYTJjNkSVmJ2uQRN5JVSPfNc+QDclT3ejvz245G3E2tYLIwN9tvVPfXBwd0P2\/Ssp2cootp+nwpmmoLne1DqlSaRwca7rYeGEUh\/OD6O4pkUiRh1mSoOJXuRrkeFuO6l37L0zgEvvKplJLIIKOcnWQpiQxkom8VDvrY3okKTkBvcZ+6ePs56eit6SqBhQx7\/5lalfk0PtMGp5S6GdS77JueJV0eF15NtTIIz+zgqiYbcBB9FuEoYAAiU9b+P2I8KUrMlg7aZfI2kUl6vtMT\/6dqEXB3klkbklkA277\/I2xO7ZF7MvTsJZBZu3734g6YwPlZVFTfqUhrtffvG\/bpN9\/gAloQBT2dxJk6y7y+Be8rtQDYwzD1fjccZDCakcc9mdqx7x797L\/0hFnnb5lY+USoPqVIRk2AoDZYzG+1lmMQUPswXbhMaPeFUudZy6+QFk1VO3PIa59zUUDrMsA0xghcnMfBMu7hD5iDKoHnZbMaFa+RDLgSXcWNE\/7KFzqMlmWmz0skK7hDJvtM4c0sHFoRPJrbym28Zs3vYKyCqzL+BnW9mkwEoAEfuoIWgcwmIClDS7HBIbV1DiSmaEIvc2o8fqT2E\/pOsCtWbSDZfDZC8oymHXo802pbPWmrWilL4KFnzL8B\/lAlVLrLG7QdbNzfpI50+waIv7qjPXXRx59GuwMLgZ2i9FEeIFa1F84fkriehEY2hZVQEti1OhZB6S6b2FqEI4LIpNqY3VR9dYtH7u2VNoA0SinNhDpUzWP6R9OlrAPKz332zb9cVC1FM2n5xealmnDH4EbdTKdLEgwt7sksXigNFUylj2Xl2U2qWRqmXmsPTdZnqCILZJdKVMztvjWamAupDsBni8J2rd1i06zsRlsChNkhXTUcAC2\/wtsU6qLQ9KdfBbDIGN1Iu2vfy2VPw16Ki2AGnjBoxXKUuD9wuPd+CqyRDfkFV99FPC2epKWjx831VHARRgNU1Y17UB7TibSpIu6bkcwjJBB0RALNmC2WsuZDIggV9VVwrMB86iTL9Yy7RYR1NREvgwUK+jqosomn96hg2bVSSqNujP5qS1KeHzCusvy0JXxX7KQon0sMcy7h3Fk11g7Z2rNU\/PVguOSerNwjukRuGRBoZJyI\/LB7GUUfApdHYBP9A6eY5QJqSbYCds0rXVAh4EfpeIoF8Z3L\/z\/d2II7lLC0Fbm8e92zAyCJDdVx0BOIzBkvd3cdp0RAOgiJg1WpPMpVnCufGfbaVgiAb2ksoZCkWUJCk50vS8IwMhlAZNIJz\/AWfeBUtW1ACV2rxo2bNEZ9xwBuALK3exrCP1cMj9gzRSDVO7BFVv\/knmm4WR3Id29nbqJKUP0eYaN\/F65XOVddn0cEC0Rf1q0dcQkgo3OlCunXHSjZztk8Ja517yyQSLNK+ki7dvizMujiRr56g6vopoFa1hS7QE+q7VtbWjkfpmmgC9UFTRYjwNKMaRHV5VNEpbO4+AMhxiB1byXqhQcUu2uVa8cb5e5r\/KQ95\/M4NTEV\/pPS5QVApIoJLprNrS\/kEv3\/pL25sRGyYE4vUl+uynEY3fbLB6oxHZsCjO7GaQJPNxkdQ0I3nGCI2i4fVeEZaPDTAaU24XaTQ8lWerz3nnq276V6nxmX0oKGk8OynjdbczjfOPpUBOBwOoS9q9sZffbIWIFKpa0Q9X+q\/7Bm3s6PHDQx6YH57OUHn4oG8AUx++OFyChmarsZwfDRG7JHfEAD74tMFxxUQmLuPHP50in7Sq1iQd6VYfhaPOZe+oNt3CsOnUUudCTCJO\/+l8EeI0\/D0kEfh7tbDt02V\/vtvIkGj+KvGx7VWh8M0GdIyq7cFgIx+7XhhxrTfIrgE8NboaCO30U1GRQMPm0XRmxfNIHuDC93BLjoJtCwBTdo+faoSASS16bgp4Ho30HHA\/lOqJWmYtwcIKKWQaCN+z5ElFSqicQT8M+G4UwP19TMKR13obrmI2UhsRHRtvo\/GAtkXkGkyFDX2DuO3qNTX9awzib5ekBWEC0ifDaUMyyNfeZHMymuPP9guMx\/fYFKcsbKQ+5haJ2\/eq4PehDl2jgr3d5e5UmYhh61q\/Wd\/HnmctEqZemmJn+MU8GafKtkY7mBAYgtVxwRg4X\/LvPJxnOXRinz93zvH8rrWUdnge9Cs9+\/ePus39h6IeVhk+nPQz\/QEWsnQffYaaxflr8uz6q0xKbo5Unl9H7+t8\/lFfm+T+nE2X++wjjDzEiNcDyvDcDDj7N6FLl9IfSUKWlLorKMv6MhqASUMrZv2eA9eeNFenJe6o\/urNDBaPLfSukcAH7zAn6bw69iB8izA31ghQgQ7y38J++Kuzpj5ogsNmW5TvF6zcVG2qygQhzlRB9IJMdOtdIbgom495NJaAkOfG73HIN9Y9pFl+UWTPwDgU5qNk6kzSBUwqVciUh5VXf519zL\/5CNNQNUGkuUJa7DLlJCroQJebbXvyKbb5MFMX\/7mM51dRiUn6Y3V7IPTChIp0vLLFwHMqThInT0g52BqyXdufwZDe9QEsIZipGQovCd3RLc77uTA\/ND+BcNmWhSUBYabmpsG33XkD+Wf1lbzI0djH3knvmiauqK3DgYHGzk0YypTITYnCtofULkl+mkcOMroJAdS\/\/DKR+lohkpgS5f3xmVLVaju53uMXljXnTpXwbzJrWcgDU3Ll679vu6H3M83ToUZfYGAvQRnhJuVsGWFktuIOES6Prosg8jtyCT3X\/AdWRatWjhnt+AD\/Y+Egwfom9XlWWmftDSJM6LH5hc25zf8klQ4VH4KQhy+1oJmAuJUN78mzJ6N\/dSCwYFeI9hX19eMB7TU\/iBFOd8lRqU+QiMCShh0uFnAow6Zfuqvng4D+XwJHL3j\/IHedSmwE7R1DSyK4x5nasCYEKgqsxUZP\/G1TbJB0\/tCBx78HjB9zSu\/HmvdLyfXebNbl9Ig1nZhyulzLpd9CDe4rqaZ37M2rMQe8LbVU6vl3V0UgWIhIOaRpwvC7M2rhtMJKIU7aVxFmJKfaeToGQjz5IcVaj3K6KY2BFelOxbrbZmUxApuAbhaHREdaK33ABbPHNOAQbxQmEE9M50P51euuCNl3qC8dG+ER6DE3Pm3GM1Z0cc\/BFDtI1fDhIW7clKtpdSw\/9XTcLXBi6aq+Yuwv+GoMab7wId091\/rDJ++FJJmFW\/bDAvANa3Tc7z\/b7bcktLGKLvxQNT\/CHtuuWKs9hzsy0kTfhYVN+7lnbmnLBgQspgbJ1K0Oq7Jq4BgBpiBB4srNsB0ZEyN1ThaLd+jFPZxGiUwbaM4DYRn82lDockHKl603xkKpRBaL0yl7Euz5HfIuwY2Nf88n5oIvAE7VVjyxyKCGoENAAY032uxcB3F4PRSCZV5ms\/WSZytO\/3vsosX0FPExkw1zzcLESwI2y9VTrBBKMnEeUCC0p9cc+uEn9Vs5vDMnWXMemV7\/GAfKxOQcVLHauTtA0NfMEMEOtST7hVtMCQZxz\/yFJr+q18Ny9fFHRf5vBBQl+u0oCLQ21RuWfIJ9sa+ez5zfaZAcfLfvzoXVBvzFYoYaTJBb5gWwrK4sw9fV2WlSrsX+mdysXDLDDlOUlLObqTeT0dEIKaUcYCBRue66HbxEWPYj3eShEfbXzMiOfXPMeKzpgRzD0WxvKGwWDlaJxyYoVlkZdAvI97fSVTpoYUomp7mq5\/prCruB726Dlmzx58PKHEtvgdBEsvs+ge60PiMQstdyEUHRmxtDW9xieqpevfGiFNPuYgpDv2DNnxVgcX8Y+tGLIQLEGqPjp+ukrztKJLUm6ay4Ye2GgX8C3xeDnm+MpYFykcN2ZgJZ0V1FKsTtRxi4EDeLrg7DQG\/CNM3WTf9aZT12EsjRecf\/rJC+XdqSSX1t0trbuv+CfNKeuyBc+WqXMUNIgASzqxpq\/VdwS1XN5F2RiOqY3qszPH6270foYt8Osmv3qM\/OvMtDSabEM\/dXOf6US0fO3Qtnp6VCoOznXkCuan5DCY8F6eLuIsKurIZ15O1YbQOx\/mpXOyJvmZSrFy2oBUAzjyapYO29XwkuYwXmkCFEehWJtEb1eGtZmUutsGbqnCde7vAMLobQBcVSQ7RLIFB0Hv1dZxLbjfs3PjpVYzwSPMV4uiEH4T\/eRs3eB6SGEEpTaX8fteygSlspUUpyjSFcgD7xRxNpKPrv1iAr3bkra2IniIaoykpWu8zqGx+CQcVZbP\/ToE6zUO2kGnw7+LslBmYXdDyq6axwNNHLVnOyBNPjIgIaNx\/r6K3jF+G7Y+Wofl6z3AxJOnFihncCXM0LlemHgaoX11IkaXM+sP6YDnCdul7XNdTu54QMJ9hNNeYccqKp0JA0OBAdUSfF4u8YDE7GU\/BAtmb1kpC9uAn9wGODkRQrj5zWLuJpCsE1w\/4yg8ssOd4Ajczyz84a3TNK0GPh6ucZ3N4Zwz5iCvNOx\/EQtJqAwUuH5MQ6g4DigTBeVq\/Qkllv\/fBn\/28nW5YOFSIEE6MxLbOZwj8djmr5FSOk4sNusfThQOIcLWaavD++zl410LfLr9syFSn+aM7lmQ0Op6O\/TK05dVI3QeEdih+qDB178MxwG0HmgR340JkMnd0O2dJKzH0WVOv6t\/xJNGxI7xT1muvD4a86bx5piiRPg3Mz2s3JtbOY+99SQqMuGvJzQcEmJN6VIxmwJKxdG21cUeM5HfvC0hGG\/oaVOxKa\/OuUu\/kLQgIlgFVomNaEVlcAk5U6ziFieA8oe9i2sPKyidBKxIvpMkrGMJ7qmi+UCcS6p+d3\/SUc4u55A8vz702AMcy2nZ0J569CSs4zS0f6FjypjN5Fo+bjAzhhBBsCUpf\/gbzNG1BOeY8qIxrP8IAxMwGz2dqI6uQZNj73DfJyL\/9xCBBYK8qZOFUaQFHASseH6c4asNYuGM51TTzlQygVWVe2sxOYhKSpobghhMudq2bAJpMGrfKqUZrzRuG6GNZGs+AgP4agusjQ5T2OwfgTa1\/fzO58dBPC8bNfpYSDqeEm9y0eLGsxHxAilzaiplk+E7QHAfrP+Q2atRUT4BQlzafh58VWenfRlDmZlaqDPB1\/F\/rw4Wqd\/jp02xI7bCO+mtm5f0JPAnaKEPyao24zI9Stp3p6cjhHpVLnEG97Kxw1l90wbBeWahlHp2k1h8NViigezjOzUOV4Sz0puunRYttO87YQ2Nj6+5+3MEobPYvNe\/K8COOjfaeSODK\/sFSpIOn9XhXwd4bcnLwBk8brbklymSPlNABqQBBKOvXMvYedlaxGffeV+UbS05IGoIZPSpn69ZPg+gP3RSAUlblV1VCZvzov0rOqWh6gwKF1h37rOOct+vRy7uXofN1\/S6HOU6ijwlZg8yPowMrsKfjb0fChwa+svTI8RdAvmTEFEH4TKNLp1UTiRx5ku\/PfIpRplTrSU2LaTm5StzhJUsil0+8TXNafBjEhqxhY5LChlZbqVjBbHwE8veU3ygQxm43Yzfw5y1PMMD\/FCi6qlbQmpvuW9onQnre1RlaL0WK1sFZt58dtkQhvRlw6yG7Gf5rzXTkOjX1MT9\/sz+ZRBiDALy35oVwZcJu7uRgDaYm2jGFKYdSfu0IHLxaTJJRosdBQTk0R1