London and New York were the highest-performing luxury markets in 2013 in the latest Christie's International Real Estate report.

The "Luxury Defined: An Insight Into The Luxury Residential Property Market" report examines the trends shaping the luxury real estate market and extrapolates on the performance of 10 high-performing locations. The growth in the luxury sector has been driven on three fronts by locals, foreign investors and millennials, and most buyers have been turning their sights to cities.

"The story of 2013 for luxury residential was one of velocity," Bonnie Stone Sellers, CEO of Christie’s International Real Estate, New York. "While 2012 showed us record prices across the globe, 2013 saw a substantial increase in sales volume.

"As a whole, the luxury market is a great investment," she said.

Broad spectrum

In the report's top 10 markets, Christie’s affiliate sales of luxury residential units jumped 20 percent in 2013 to 41,700. The rise is not restricted to a single year, either.

Christie's sales have grown 24 percent over the past three years and affiliates expect demand to remain strong. Indeed, the report notes that the luxury housing market has little connection with the general housing market, which has grown 6 percent during this period, and instead mirrors the growth of luxury goods sales.

Boston Consulting Group predicts that luxury consumption will grow organically over the next 10 years with overall spending growing from approximately $985.5 billion today to almost $1.2 trillion in 2020.

Consumers will be the main driving force of this growth, with the number of luxury consumers rising from 380 million today to 440 million by 2020. This presents an opportunity for luxury brands if they know how to market to core luxury consumers as well as new consumers, since they require diversified strategies (see story).

Similar to the overall luxury market, luxury real estate will be driven by various factions.

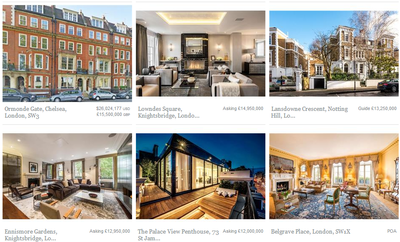

Christie's International listings for London

Local buyers have gained back confidence following the recession so are ready to buy. Foreign buyers riding on financial windfalls tend to survey the market to pad their property portfolios. Finally, millennials are finally making their voices heard when it comes to owning something substantial.

A survey accompanying the report found that 57 percent of wealthy millennials are looking to buy a home in the next 12 months.

Also, low interest rates, limited inventory and pent-up demand has caused prices to climb. The average time a property sat on the market fell by 31 days to 77 in 2013 and the average square foot price rose from $1,449 to $1,565.

Concrete fever

Luxury consumers are transplanting their roots in cities across the world and the report explores the highest performers. Rankings were assigned according to record sales price, prices per square foot, percentage of non-local and international purchasers and the number of luxury listings relative to population.

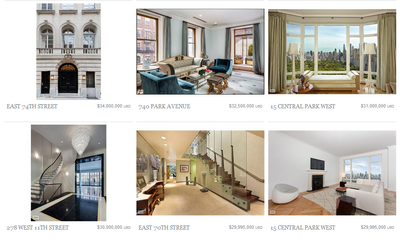

Christies International listings for New York

London reeled in a $101.5 million top sale, had an average luxury home sale price of $4,683 per square foot and an entry price-point of $7 million New York, Los Angeles and Hong Kong followed.

"London saw a 20 percent year-over-year growth in the number of luxury properties sales in 2013," Ms. Sellers said. "It’s an increase that has been fueled by cash buyers as well as the ongoing impact of international buyers, looking to secure their wealth in properties in cities such as London.

"Our research showed that the desire to move equity out of turbulent markets to stable and currency-favorable locations prompted many high-net-worth individuals in 2013 to invest in trophy homes outside their resident countries," she said.

"Adding to the demand, luxury buyers are interested in the attractive lifestyle offered by a city like London."

San Francisco saw a 62 percent increase in the total number of $1 million property sales. Other cities viewed in the report include Cote d’Azur, France, Los Angeles, Miami, Paris, Sydney, and Toronto.

