While many retail strategists stress the importance of emerging markets, these regions only comprise about 30 percent of the global luxury market, according to a report by A.T. Kearney.

In the 2015 “Global Retail Development Index Ranking,” A.T. Kearney released a special feature, “A Look at Luxury” to understand the rate at which luxury brands are entering emerging markets. After a challenging 2014, which was marked by low economic growth and political instability in many developing areas, luxury brands have adapted expansion strategies to succeed in diverse and evolving landscapes.

“It is crucial for brands to develop a market strategy with the long-term in mind. In many cases, initial success in a market can spur quick-fire expansion, with the risk of over extending the brand,” said Jodie Wang Kassack, co-author of the report and manager, retail practice at A.T. Kearney, New York.

“In luxury, ubiquity is the kiss of death, so brands have to be thoughtful about what level of presence local markets can sustain without damaging brand appeal,” she said. “For example, in China, Hermès is the only major luxury brand opening new stores, which we would attribute to its measured approach compared to competitors who have become somewhat mainstream.”

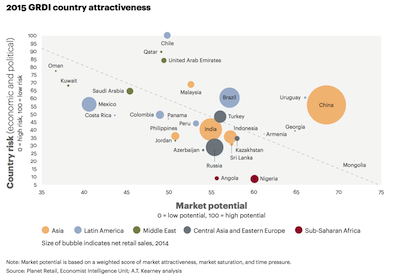

Published since 2001, A.T. Kearney’s Global Retail Development Index Ranking (GRDI) ranks the top 30 countries for retail investment worldwide. The GRDI analyzes 25 macroeconomic and retail-specific variables to help retailers devise successful global strategies to identify emerging market investment opportunities (see story).

For 2015, the GRDI featured the special report, A Look at Luxury, which includes an analysis of the 15 leading luxury brands and their retail presence in the report’s top 30 countries. The analysis does not include department stores or duty-free outposts, only bricks-and-mortar presences.

Global goals Although many brands have retooled their retail strategies to focus short-term attention back to the United States, developing regions also work into the plan’s long-term goals.

During its examination of 30 developing markets, and the 15 leading brands in those specific regions, A.T. Kearney found that emerging marketplaces fall into three tiers of development, each with varying implications for brands entering or expanding within the area.

Generally, when a brand is expanding to an untapped market wealth generation creates those opportunities due to the increasing number of high-net-worth individuals. Also, an increased population of wealthy consumers acts as an indicator of the “ability and predisposition of local consumers to buy luxury.”

In A Look at Luxury, A.T. Kearny defines an “Established luxury market” as being a “developing” country that has the presence of 11 to 15 high-end brands. In its findings, A.T. Kearney describes Brazil, China, Kuwait, Malaysia, Qatar, Russia, Saudi Arabia, Turkey and the United Arab Emirates as being established luxury markets.

Oftentimes, many of the luxury brands in the sample study have long been presented in these established markets. For example, Italian menswear brand Ermenegildo Zegna has been present in both China and Saudi Arabia since the early 1990s.

A.T. Kearney's A Look at Luxury infographic

In these cases, brands that have a developed presence in a market must look beyond tier 1 cities for future retail opportunities to avoid saturation. China is a prime example of this model.

For instance, China has an ultra-high-net-worth population with assets greater than $30 million, a number expected to double in the next decade. Also, Chinese consumers are already familiar with houses such as Louis Vuitton and Gucci and are now looking for “newness and less ostentatious luxury.”

Due to market saturation in China, the “days of rapid expansion are over,” with Louis Vuitton halting expansion into tier 2 cities, and others such as Burberry, Zegna and Hugo Boss shuttering storefronts. Only Hermès has maintain its growth, opening its fifth storefront in Shanghai in September.

For luxury brands with less exposure, tier two and three cities remain a viable option in China. The study found that at least one brand from the Luxury 15 list can be found in 40 Chinese cities with Burberry being the highest with a retail presence in 31 cities.

Burberry was followed by Gucci, Salvatore Ferragamo and Zegna, all of whom have retail presences in 30 Chinese cities.

In contrast, the Middle East has a high concentration of wealth and an UHNW population set to grow by a third in the next 10 years, but the market has experienced much slower growth.