XaIHTkbDSx33aDktbQ5YH5IB5r+OC\/Xv\/fFhLLsrBFzNFztQL2BQH+M19E\/LVgQI1vuy4uvNpP+VV09ASHyPsNhlfdig5NGgFXibPjM+kAfA30\/pLQD208A+oophhzjjBzbnVfloGhTjWZL3oFTL1DIyfkuyReLgWadJO6mv5InESpg+JiHFhDEUf1FaN9QhrpnQiHJAFIloLzLmjCtupnQCTWsTRJCezRUhxVSxDyCc7hAfjruHq68mfe0pGEQo7UOiybdbxoExsxtO4+8r8XZHKP287uw5rIGVSZ97niZmxqSQKj1ade449lajwGGhyJ17OzHULq1KrrwibzFF9dUvSVstTLt5ZhdwkgxI8qC3RsG9J6\/VOTa6Rq2ju7FOj5+Bj21mwV1ZqHgFNARYulcJC48buD3ZMLtM3KmJ68WYZxFlFrT42vYqNoeRXvzt2cSSMi7DKLtOe8EEZRdygyKmXGxcu4tPOxn4QEWm\/znoJSb3XMwF+crcV5nz1QC2phQdhZVEI8uCYFSaffkiJZvFjzqSLuVIsUHiYw9e9AHxor+H4sHXliyOF2ziZVoT7eOSEBm3Qj8Cpj7zD8GCGWpRx\/SRBsgA86Iq0DpSqOSkdqYIgmdSa6gGOEhZ6++wh+VYZm9qDVfuvOfC81xxTxi172W\/lJrJ0puTus2wPeqF+Qf3gz0gv4nr7mi\/WAyxv+nKWEfIy3kJUqgy0CYj2vCtg0Auoia8QF4c1DzVtbpNQs8hhz8v9BzVa\/Ty07fA4cWYGTOMo21tW\/vXqmwqIwEchR1X0Msq6urDdKmbBsZ6o3QHH3KsdMABP+dLc4WBo5W8oz+OINs3azrOQ8vkKSv4YBTrZcIQlsFmtG4jKshqgx7oRUblXnJHvqUivq1yZckhg5zi5x9GPgP0LJCnYrHYVKmW+Uw7K2QP\/Ulw5As5VujRe9PvV3f2xRQK30Uo7A9RN4aykUWzaBO330jycH43aJ+JsIwhzjQf03VTs3GiLuBy+9t4Ueczd4GPv2pQ6Mp7KXywdl+HdskWhzJyJWpggqXUqCy0mZIYqsdo6TsEbZdIasYOnCtytXC3w4yMfaInJcqzdE8yWGiHrl+lFzk9MH5JpmfLT85l0w19v2emZneQXe\/SzS5sZXfUTP7bN0\/M\/XbNFg2AGZadAcaoYdtueoPcxEYsPDiyKkpiC3oIn+Bc3tTkleIxnYBRjopdLlAe4LVwZWA4osDSFMq4rzFrU2ohOb1xbsf+EX9fJgy8ZxFITD4hVD\/3M9wvYTiNBIkSyczmmqnGzfeS\/tweNXtGhqxQVPxMvkgqoiX0e+qj6CJofldalWvmjfWZaun3hf6gHYsypas6Lu2oCUmpp4Hnt+kujwh2eZINAWpUuhuIu\/ZYqMpnwximNFc31LKD1HdgMMSi08mHIeJYorqJVLySBvxNtnOX0dp+xgPUfM7uHOlUp+LltGb0kLwPCfdKCJl5gJye1AgOgG2A6\/HmGeD8m9dH7vZJnV+sQ5JOhiNymbPmHkLZZLHaOKaPYOuoa+SG0nb\/RthUvdhCCUCWkW1uLmxTIYLqFr7PlPwKir1l65w3I1birtVuv3XxaU8UoYmGSJAv8fxAawfYSjoxgUTssdIlcIa8\/a2E9scCFyJbmqWtpPDLiaMGmIVtV3I5HbzA\/byH2BK0FQrUtIgkQZ3rPIQKZ4BfqtyNarHTAgo81VkpV\/M3AfL5R0tFVO4i52asrYSaPCHOWCW4BKNzEJm+2bISUFceTpjgbfBhf1esqEu2fcpeSQEXR2bGAoBpKvSfTK7+5bg2kYvAxMt8CGj06jNDAJ\/zlQHftxIQvc9RQOjBWlPssJoebrUML6pBLebI8vWrADmuiwCVYdY7quIqRqdjFr8\/xGLOK7YMqrcSheQwVmyIZKHWKtHgprvFz+bYlopV7ILSCasoZLhUlioqsmGQgHcT97VpONtWdkPPYH3idrnsamyc5Orq7BMihLFN4IyGvCrDQh5LBP7iKv+DgENIBkqyI5cHXjSlc25R\/bq5gQlmoij2bFOs\/zHGMacSi7EiAKs8+0CteOf1JBvA\/mk0JbZrJCEmmFvmXCl88nCnKRu76fMu93IMwLeRV3kX\/Dkjlw2fopw7l7KGaQ\/Px6wsa5rs0w3XfJBlUT4p4FxgO0VyWTvBH770nfEig1i0FBEAfHxLlsuOvGns\/jjdk3RHGTL4z\/lkfkXJf5iK\/qfq4fY2BhjMkawTgRh5uJUqLfOaPD\/0Tj2M69vgERBNLgO6vQ0qXNxkAOqwLmN7jYYA3yQF\/vKdvC0r+e4Ckzblb5pQE18YNLQ8mpe68873fL7Wvnx2+qdESLj6YNb5kprlnkAxWot4QvoWJlrCTNbSBHDrMkyNhvgh1u7ssaEWZO4qMUcVjiY5KoDhHHUWZGG0xKB8u1iIkgUaD6PhhCnvSlQggV\/BZ+vvs2dEvM1chvKHb2J8lbxTUIHAbv\/QVniFE2zweQ+9qdY3l7xPCElG5qdjYf+j89xKJPuKOOBLToMtWBK6pPnzhRtjVN8\/b7pphfnsw4WqVfmm4Iz8H2lOU6uJ4MDzE\/MT8zTl8orGfrxZ0n6d6ZuPKFraf1jIwpESD6lJmqwEhWfT9KCkSdD2GhBA6OK\/z74kHGko0ibcF+7Z3Bk99Sottfc132Pqu2Tx72o4JblzVLmItNkS\/95rbD6hDrtPQcVyqcbdcj0dsDQGqvNLIZKAbhjXi9Q+RsG2tzWivZ+wNSq\/M1lJCtjPcWnJP+QdyLy4re3W0hhSAxlkWkbTOK+fsAWPGzL+AnqytVQbNVC8