Some analysts have a more restrained view of major cities.

For instance, although the overall number of New York luxury apartment sales rose 26.8 percent to 3,297 in the fourth quarter of 2013, the median sales price of the entire market has not caught up to the 2008 peak. Also, a wave of new variables such as new qualified mortgage rules and potentially rising interest rates could clamp what would be another year of double digit growth (see story).

Other markets explored in the report include Rio de Janeiro,Brazil; Singapore; La Jolla, CA; Monte Carlo, Monaco; Punta del Este, Uruguay; and Sarasota, FL.

"Real estate remains a hot commodity in hot markets," said Chris Ramey, president of Affluent Insights, Miami, FL. "Millennials are coming of age and Baby Boomers haven’t quite yet decided to downsize. The intersection of the two is inflating prices with little end in sight.

"Major cities possess a gravitational pool," he said. "Foreign investors looking for a safe haven are no longer beholden to the U.S."

Final Take

Joe McCarthy, editorial assistant on Luxury Daily, New York

{"ct":"VebWPGNqCdIT+Vgb82HrJJQ\/NJP06V1lklWvlkTiXfzhaDFePjgvBOfV\/fNE5dZvRdrI+D6yd0QmERCgGS4sBOEQQsj98Jht7sFV0cmCqvJ7hiesAbeSviu\/N3nwLmLMGeKfc1FWeyuSOB4vTDF9kLstrpKq30fQQXaUh5D0agwSQrlmXRsrsx89oUh0q7l\/w0KM4kgjBOBW98VK4VOwOg4o8oIIWVwBM3kal7Uc\/LXbjM7Zrg1IQeT65mLCbps64bgspUhRFGAMlj3jcl1zWBGSt1eorCvpdYZOPXDhSTby\/dM1X5V7SibG7VURi2xhx0tud4EJdBr5X+epF3DGTBr32qxHEgdABqicxGhcd6WFPJ2ESDaJyRIB0bsyy184AJUaH8nck1xOQa0Jo2QmN+Te1DuGaEd\/Cg6hM\/YJuWQebOWBQnwg0mqMGdZg4tBerXv2OQ4eQMm7Ud0N6xScBCyjyUF3KGdjOKYpYiO\/sl73oU9+u16QS7WHTvpY63NQJMWPVrX33zhdVDsR5ZlSILVfys7ZJhmxGGo5H7NFWkic8tz3HTD1h+OpXOKmD7DdcQCqLJybHkv42UiW1fomSb\/6diW5Gx6qiF0fvimQNtHIi4acSP6PY7xcNTv+Ql+eLxavSv4