A.T. Kearney's A Look at Luxury infographic

Given that these consumers spend on average $2,400 per month on luxury goods such as beauty and fashion, brands entering the Middle Eastern markets must focus on service excellence and innovative customer experiences. These touchpoints work to build a relationship with the consumer.

For example, French couture house Chanel showed its cruise 2014 collection in Dubai, UAE, to mark the first showing for the brand in the Middle East.

This continued the tradition of Chanel trotting its smaller shows outside of Paris, which have taken the brand to Dallas, Singapore and Scotland. By taking its runway production to the Middle East, Chanel proved the importance of the Middle Eastern affluent consumer (see story).

Although markets such as China and the United Arab Emirates are considered safe marketplaces now that luxury is well-established, mid-tier regions are blossoming with high-end real estate opportunities and rising affluence.

Markets such as Azerbaijan, Colombia, Jordan, Kazakhstan, Mexico, India, Indonesia, Panama and the Philippines have six to 10 brands which defines these countries as being in the “Middle of the pack.” In these nations, brands have opportunities for long-term expansion in the larger countries, while the smaller countries offer limited opportunity in capitals and resort destinations.

For example, in India many luxury brands have suffered “false starts” due to a poor quality of retail real estate, often only found in “low-traffic” high-end hotels. Zegna can be used as an example as the Italian brand entered India in 1999 only to leave shortly thereafter because it was unable to find a suitable retail space.

Eventually, Zegna found an appropriate local partner to find a more worthwhile storefront. Even so, as of 2015 Zegna only has five boutiques in India compared to its more than 70 locations in China.

Although luxury retailing is complicated in India, brands should not be deterred, but rather build a foothold through marketing, social media and advertisement placement to connect with consumers. For instance, Hermès aimed to do so by released a limited-edition sari collection while Zegna saw success with a version of the Nehru jacket.

Hermès sari collection from 2011

Lastly, “Emerging luxury markets” are defined as countries that only have up to five luxury brands, but may have significant potential in the future. These countries include Angola, Botswana, Chile, Mongolia, Nigeria, Oman, Peru, Sri Lanka and Uruguay.

After Asia, the countries in Sub-Saharan Africa yield the highest projected growth rate of UHNW individuals among the GRDI’s top 30, although these consumers are starting at a much lower base. An indicator of Sub-Saharan Africa’s budding affluence is that Nigeria’s Champagne sales are second only after France and Angola is one of the most expensive countries for expats.

In terms of luxury retail infiltration, Zegna was the first luxury brand to set up in Nigeria in 2013 despite the risks of poor infrastructure, high rents and duties, scarcity of real estate and corruption. To put Nigeria into a larger African context, the country only has about 20 “informal” malls compared to the 500 malls found in South Africa.

Nonetheless, Zenga has done well in Nigeria with African consumers in the market spending 50 percent more than the average global consumer. Zegna founder, Ermenegildo Zenga said, per A.T. Kearney, that “For us, today, Africa is more important than the U.S. In five to 10 years, African can become the new frontier for luxury.”

Partner up Entering a new market can be daunting due to differences in culture, infrastructure and bureaucracy that brands may encounter while expanding.

When strategizing for international retail expansion, sometimes the best plan is to find the right local partner who can tackle the policies and logistical hurdles, according to panelists at NRF Retail’s Big Show 2015 on Jan. 12.

In “To Boldly Go…Where Exactly?” the panel agreed that mature and emerging markets offer both unique challenges and opportunities. Navigating unchartered territory with a collaborator is easier than going it alone with direct operated stores (see story).

For instance, spurred by future potential in the Nigeria’s capital city of Lagos, Zegna is working with a local franchisee to open its first standalone storefront on Akin Adesola Street, which is projected to be the city’s first high-end shopping area.

“The main takeaway is that there are different segments of emerging markets that require different strategies from luxury brands,” Ms. Wang Kassack said. “The large emerging markets will continue to demand investments in store opening and brand building as they are the luxury markets of the future.

“China, for example, will be the single largest luxury market globally by 2020,” she said. “Yet the smaller markets also offer opportunities as the number of affluent consumers is growing exponentially, and even if it is one store in one city, the potential returns are high.”

Final Take Jen King, lead reporter on Luxury Daily, New York