qU5X3PI7Ls2\/JQ1fRUAxRDgWqAty3PZrbW\/OeWRzoa+Qg7xromtf\/3Uj34wsXUma6pDa4WDxvJjpaRBt0hDi75VUP+h9N1dWFvXUCHokx8saySV98Ya8JFy+IYOvre5lk9\/YyLyrZP2YY6M72r4vJq0At\/fw97W7jwLL4vZq6QM08OGYok6ZcKYsXddxzBmIeAf4s4\/eiDMRlZGy3dVAm2jwDy\/rP8ee9Iuekjf3I\/6u0BxrI1ipAvF0QCYXBdsM+iSA7Ys4GGBnR877GNsSJM5JiJfOnDuTjyUIRqDvR7XHBVY2g\/7Ft5Oh5S4ASf58DIBZ72vCwUChH4ltcvjVExmkjnYNfgauPAngAt5v3EaQv8aKsBC3VZOoQOZgv+s\/rq1YTP8kGidIjw4GnclmFylTP+ZPdAn+EG614oKySVbptZsCMu9sxR81ByOLfx9I\/zDYfuDd6KoyQNS4odEbSP+pCMFvfu1xO+z0\/CQ+uwmdK+c6+1Sd292fMuvioUOi7eif5IzPMBJj\/PxYKHYpxOFhtl+PWxpRX6GeEtgktK\/flF4Mfk+\/jGua8lycHGPGdo8dvD7jnD\/VwNqLJzbUVQ+M\/uRz7W28Zb52\/armU\/FnmcmI+z3jWHwD6K20VNtw3LIHEi0bHkUrrfDsaGysWCCdDVm7p7bPv6Amc7cdPiWYvodbf0jjFXRCMtsEkWE5ttn\/UzVRNgHZU3XgH2+\/L41CyZY7WpF+Z9Hy0SyvQFUgVs1jQisYQEk+VTWLOfHue7p6pvFNchEPhN0dBlraxFahbvgYPdPi7gVPAsH8l7Vaz2Vqj1J8pj7H0+a3a5ZcWn82bmG37dPf9K8tdc1RlsgB3qAEy7aeF+R15lKN52+sgKRR1DvDbp0weI7+ogcf1HO+njdjpfCmhJ8C+KzgByjWCGDJuS63b5oMOUbqmKTAKjjHD0bXkP+ErgwMV+6AY8rkyW3cZAXZzjfrF9gALTwhldGgnoGDPnY7lJi638dPBljvI27iCbP6i4vHv\/FpRSzvQ9+u2IsOfAh0Twu8AWttdqTKbr+4sa2rm\/kh\/yCB\/wBoPkLWA0gd9fPxb6unqvwyKtJa5Z3qSwUFDUcHK7tZmVWja4IrjeDi8LM7KC1bV6qZEvZwuAZTO4ASIKtBt22OmC7m5CJGAApCvfV4QLJOkO\/gdD99qeXLeBN3\/yOth+TnANdhDZCb3XLWVS9giRSY0Epl6YtAqZUHokaUWHWV0nsPcLBrkZGhptqWmceabK1SFluh4O6UksaiOfZGeFyh\/N6nZtqvfayujzRsxjwW3Q6kg\/SGVdb42QptVzOwyzaKegKL5gOxYnvLAQgjrA5ytJFhRK9k7jHr33QVMKC0w9hro\/qMA\/DkWjlrZVLL+ma\/sj7kJc99Nq7F+6rvl1l1BZcGS0OB5\/b6N0PkuIl3p6IOdg6lzwq+GbeaPtjm\/PiR\/EfXOe+8A19vezCuSECplAN3nO9g38HDVD9VyIEzp4cpBjSAFyChefXbmCPgoXgB8yJLCGUHRXlDFKX0uTOmkN8RyWpxo7FTeBryYrWG6uE3EEBwhiKGXouLEj3scUmjcmWTsmseEsts+PtdLDRY4hoXtEjJYcSLAK1BVC6FShrNyGI54asb19PA4YH5PmCyjpuH\/TpRdcAWiBLKjNqseuoE7D87phWyEVfZJ3lZCN3w1I6OHDtVYWVaWtjDQb04oPUvaTAEdTu80ApqqDrJK6rNEu\/8pIRN+MIQ+48bO3I1oVnWlwvTfiuR++33GuO1mi6CeJhuc7hWWpwM3TkS9tK9MOLu6eexQ+PVJlH7zppjQO3kw1g1qfStN0MmEe4qqIyl8s66JKc1t9gaQxoLhvh9AjQiIte\/KKW5c6LVUxqN0GbS2wxI1bGNQnZ3RQJbHw+\/n1fWztpJ46tBsa4P6EaGhqHf87R4X054WNnFmE9GU2CyCIqcS8xtxNVwf8JvFKZBiKA5H3jenIwPsDmnlDliETI6\/2TeHYzVZ20nuZyPasGcQbGk2F5KyerTeFMrU6eWfBCs07t4zO6fBVoqekv3E09\/wWbFtUuywZPAgVPH+w9jTeO+gu+zlrIHtmIU42yrhU5F3i4iH5AeWtggY1D5uaLrEFc5ApLqG8ToLAEJ+AL3WJ1hb2w50J5qzL760hixZGvaRC1y8MCZpJtC0aKcEQkdup\/8HEnuyfdzjZM84iKTdbKAJy4W4xcSVNU8sG6X9WUFef2UnIHRvj4sMB9mdS7fb27TxLj7lKBPdgLUggqluMKfmrY7e7y0lzZ2SS7iOJrF\/c+22yViBVYFy6z4T38HvzB31FORdQ4ywJl7AdlxHb978GBjQlkf3N2zWMQNSrSl0VdmPq9FlnMDj5qlfWPc6KLzj05\/rpq+PysF3BNbnTfgMO2PtDxyLYanKXLQQyS9WXNvuxxzl1d26NSCkOZ5QzIqRpt81tAGqAofQgkj3XghCygBq6SzdlCaj7XngzUsjEy0Bu8Jdo3TsyLsEbF9iKjvPDZKDeVLOZeppECittWbCw6CDrw7LXhhFgVTnkF3SMp6\/FuTyhYRh4MhGY1\/\/gY4HB0q+krcfesy5hglhX0ijeSu3s+k6tR5t4+VHNXheKoD\/Sd3pEodYi\/rWW2GnyZhbwWs\/bno2jzSo47GXNwH0YxyTi8p4htkDJ6sH++tpieaSojt1BaxDS9l80uCZxWa9DWfNV8BVENtyjdXmD66bkxus4u3tD1UYF4Uwks+ZrBD8F2AJRh21Zf72BEm9cj83FTZ7w\/ysT7BR4L0tHSZ6e1zS+1g2phkIFphg8LX9Hz7pYmrA1l1\/TTP6diZYS33hbxU5H\/iU+etbxY1Q7B93UkEcSfJ9y4Q2QY4xR8rARsPrvGeTJ1NACdPuWsdhog6n1GEQZW++Xp9yNvEtrUW5y2ivL0K0wDTxPRkggDtrAMY8MvwuUL0s9Ugxj67eOWyg+IWBq0VbRupqI799KghYJ0EWJU+9RM8o4VvCozo3eNztjiakcucLjnDNie3pp9SPMuclDFd05htcwMmy1n8Nb7qj6sG39+FtZ9hDqZexqvve8GOVfEFjV4qlCtwrvBI0eQnnFTj2CZle3rEUVpdPIjnuH6lvrk4lCb9URnwxzoTijNMuZO4YM5VtiurwtRfpvEAr5TxjLvGfRNNyKKBfTmf66G3qrQoNE2V6LNS441tFqUI1QMS\/JydjfJjSe8RUB8ArlZZvM47cKOAV7w4kVcmOfJRCGvsVlDSComET+4B4STDeS\/PWhkXzSaQdwuPZYOhKXKkJ\/dGENEV0A3ambkjv5Nt9tIcJtdOwZrBV8kWj0GWz0M9f7p4nqz3jAvyFFMRhn5\/jLbGi7oRYPqI0jcnrtyB0hZzfbrrTFr4CdWttGQjq\/5L9utjDOnOH96y1WZjemoGwAAuONFt5OFLG5YmtmQpwXiPnrFep4mXfXF3CQtTGHpdDc81Wqp8v9bdEQXwHTHZX9O9+zh3VhCccKGlQ\/VlARVZkKvJXwGBSEXt2MlUnTCx4uM1aUpdTaBbheX0ehq9If4LAutnf\/PGyj2STj0Ns59YWRv48nqU79tjAnOn64eHlse18F\/SBXu2s0by+7nK+Vs+hKz1OA9LZb7SguxwRAtUNtJSlWKUkmNuGN1bGYSttXqRBW1wRyYXNzQ2YalFbrcnHyuaRhO1XRz1cqUM\/VbFbUKsT9utkAwsBNfqzhG5OzcubQ8hQ9W\/i7Awsi1Ahzrwj7vVQRSuBtroxcKX4pKzqAUxJRB00eQPtj3\/Ah3UpyaM68K5jVTN5f02G2pO21\/u1qKOsj9N713qh+Xvv7e9tK8UmC\/ar+ngzpzzcUkD1N02ffHqX3P+IcDe4+ccWuClzTMAD\/JJsM82GkQ3eR6Humr8\/jDn0+n9jPfOPgE+P2jG0kSCXCX0L33svDYf7eSQVDjzgDJja42qFN1prb8oWQ\/codn2QuagPmxumAlGILCyaWObwautCBVeJrFmiv+Setz7uJdRGL6poAjcN0WtATFmHx79PuM\/dlA+AZ\/dNYxkK1a6xRvqNTh+5OevhFGv63x6FxehVXYSP2P9\/FFudd1xzFZ63A4xGTF1Yt66fG\/PBLAwlVGOIxUPYZpioAMcUshFBwEP\/gZ3padPVUsx3gm7nql8RRCTwt6Yk47xvsEn8\/m5hQnQkK00QWT58JRW1kOWOWB5PKmZJeDLO04qq24xhSCMAw7KQp\/q2OdZaQvl0l6bakhKT+M\/aYvCZ7hQLhvNgTAu9PVKScFrcWaMZl+6Ou6zJSJ9g1KDHqWqCMEYFkBDK3SVrYJnNQxQ5KrhlFrofJALEra3W6Aab\/KP4tCC1tEJ13Ox+uZs7sCMZlEKGOg+RpSX4HGMaaYgDGQHVRJFBrjzss5KWjjaeN8RoD18H611cHZs\/3nmLK1Ra9zQoG9VThGCxn\/XPQseIFNi7vH94LKAoLoWokWGXpLzkkfQINmavTKIaT6rmWKkAZkpPgGVG0JMg2LVkjxHSb5CSa+tk3eYfV0YPVDL0OzqPW4N8ck2fMOYU3eZoqy8bKO2YHiui6oZQjc6sdfRizzRZ7cEc0DHZYb+Ynu73AL6ldSWRDAACCpYEnqU9KJdLrW5LFy6BwRdyodGtHoatUY9d5SZ9sawNLmsS+HQn4hpkbNOEX44GfndMfNwGikZ7XLSoF0cyA0VSArROv3Z4a8oeDxicyXaHs3IJbQe19CuJJxieSQ3TilOX4hhsCixbOTin9q3Oa3jb3p0DUASeSJw1LbMSEuhrO8ntD7ilQAEhWpTL68+MHRGf5OYdXNYjDh1W8eFu4VtCh3amguYbQfP+abyQCiXApAODO8Xx8Kv\/7hsFbkjSIkvE0G\/TmTMJnqk7QBmyBIlZxSuJL4h0OT9Z4VGYSnXWMmggoPNDUNfwd5yB2YXdGEsk1Uf8Vfn1WXW1jdGNL2OHnUf2sS\/U6yC1Wyex9bSuP0f7hwwz1lPKyQ3nVNVHAILKwXAP\/+7gQvKcoL5c9JZzMQFJ+d8N1XVLom97O9\/GrkqwLydtUHVXray8PCgeGsYBpDOaqrDG8rLNGNrev9K6evWnoZ86o\/p1Idf5+ONLLvSJBHdD6fqGxgk1eUD69xQf\/X+eCFclx3yrn\/Kd9Wg8oEq3ttLWdEX1cLQRKl+4+tLVOKFIR\/2ZeQ9RE6TyU8EX7qmpVqHMsXzThK+NqX3QrEsDf\/o2OJW8iIXh2qGrVOkOZY+2GnPVx2E8YZ6umR\/rNomPJlwhLQNFArqI6a4tTLfP5sKnTVmRiGb97KpIKOlDZlMzZ3SNBOwIdVXXfhGS5qYs\/5E9cDYJEDG7mFTDYSsKtc76RC45hAmDJqxhSsCdW\/PadPsOTjGvgSqtMS+nSwKa4UC3ovoKp6Ne5hkEUNyvbkHJ1wOp0xBpH\/zZMvP8z9bMWcybHZrFg0217Sh3kS9mwQ57mY89FYoo2Sm15bcAzV0pn+qFmWpt3mGykhixF\/5OpDLrmYYVNDWe9QXJc7m0y\/0yT4fXL1fE9AN0sdRwzW\/evm1C4y8wBY5EN6jQNIMcvlwq7QmfkYre3m1Cs1oxHI\/l0kOLehshPHFifvD9Z5qnjLIF\/W63zfZg5lkAwHj4AYx9EZF5KcSb+9KO6nvN75kwRy+RaoK1CJv\/fhpOGBgZikoJliNzflEHD8FjV7IImSYpAVYrhjq6HzkbvX3uy\/dxGcmuJDBo6ae\/7BR4668E9g4rFiT5YxyrfXX6urJvnJtfIGfAyfjtPpx8e3\/2x7oxK99vZjH3GhzYhB1pok1UDBOJNVJZui1jb428iEkEBWRk49yKSzeL7egK1Pypi0EL7siIULZvtzp1tgKZoa9vOyYLmfHSXxmT08DMWZfu42qHyZP9CSOJ3Ps7HzSQod80VBx\/yT8ntpx8hORAbZGbau\/lIdCPEYwdh59MxLFkW0IdoI5FydiSqU2AtwMQpAN6BtbETQxYpp3K\/WgjGMm72fBswukufHF\/dMMpGniIc416+GYepMCKC6NOwH+8ghxnqUfGmpMXPdLdwdkGlIzqjGIAdiE+4IxagZ9ZaM886J1Rl7OLQ8cObOunpE2UTGMi+XxdOWf71CJNWCnaV0xzvO4LiMmyTprXt8mgk4hVd4ZNrr24JcwyGlZxCwrRlVncBGm4nBmoteRa5i8vObhk63nr4nLqjms40N9+5nIVhQRm0iUGKnkl3IR7pw3sCQUkXTEBpCE5vtCQsPccRWZmdJn\/o6ysnrX7jOVhHnVQdh6HqipZh3EuXKSt\/vt1W+TXAqBvTtH4XPa8cJFftCZ6siE74OpTGPv\/OJ1skN4mptz5LfZVPGoQ0Kc9hmCHKAgiyupWlTbYhVja7txefWhPwGThiLNzQwFlgU\/m\/h+btoPbdICZe5ROJxl4Y8XnEjKeHolSfXq4\/LR+i\/hJyaUu+0aFf8QitlHECtbstgKeMCnRRuvMAw17ByFo4q2hAxDtVfYSsmkDAcUBmc\/\/Lbz2dffrRzuMZI0zr3P\/1DBWeBD5Xdts1G+ok7YBECnKUAiGDizc+4hRClK8hv7HiznzlxfzU1ZiGvpcjmDkiSNyhOFW27r0vM91RghZPvKz2EAUocMqEp5TjZq0\/\/zlLj8qLQR\/ldWtJHn0aaP7jCwGcp\/3GKqY\/+Hvnv+Ajpfnp3spJLTabuT10AuwDvfOlmlE2cgE6OIdkBIrJGDaPsLOTJGqY\/7pu1cuFaDPozw1EQxLOz7MZNsfcjugq8kuFoIEHybpbwyxbE6XThstlIOIxJFrSgL1Qp0T32\/vJe2S1V36BBXIDCuW9DXlXeLdD9zImwoD2VFhP5OEJ2QsRu7M6tUgZeELFVmI0evkK2NS8SWILI0SreQyWoykjaLEYskElVrJ\/XiILCennrVhWWlqr2TXBEGf5wd2PvoGXqYwgAHCm4oPKETMlcfeSzG9xPJ\/UWlrCH2O7U+0XtmiqD\/q0\/wdnTbohpX86dQbsy9mUbByr69FP\/1xh7oRqOEMoNXYcWdkaGnN\/cIthvJjYUXS5+fO3yOIYrBSQhBA9WwXrkgQLiaxfc5a2IeU3g1rsX7L+d6jP9GOWgfQwGxz8yRqukZ6NEcvfPkLJNiyKCdiKMCh1Ykb73+Sqn7eZLwbrJ4EclVbMEpJ6aYjW+7wZJBdr6Umb2x8HqgA1ZL\/q0zP\/5VxgjBthVz2VZou4nifSBQQX0XGsNyNGRadkEkxXuCW5NkO0\/knJN1TWZUOFhlJMzgOKF9i3fj\/XpRjJnVamLsmFMiAnzj+B3+AQZGPzrXSZYxHLLWg3wngu7prv2TaWyDsho8Dn2uZM3MVGWo7TwGwI\/U5u9mm9fD+vfEobCGOVvnZQboyp2vqnZVOLTUt4RzLVsw7wUC4uE\/zf4ku5rZrs1I7u8tKQ5lNK6o5KEXHw2BWTSEIV+h\/o8cCmrkHnGFARVOfnMT1R20vBHR4iMJykXg+s+DYeqMTqXFUFsCTInFeOFLeoDEqAzqh7p\/6Z31EVzCgCugJMzl0dW4PRZbSol4HkMXMGH\/IYcbE16\/Sw1CIATqjRD72CRanvaRsIaXM\/Yycs\/PEwZrWeL1dnD+VflFnqyLig7tVRRQl8vOmg9K2GQhk8XNzArnTlyHy3Zzwn\/StA0S1RLWnzULNY67VRfzD6cUjPMYVSLe3TJ1SEEbqYZZYj0mQfdVnJt1pHjEA6zVrBDvXkneyBBPedruUamHQzDUakmK5bRtBtBQd769xu8BvgXxIwd\/qPzpISPSiX+eNnUDWV8+HS0xwvjDelZMeUjjEwbWdagzN4Vj+X4YWeNw6zIxOjpVNPV+VWFQl3t1i41b7V07t+bwS59Y5y50VvrOuuAvZbsFDKbk4Fr6ptrZvD6cuh95Rlz4QyVgJyseDdIr8s7UDkOzR7XNhJvPLTkmmhmzMoiMsmuZrEK2xdAl30OUcR88ZUCoifi+aOVE\/B3nxfLP1O5mhmB7LMY12ReslvS38BNWU+yyFU3QJfO6hwyShJPLikINsdVIUwdZOl3KLxxONyNyJKfmyFmpwjG+z7kjIFSveWQGYWWY67uDOkf0RlRUJyaJHKdtLMGBEvbkZUt1CGbTncaimXBdTzjLnXGjNL3ci\/VClG05sPa\/KN5oSC\/apO0VPlr0h6CkK0lTHxTlrFUy\/bK22zP6XViGhCAAbKF16\/450HMB5NslWJXGRksJ576NVAg9AA9GbtH0i050PWiv+PYM\/JCtv6DeswpQ+AN\/\/+tBsnj\/p3qqGmdo62oGeL6y4fuJj5RbPPNIAoTSJe5p4Abi7Y1BLNGYIN2CvoJsW1Hgt58yMXLKG2DmSVKbEfUnB4Vgm3O2dc8TwM3BuBlAv7KpdJuQyDpuHC99E+cNei6QHGj7tdR0wteBrE4t+y2SywfwSCQsqGfCXyfj342yV+S\/3NijtFlSUfB0B3+PdkkbAR9vhTmpvb6zUi8TesJgq5gFdWt2TItAO\/5se8xgWFmf6gfY7vMgXearI\/pZduhHEfvb3sfi8WErSVfQVvCAq3rLroUwc0fuRVr2NMHBeKqTSS118LrtXqzxmEr2+iRnw\/YvABuAVVYw6z3oCEMGuWK8AHzydDzCh3ll4CRaYUJNIE9kP\/eGvbKxb+uB5kTD0Q1PdjNFyjEjhfGW3ti5dngdzYZqX5zVK7358pYURmqvwt1SfyGSdHld\/SeNE9Z1LcagBa4PfmYRmim\/eMxeZ64Vvid3rMXjBh2\/R\/nt8gbKe6PdLeinLB\/wXSchER40euzBg2eQRyAwPQDDc0GAxp+OZTkZ4XdwkDrUbQPNDteHx37n8brVBXWkmCxLgeDB3f+MPqOIFPKfjtbARS6sG1ZPyC\/9pUXyGv2FkDKDOeNMZJf5UPb8PkqMc\/mQ59r+jlMh6aCWWW8kFpQQW3V8U1yvygLJ3lxYjxXElSV7\/aIim7s2Sv6HfEVXqa1pIM3sX0e67tzH0zWp0CkaEfB14gPLEivX4MtUM9zxk7nKZa9ghn6q8BNBbIR\/FcQktx7\/TRo2FZ0tS2bdubLtTwB+\/947Wku50WdKiCddwHmOzIaIW\/iDwCYyw4YZzm\/2166Q7KNqXZCcMaIWsIyKRlalnuW5rxZx3rGpDMoa6sHgEb7i1TXkWwVIW8NL6X+h0Q13lcfCxCPF1K9r83j2Yac2b3ehubVXMBtyaTCwuhNe3TFWWLt1kF0TQLO64F0Hx3QfhxWf96bUsGcfsW6o9aSJ0y9obHCPct0J6rG3sCsAgqvqwi1YUzC4Mvk2eREB0RpocZPesz4lIAZ8oz89sJWf\/a75cDNskGOhYLI0FqwGTe7JZMq53l5M+f2vKgElMSopI\/y33vraQE+DnRL95IiHuzPWDKt0ZI6uloF6qzavjf6EkTqbl\/27ZC5gMf29qk2OAaHp6C2U3gAaeWjV3ak9eyrSo6i6IngVCvdoRgdw6Jcf\/L1lvR1Q4FJIOkX2UKQUzBB8BWGo5Ww1rSaNU6Ls+GdJtQIZPB5PqZNdaSM+g+O2g2F3pKsvXwivLJcloXciBtd4VBiBWQtTGcpdVbQGuQCVuHiuTV0yypOFD4TXWDP12zXVqdBtSPTjYfwGCtR945CotlRjO6EGoanP7W4yGFeo+xNO8MK19LFsuRmU27BDyY+Z6Mehv75JRBrURV55tkChUQBUhPQkRM8g4r\/CUv2SOR1qkgJr3DcpIdsjDhmNkwm8VEEhZy64PgeqSYIMuRhPNbR56bXkvH\/8iqrBybNJrzfneseYJ2n8ZjmE3e\/bzh4Mfsik9M6a6gWLAtAfickEqJCail\/gUtnyRURUd+sFR8SeRman4xBVAhA4rvaPmQMHXeWGcJJO4PuayJAXF9crGr73IJzfD3DuguWpzgah4PV4qvGlq0tFTI200wUa36NekWt5yVnRKisEuO0sKzL+h\/itQ6kJqIRYP+nlCzOq7\/3+DyvIAhSqIZa3dwtYQEXiGCcgEJvMC6HCfyQnPi3KR1I\/41PjCdrC9mtVkGA8M\/TqA5aK0WhXPzBDXedTdO\/Wz+VJHMI9UkNC0HXvM4IBgUvhMcy5QXP4GPK1PE9m3aQiObiOjI18HSi4FUH4TMPcp3F37Uf4SAFZlXFUePOTcPgaXNqHRCK7wSKN+fOiWBUkjW9fyFvKtvCDduSyud2+sQxpQxyjM70EcWYAQ1FjaDlLlnVfss1xrCI0buZPmDgu5epwR+iA5igTJnSiyRZX36Hhux0ihp0NQBBgYTNiZveYm63UO9oOpSNJDe6qiA92krLc1TBOWrax1GW\/ihKr4VBXJlQEMAUmZPlUfUYFIAJLPeFlNEG6n0\/Jm36L7vaMYW1GT4YiVbmGXGO8Q8rQit6A5EMRp+QtXSRIlfWMFd9q8jJtcPn7pNpxznMOpYB59DrcRoE7fGQObVkVqjsLpW3YFC0U73mCp8qRxhczqaUFCVTDyhKDz5PkuLr9mCt4wniS8Yd3DjODWodoOTQGEH3oCv2fBR+wsZu6Qcw6UupVS+xiBah\/8wMKQteZ9sCuylp4567FyVYuO+i1ukAY6q\/ktd86SQBE9+ZAnxSI4BDX7DrYBTqe97E6Ij4XLALK0ng6xRNROzcpom9n\/yK3++GpWDEaqtA3CNztxET2dCwB3rzbb156kGkPvBvHxFAJ1B0pYn6QFTHB98fno2f0sWAKpHW2zyNU0Nr8eJ4je7Ykxxcj4XHrKAipMp\/2PdNP4sW\/jkig+9EpPhxmjrAWRyL3NfXOEywpCkdlExGIRtnVdMgRf4cpr80tcJQvb9XCpb\/VejsPY56qlvIEihM\/paWfQTSo7L+oBliiigEXty4izIWjQUW9JjhOKXW5skd+\/58xo0q6JK6wTxDst0uclN40tjmymFQYq3kpe2Oh7VTO6esvu\/\/a2Kdd8PL+fTwwdKL7u\/wN41gFEWP2mt2WeEm7wOw3aCpgZhGmkE0LfoCYrNPFfheW443JylRFq+oVriseokeAFEYxl2+OAdw6gLVmBfn9IyULI2dtNHCe2q8KOoRKpPArNwKlF4WEIHyMGbyITeUFrPAZRA1sciWBrgTninAU2BzKxQfihCIEkrMP7GlO6GgFBQ587M5gccfB\/qXebiQyT3l5NGrkNyb8MSVEQWWEmXffsRk9TvAvr9k0PBxlxBXYL7vh+WHtGvIWaSrw4pW8f97lDnX5aFswRJ2Y2\/NVu5mitQG+eeeCFj1Z25\/zUkqN5asCldwWA\/\/YJ+1Xmv29WM7lzhoqezlwBkZl62sV\/wjl2+AOt7ghn2lDLqznhyW+TyXNq5tzS8WJt69WTr5b01V7uVEwlmCfl3YB\/iRrFJ+YOkU8RF5ByehnQuajL5je3K78mb4Pf6dS\/SnhmHvHzzxmf+MjSkNZp7G9CVzMZBZGxdrR6KNmezZrj4tZf\/zPBkMqbTz4PopW7xw5YQmSXDaqIJknCl2cTVbbIvrhKJtxllEz6uayNVk2o56chbPeD\/xF0fPqMYZf7hHpc6BuCxw\/dcfmFQoQQRYM8f21N+NcmYU45+NV4OHMb6\/OElMaFSocxUbGN6R65EY8RzqZNm3sKrdCy1InJ8Cs0zjCR7GETYLJenLH+teKgw8k\/78QTd6ttbsnKeEz6waDvVIC30X1Svw5P+0zLRRjkeagCIHIMjj+oY621zd6SfpAI1AiaUubxLP7cDE6HnIAaw57yosBjn0NixKA\/TKF1vFln+N3YkXWk0u\/XUBE3iw\/GmlAlB\/o3W9ZGWKI\/2wLq290shqJkhlCITZhGx6c+Rrs3kQw+poNK+2iZyFmjx8voVAIithePradWqZRnGUQoERGCbwyAvbIhzYbmspE718hMtvxZfgCCrRA6Vua1K0zw47oHWsBc2id0T2RcGJ3O8z82pBUw258aIK1tRoOTaQN5caW2UAPM25KkUINScDKYS\/WpyfNVWs0e+OdQ7DLInsgml3TTkggSWDSBjk03o123O0I6n\/VMzJSss+DPFKUoxL9rvXnATmcVwq6r5h5h8DOEad+08Q418eGvDgvc\/IIuJJSs4DBmScyOYg7v\/Nuz24xru7WbjRJ0UgtGC5TBod9kuu6Lm5R5fBNDFDUVGAVbHE5gLPf50MRJNOC4RPVB2tNXQWaFBfS7cFrnbnf2IRY4drEmSdNgkt\/teAFyX6OgqUWvh1vMlm6kdSrbMytwClzODCmkTZMaxWLU2xmJK+4v89aee5do0th91YeksMF1kiU5VUYF1Ihkjen\/JV9saYjiImbAl7TaUBdMqYxBMnqg9WLi0kfeK\/x2i06kb2vZSiIr6s4dAJsxX\/9EDTHPcS43zT4JjocqpkA\/tY58gUBJ5\/2nL4C\/qSjMkGdERjvMjDqQRjGI7tlib+SCTXrahlM\/IpNGHqxpMse9gc2HCpqoIV1cdbbml8iJ9VSSCCqCUWMPzyy4DOZ66h5B7G1NaorBdEi\/VCqyx7lTfZ5h+lbLhyAaEjtukqIKqIUKDIe21kM\/3I\/cZAoDbE6vAgI3bs4vxq48+mUmhulgCJZSPM4esHK5fvXr8sYLuMnme66ejjp0rPx97Q2QIeQw7SNJsCtF4AZqyCfyOFDrrJngP7W\/\/wr3l28jjh8NsKB06\/gxLhPyhd+VYrayiPPloHLbNVq0+oZs0EQTxNK8t5NKiuUf2EiLL9aAwuzK1gm\/fjoXsL0pORD5sc5H0vrYfnmp6d9phhMbGz2nXZho9yZxxbOspNbkEyMlzsJXlikAgHGdjkLSqjjxTTX302OZxOAg7wpYKgxNwTvlzLx9NlWLl675N9wdHYZgYwaiaKsof0M+KXG5nnAdcYyxaYNQFOUIeDjnQGJUoOgkOrpuwLlZ6Sw2W\/EHtPQsCRqxwha0TiyAIed+OEiYhNmmKQqb3aBQBoH43esjWnPbqxO6toP\/CJ8BFzy6U8sZJdXR9ap0Ii8QJhXDhJIV\/dy6x7KnYmc8724vrcbMHX4BTrOmV12F4EeeTCHsQQGLovaUSwIA1DhrH1hbqtuxomNW8SXzMYDDuRCVSq\/CvfnRKn\/PsHfTqFm6UeUkuusvXPrH6PtTfLsHOijO8XGT+59COY4Q4RUGMBDuMqfw0RnR2nsGhZdc21dNRAtt07WhpsF3CJSo15jJXpaGWLuIl8el2lWDbIcTu0mcspeTu14a5gVn0c2JkICQLrmftmedOhMEamxYWF6GwQpC7Ojbl8BdigYg9unMNKBozIUDBsOSjmuw5R4MkPEQy0LCZgSUfCdlohw1JLujwK3gDo43g6GGXf+je4cr+Fz7uw6rHC2YIOluSzpb1\/fepN\/DOP9\/OgI5vIY6sMIEsLavbvZ0cNx2ttEqKx4vj82XvpCpuVgKdvx0EsiVUpaR9lzVmH6\/TF1AVrgmAWY9LazDjY6yIznrTLdnvoThx2xCnyKBOTY971ZNbii3wllOpw5yOrBW78wO5c02SZvdnNFN1ev6ACJVlqVUKQrn3e\/y29Km1AZ5EV7KE4miZQqCANGggYuayuR\/jJly5hlMkiDpjt5o6dlkAHcsMUmX5XAN2prJYYOSeDebZ3zyFyMiECjuEfSsCTO45lRlvegRQeqaqsh5D2CW8nkjbapxu4yBwIhntnq9TyHY\/Aovg4Mu2FjaoAj\/HD1FUJMFQW4k0fInTAFgt2vH\/ghUy8jIHNcPfC09+TGfcl73biim7oIt10lSUBdNcr9FSjYfAuLBoCM60U43S7FF2ZVXPEkaHsSi5UP+8E0tHScxiLf6gojnk8GzgoOHhkN\/0Oo3zFp8kkp5Bqt+Hl3U00czTbOGRORxz38Kd5o\/c7MN02C76q9TdRB\/DfqRZ3gSZJZcfz+0JI1MPE9vejJiPFlKAJuvYfUtrP2L00htkmGI49mGDwlG4rxLzKfUBp1A\/SrOBRqSAKDF4wzgtVWx54ScZ4JG01hRDI0m\/FIezZZVpcBW8ayNxZMZ6PpsWqC2xb8j\/C7CBKw4w==","iv":"1afbf8d6795f457357831e293077c836","s":"70a6a29d3d2fde86"}