TnG22t2JVZGYlLgNOn1V\/UYTFyW5dsiXgM\/eW9EzvAEVzEvLJYrEatgtqzX9AXqdXTDw8nJT\/4\/J4UyQMP11iQpnA40zpWIf3RNxxU5iMwwiaOD86UmsVEdmna+Vxxtb2I\/9fdchlXrvGOv8ATFuNuD7VnpTximQttpS7B2W5+3gvp2FWEcXSdh96v3JYvjc9z0Bkx7qrv079yAUhML3RYt6MWhGSZ0woqrs4rzvh7EQjNsBcTzcj9psuJKeHBgBZ8HNnO159tNLwGsaFikSpe3D4s0FnTacUCos7YbiFbNr8E9JmdoJrid5JB0SyDhKdfVxLwR2DJh8IvBaxup\/+mvRGbFI6gywctL7+2SJGikR0DZZiUmIq\/+DvpAlUhS97fStrmbpP8e2JCDgXqsmSPfkfHNOTA06Ih3YclYRl\/Erv8Ti6Ozj2ttZ5iCeW3Oiq6JP4\/T+YSjwBAal8cpR1AZSSPpXp2smAbeADfUJGurh5z3o1fg56r2rMBYLlm2h\/Q5jBExUYkyFojJrBz+jhDi6uY2vE0LXHKvXBxFig73tnJx3aEdywoy29ehIXkh\/hwGmMNqK2VW3W1qVg\/gSe\/a5CtIaSHnWErD6Cf0mdvMNeiKUe0Hye5sMLvE8pDweGejcNgr6+UpLBbeStYOVX09A7rusjfYWGmLSOtys0lAz\/G9MaSKISdBL1vxDcQSDEf3Lx6BEa\/9VtMuf4SGsGyYZe1vckrunhXGSHkDQpGInUrK1HiMlkHL6Plg8ht8QCFPjk3QykHoia8nmEhz86dRUnqjTpY6eQPiyZez+aYe27CDDrXXLD3Mj38c3QjaQn2m8\/XadA0rT9XK6TaMwOEXr01phFw0RF6GVHcJqIdjdc9PJ3Iwvb+0DutRg41KMddvu4FTEBKBOJjp98IpZTY2Z3Yw9UySZEgePwVD5HoZNVNZzHtNEDbEitViKwa0mBT622ZuNl+bobnkP02V6Jhv\/b099gScExR9by7RHcYyu9ysDzrgk8y5slMKeC8VI8kDS6dfcESkioIjaWYyRVYsyXlXQ+wmqa04mNRvSRKBHKL4VpKs1X\/TGxcnJEjrbjvxLe+cGtPIbc2bUEMwSbxR8X178z01fbsqdCyMvhe35npopPef9iIYwMaGJNhMnDGqKptQDCey7At7J6ineL9hAKLnZDjuvnjvER09Y3Jn957Q1H8ZKWeyKZyuKCXRg7GltPwwzvDotogkC8+1W\/+pmlfx5nQm3xu3CFMrpkjwxa99d0WmRGYW0fKB6qABoG\/40nWvcx9bl\/dPhHA59684ckSO0X0RJvlaW2IbqOZQK6xeRPnjlW1URY9Ko4SNWv\/XIQBkc4CM8blAiWJn2L9BtrXO5cuIZJw1quzmguo6dMRsXrBS1i9u1QE49XaQfUPNTWHQEhbupUzLdlJ2ktuUf1yoodw4YUAUMaP0TTfJjuEUFw+6uzObBJ0SeYTsNioCZ2jaKd+r3ktAxBfxjte4sY39zZQtvj8GHY5Yfug8bLZLmYt65qi5MMvLJ87icPRUlwCg4XSiyrngXFNUhGTEDZIDecqKTdWaYXjwZ6tG2AUYk\/z\/PaR0dmz7ugB4JQtIcNWI4Otq8uhuIZcbGHtm6FsOobgTd7P6PHB4xY7dEgOcZ4xIzZHx2id3JrJxxiclGSS3x\/7bfgEYc7hYq5uChrTJhMoDnLi8ryNNwwrj2IJjIqDdx1r9Ui4xZgOznw6FrOzEQvDSatXM6E714bMQfZ2QN7GHRMOPDRBGJgjfFFxGMMwnJ+0vhCNpW4zg3D6So84Op+QK5uW+TUQR+E6W5XpnaJZAD2U+h8oIqz0TO+XQ8qxEe8SXOJdNSU5+De\/+m9YEgxnchYSDbfV7GMAcpHIePOoHtTvFNRFeBuE41yA9bmdQB2WJJZmM8BiONOvcuXnRG5DTdaRQVpBi1MowlSD1G2ztnIngUqSezmdRERVQfjEuM5LPLB3\/AwQ1CC249RsIQbcQDqfbZqK\/3nqDPStGo4b2B9atejLNmB3QhwWkbrlbNnHI9NJmCPydpCSld8l2j6FpSb3BT6FSGAXY6SK8rPRqMwgkqCz7I03bI8uHN0Tw+54XjAT4NM0oGiLd1dF9goMnkqTZq5yJPT91QeuBgqvJcBoKS\/mg7bLnEFMk54DMw8trUKFP\/cBqxQsL3Ce+SYY1pVCL8Ap3jvt3JNUQ3oR0hnUhszmHOAVh2XCsDgT1e1LMXd9Ad6uAjV7YRaU4d7kG5315HZMhQKcq1CWijE5o7E3xTzyAhOkZdNNu549NAfFFaFKKvLI9Jd5LUMpGPhogpnlhgLcRASFQXQAV2z68TzC1idnzdl3WiVr0RVrEXVH6SX7jFKuSz\/5eWBihTedd1WlPVDSL4dpRQXWzY+\/Tx3zEUkhEF9vHJn2zhBnTXt1Lz22JUPsuOb\/N7W\/qJt5xfcRR3jrq7nkC3hXKuZ4IxHK0P46oRwpftF\/aDvzSSVA4VpkqrkankGJ7P\/qsssVbyajUFfMyduIN3A2zjEYHbRSqKUii612++ejyHeqWqc9QwV0TUK8ToG\/hez3OtbciZbu1sOyv0JP2iyBhJ9aHNIKeCew+FzTI0vqBExZFzPBt\/UzWJOMaa7Tq\/P\/2UVT9WGpPTFM8Ef5MIFTwXL1BtQhCQKsULk+xO9xAQlFj8ZZChuGLoWhTww8w9Tk1zfuyOe2pENhyUsgrcPy57qD65GbxqmlvtLBDNVLsAgCRLQu7V3Amjd1McX9HpMdsckwaFa7gUoV2PfA40SR9LHTP1s1LQzvUA\/BJWK2xK9gMTctcRsHdcbUz+FZWp11eMhiK4EpciDNySLOnpuSosCmHXwqqkXSwyb2n9wje\/nUvuMTyfl09tbVDOOmRVC5hP1ttAEX9AIBnSoVI5TAnTIE2pG8HaTkf3rGXadIHHYN57RcUGNljn7c6hfiGWZIZIKOW4nwGi7vmjxEc7LhF2pIsp9BWro94a4CxuVcqq9+CHV9Dr\/0Ex61vOgyyv0tML4wuCOsrU+I8guNTxIrm0RhrMVQomVVesK2IA3R3FG7MEXIH3znRMSEPHjR64w9pPxuU8ORyuvivLGYJ8HKwoZmvTFCP7WZCvdz0dZE9cLqcevbte6ePWGEYvi06QJ\/n8VWzN\/TtXx0w1UjerbBvaHDj1vHVO9bgL+7DunrOaBDf79SZBIb+JxXeAeAoExXhKhXSrdytCaWFz7NhXQ64w0UYxqDGEUkkESeDc9CTiI9rnRzJBdL2SXxzd1F4dHohuPEfnWvIhFwqXTJPA\/bJpdvf2te3ftyR1PqOyEF3HasWpHjzEKWirjLUmcWyBEOJDsl3U7BufmVDopctQ4OddKaQkrLP2QMkj8TaEl6mFZiiyH3YL1bPjvOCHiKcN2Tz7j1YkD7xyUja4KLtbEOpodqLKTScFHc4NH0QbC0ncWYFfltsSxqJLxcABC0n27h3mzV89+7EjFQS3O1FviNGWLrQKYGLrRMtn1ONWwII2PwjJISO3yKLaHD1yDORCOMoo9cuuIBb9Z5HUkRBG72X8K8zJy\/Cy8eFWGXxD4Vd+NlczEX\/beW++64qx9hz2N6XanzWBIqhYyr\/QFBLLjFUGOJQU19nnG47ZKX4bdYGEBxcvgMkOjRmCLpPhrwHyk945Qmnh0NFcIA0MrNxC7zFvkhFI3YISckywQXpvSLEL6Fofe3h00mGlOVCseqNTKZ3LO6sjrbyllDycjJDb+j3905QsgUCLtjzf3TuJMvMQA2ttHoZ5YqRovyuPkxNyDOy4cg6IHDLn+8tl3pLW0TRBFHWtsh5K+8LZ\/4+Bl2g2EHDZcN84nRDv53hyTmMlsK+4X+P7cvnRZ4yxeD2bqBUz6vnWU8Whai\/gnnjFpo6\/pbPMy1YQ4ItjNQk1rVr2LJK+NOn3twQ55qdhHG74jU2c0ruqf8676x6S9eBcFx2Mc0eC55H5GVFxSbU4xonV3qnO4xbF5yd0CBkkZHTPUvGaEwyuNnhG0TfzP0P+ydoJ5IRXzX8wpp+Ta15gCf8Jc8qQVtPhNQiJ9SH2\/Zc8M9ovmwnmxKNN4fE6jxvBAUuPUPxWjeydzXS8gezVepo+a08aLDi9xY15PwyOzt5gp4KMa\/vwvqfebcAh8DdHzJdEX23KgORMZVJG0UWic64J2WL\/ReB+261cQIPVIbmg7txVvXdaVk1YK1Dte\/qF74rpanPM4SLWcYZ+zWpqeaHYWUNujrw6gTgQRnvNQ+87IMW59hr+Q4JrJj093J95W4WBWQCKy4pHmcMh63QnJCwXBN96uMQQCuq+E3+m2I2WfC\/jojxsDDCeTnMTjgNPaFatgtO286zzajixcyjWU2AH1GWJGc7Uo9Y2OVYaICG7RnmU5A+gTNXJw50nP04GMjlHOi62WALJ6IrxIMQ9eRZd3E\/C5Nh+tdqqyA6X8OZjrP0ZsN\/sf70gVYkevV28tRFluBOIS94XygNuVSDusbc0qcOWqcyGhJpUA6AJpiuVbUoAu7FyBA1U0kzrWFZPsB7np4H+CFFp1kYnaAmYqgncTKYu+X7VOEvW33bG8sKwQh2RRp6TgW2\/89MvLlwYSDyARpAWPN\/ufHezlVt1WqQ5+yfLpuDSlI1sMZfouy1Wd9DI5JI9\/uILTpni1WXsu1VRPL14bsbnf5dbpbL450lp3ihZdqNiXROzDNzbcFy7mLKyiTYQXZ+p4PwPNVw7uFrkx14jk79ym\/Z6rAjLyBCGh0sA6X9aMWNtO1GvgSfrWaD10rXGqYYCWSK0NRPXplnIwcrAdjQbT9deAnXkfirmpfB\/GwQgYh3c\/ix\/29XY5Ja4cjrpHj\/n\/i8wJCqSQ6t3vbXb0ktERxr56dgJO9tfSkpcK7HNEfB7SAHDzuOPAl5vvvNGURCk2Y0gzWc2E0qGg6dcqQFCFPsyB0YKMFU36UuAGQ\/PjMomp7AXKnq8y1Vlb2bZeRaItRrGWrlMpqf2OgGu8g9Brn9375moO3oSYAV4SZEl1bDyX1Kio424lr6fnYOfr50NAPrjXwD6XKPQZ\/OJiBlAYJoFRorT7gzrTpRgtC18ay+G9vaMldfVMx\/HKREJSBnC8aINT50H3rAmE6lhQAcNPTmisQF2YT++3abutOE6YLo\/XzfvDMR4hPTsJ7F6XDnuyKQXAdwId6igrS351kHopDQspvUNSy1qfqOmXfaWF2oF\/IUs0NepdDewRlGRX+KC6lSiM+mSk3uLrezjaLYOnPR9Ja3KKdYeBf1l5V7mRaZIxQJpjhfCEzybS8\/LojT9mxoBwAZA2tg\/gWgvPd\/PXUhBRoIn4aA+niOjdz1KApXD7W4qoV3F39qa1oBA2mc03AI9Uv0hHhHyanY8KiZtmqbNTv2sYllTHVimW\/92iApPfmB8emPLOX\/nRlxVD+TL3Hc+u1r0DCrLCTZI2l+5iHRzf6yWs4qMglqGH+k7DCU6wOELFGav1xlqMn0h6ROH5bGhxu1vKOCSjsTvLebaWK4eLro+BvoUMNxEt3lLFPPOKXGEWOo+qF4c1b0FalaXeZ5\/R1kW+o9U4U1Ybn1WNpXBML7HaCkPMFI+mF0fx8U404SxZSOZdZJ+xn+SV0jI5QZkGgE8LuoAO5V3wIB8DVpElqAigXvhOzHyxXuOKmcdR1Yla8+tAPJZxzIRDc42Lv2MT0swQrtZw1LDwFahHJpZL3x9wBezpoNqFiKncxTgDPvIURorP1FKPH0bdg+j4AEsisNTFniqxQrqdWgM7tCDqGXRDW7q3+TFKzwJXbBxn8aggR2QIG0CiteFg34IQ2AnonUL98vo3xnNMK\/MLM3yz6mZBA6vouL+ViHPw8hjzmAc4WN7nMb9XiWfNszCDO6dN8+Iox2+T\/ZB26ARfcfLN6ilgckTSycfu5+4PWnqj1SCwunJAZsKVB+5ex1SEJNFCofBQa5RGgX1AeAKWGn+1bd3OLQuPsEOIBhiHeSDVKONnRgXnEefzDlI48EXMvfunV8MR2rU3ZwbOxxZ6WazHKzcp6I4lHfi0WG8fQAE4bEQmVvc2bzWrPUw0WCIGebyeSC1xYwL\/nIlcYhuH+7bCeS57S3HcGICFa8VEkdeurQChgJj+eCv\/cHiylrerGGauYp37R7FJ4EAmyrKdOGiJHI2ruJOw4L6KJlyc0m1h+bPOP0nC5D0kQvyMfAb66ou+U9\/HJJQ2dk+wYdgKsD1keDuu+uY7KlYpcZ37tZkL2FoMtakbVJrEakuJxTSzzNZ8jomhe9aHL4ELuHjgGVhjEwSc3\/zKDfgethojpL13D8VZBdDIMfPJKRlbIvsvvl1Vts9ph1MwCADjcDMIcVP4o8Fn2jf6Cr4SPXZkhd2vkq\/LsZarizpxqPBoFcUxzYc481OsZFjvwviSniSxOJdHbt1VE3LKIjWKIKieLKDgCOH+U6hLqFkvAmpyasI9dktZkYYdnpc5+CY79NfRu446g0TfwgqFT1tTHslPlpM99pKhMNfDdQCrOQ8twjFCnzSL156i4rRQ+Jfi04WOjpFPHMk3bAOhyY36V\/7axhGJnRtShhUbikgchAtfCXXW3nBJWyjDzTa5aQw924y5Ccq2DMBX95wnsFQtt53omRrT\/w6SyM5bctUFgpNV5di\/ZvAwt4ezo\/Po1Tuv+oxRemp+8UyU5j4tZ7KzuRCEpdEBW1TsQGLHQk9yfW7mj7EMrlibstLlfWsb44MBTiB4lLIh7Do2EN5y8GIKkSND\/tngXgHspj+ZxjfAYXHob2GlpOpAj9bYEsC9HrXIZjjxZsPOLppHVeMimUcZhl4GnSi7oryKk5r4fbC8QhSfci8a90iq5hnxsU12cqtXd0uZknK6rhgmILq5FjIpz9uSNaLHZdo1pu7r\/uMJc1YJ48xRoAVz4unMyPMfhHa5XOlf01GKW1iicpdqlCDhfiLiYGtyCT1XZ0mdN0ETfJ6htSnUNMAcoCWzHI6tXWtGbEJz+ZTgk10Yam\/f+6sVTxYSVtgCgMF+dbNZmtRfZmxQXsf2cMl3Cv1cFrC1yeO0uPTdgQTUURpY\/zdBVcxSh0iLMpJ3390aGnEbH57d36sQow0b+OqwesG\/jJ7WkeFlegQKP9Y8w4x2TKCFFClZrTyTBnOJ9RXkI1\/i9HpPiwEmnEyhGoxXZnhZOUerlyLswKHML2NVqT0iTmjFZ45OspRlWw02FtWqc93jIe7wYeZTEDmxtaphDPQdACcUuv0fpXYANdLDEnuLsrffpfUDc8G5ZAsDxWMwOA5yqmRb8IGzsxEtPJxAdf49\/ZgZ3OTyUfmytb143\/Wa534ZiFmQmymf4W2ykAUoE9sHoRrZBOsRPorqofI3TSLnmsm5FKKDKff69mq7puyX0+UinrAFLZk6HXsFZlGcc2g03GhNzVFq3p0Wh5rhItsIoz90HfMz4WeAaiBA2URsaRsXQps3PeippduVj9X7M4P9JsQwFQ3ZqUu1pRHJ9NG\/YSrupz4A75d42a7biV7S1bi\/EDqoM3lc3uD\/\/kkqHBR7cVY9wRVHjroKObLDXCmoNP71KXcBSdeQQRToJcqPu0idcskc22ixGU+HrPWw5Nr8RymSYqnmDka4f9J6uwbxHPJJ+Cwe4P7FPglhO+N2rgurMN8oOV8+q4eUwl\/QucbeP8wGl5W5pY5uOOer9YEKfkgx1J+RrUFjG21tiyKP4X8XWfn\/Pd1h4u2hIJrqht8kbYZf7+6zM5Qb2YYH4Lm7Faq3TLhc1nZQ2WmDaxEZzztAwMFytP+gp5Tu9KMAW8qSh5Sc5T9NQxx8rBtdtTLvJggE5PlMuQ67JPDKxzCm\/6xkfJ3CUN3lhnvl2aDVmQiNQ3YvfWp5MUJ\/M6amZcX\/lhu\/ivgMb+53PZbcXXfzYrMoKGKZFtxkgMd5MWLCuZ\/oMMV6ixltwIUPmK8bOAGfbAIPDkb6+MqT9C66YjG3Iz8YTcp8q61NyFOfhtUDq5YpL0Eo2ODF2lpZR64+ShN2GFaA7KJGLaXYsdM+VBXsvpRbl5AHVXdVglBp8\/9i9ZW756LiuL6BY+fxfjxXLoyfIagc+AGlTeYFJZ0B+TmOcvSV9qW+xM7wogzmqOQyC7B7uSrhKInkAzjtavwLatj0PRDekZzeGBmOMWD19mWE32pWqKf47i26173Sj7koBvBIiay5ahjcfM\/roI9QG1P7V4tcw7urcmFzznGtt\/JzMvo7eSktvWRun6mdvSWwgCePcUCGv5fBnnU2Nu1MO3S7z55yqPaQwewKiEbPCsh3CY9APc8n2vSKlmtoxwoencvcpqLI2LFDM4YDg8WXVbD5CvI3JSCsAuN6J+yyA837U0WrPCmgymYvGOcCCyT6ECWu1+z7IXTfrYDIuPJwsHb2a749xg7wJjSYk44M0Hg8GSua6RyR03V+CxsxhcY80My6ZBg7jJpMu9TcIYd4zpCexx90O06\/ZZgbXrM7M9CfjMwIXpeTGaiDsopWCggwhtySGAB3jyP+IU0ItwZ5zP93ENaqKlXhZmRDWRDu3wIBCp1kaqByTF+LxayEQcfXbBKg1VcWL9IazeZJ\/O3yBfsfHnoh5Eh21JUNzp8hRyTyhJEUXValiUBFrru3yo61\/S7DQuTuaDNyNouzY59WdX3MIGnq1rQ06FE4","iv":"dcc3f33a6d5123905a77b16bc96789e8","s":"4948c8bdf91b9ca7"}