Nearly 50 percent of media consumption in the United States is digital, compared to 32 percent in 2009, according to a new report by L2.

As digital consumption has redefined consumer experiences and expectations, many individuals have become unwilling to pay for content that was once purchased, putting advertisers in a tight spot as the traditional media model stalls. L2’s “Media Winners & Losers Intelligence Report” delves into how media consumption habits have changed depending on consumer age demographic, an outlet's socio-economic status and which channels have been able to adapt.

"Digital is redefining what it means to be a media company," said Danielle Bailey, research director at L2, New York. "Radical shifts in media consumption have torn down barriers to entry, redefined consumer expectations and birthed new competitors that are siphoning audience and ad dollars from traditional media.

"Consumers are expecting experiences to be on-demand, mobile, personalized, low-priced and even free, which threatens the fundamentals of old media companies," she said.

"Old media companies are transforming themselves to adopt new distribution technologies, while simultaneously new media is increasingly trying to become more like old media. The latter is evident in old media hires - Katie Couric at Yahoo and Pulitzer Prize winner Mark Schoofs at Buzzfeed - and the investments Netflix and Amazon are making in winning traditional television awards."

L2’s Media Winners & Losers Intelligence Report examined media companies undergoing “digital Darwinism” such as magazines, newspapers, radio stations and television brands. The study’s aim is to assist advertisers in allotting media spend in worthwhile ways that will reach target consumers.

Media titans In the past, media was distributed by three channels: television, print and radio. Today, brands must compete with multiple channels and screens as well as other disruptors such as industry convergence, fragmented audiences, an oversupply of ad inventory and a lowered willingness to pay for content.

These points have harmed traditional pricing powers held by advertisers, but ad sales have followed the eyes of consumers.

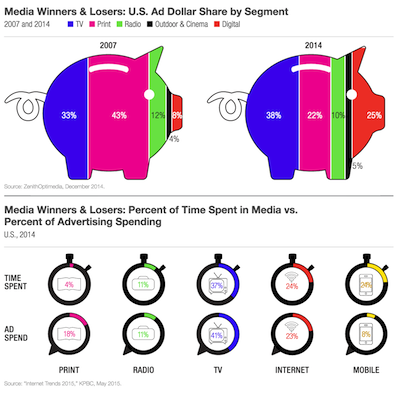

L2 found that between 2007 and 2014, Internet ad spend rose from 8 percent to 25 percent in the U.S. ad market, at the expense of the print and radio industry. Television has been able to maintain ad sales but is likely to decelerate eventually as 98 percent of video advertising growth in 2014 came from digital platforms.

Even so, ad growth resulted from digital platforms as spend moved from traditional media to search, display, mobile, online and video and social channels.

L2 infographic from the Media Winners & Losers Intelligence Report

Currently, there is a disparity between what advertisers spend on media and how much time consumers dedicate to experiencing the content produced for the various channels. L2 found that in print advertisers dedicated 18 percent of the ad spends, but consumers spend only 4 percent of their time reading traditional print titles.

Radio, television and the Internet had ad spend and time spent nearly aligned, but mobile showed a stark difference. For mobile, advertisers spend only 8 percent, but time spent is 24 percent.

While content is still considered king, the new formula must take the three traditional media channels and combine them with digital technologies. Platforms that are redefining media consumption include YouTube, NetFlix, Spotify, Pandora and Facebook.

For example, Italian fashion brand Giorgio Armani’s the Emporio Armani Sounds application is linked with music streaming platform Spotify, bringing together music and fashion in an original way and offering fans access to artists with exclusive performances, playlists and interviews (see story).

Armani Sounds mobile app

In terms of new consumer expectations these media brands are personalized, low-priced or free, multi-platformed, on-demand and mobile. For advertisers these have presented targeted, measured, contextual and performance-based expectations.

Facebook tops the ad revenue list, along with Google, even though neither produce or pay for the content found on their sites acting as a “parasite.” Newcomers such as Snapchat and WhatsApp use a similar parasite model “galvanizing publishers and users to create content, and then charging them if they want their content to stand out in an increasingly crowded landscape.”

Photo-sharing app Instagram did so with the launch of promoted posts. In 2014, U.S. fashion label Ralph Lauren unveiled a promoted Instagram post to expand its reach on the photo-sharing social platform.

Ralph Lauren sponsored post on Instagram

The ad featured an orange evening gown from the back, an image the brand had posted to its account a week before the promoted post appeared. At the time, promoted Instagram posts were still fairly uncommon, but the reaction to Ralph Lauren’s ad showed that consumers have started to become more accepting of the sponsored content (see story).

"Brands themselves are also increasingly becoming content creators as a means of capturing consumer attention," Ms. Bailey said. "Advertisers have been forced into new and unfamiliar advertising environments, and the fragmentation of audiences across platforms complicates measurement and allocation of resources based on performance."

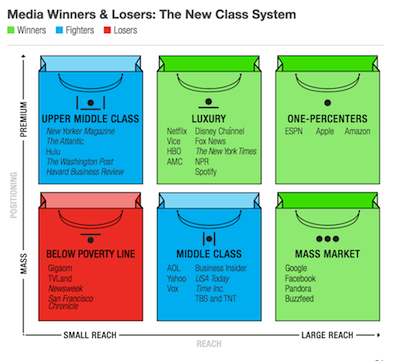

Defining luxury As a result of changing structures, a class system and bifurcation of media companies has developed across digital platforms. This has created a thriving climate for luxury brands with “strong premium content” that consumers are willing to pay for.

While mass market brands will fair well also, luxury brands considered to be of the “one percent” will “defy gravity” by reaching a large audience while simultaneously holding premium positions. Needless to say, brands with “passion followings and broad reach” are in a winning position.

L2 infographic from the Media Winners & Losers Intelligence Report

This has resulted in a number of old media brands repositioning themselves to resemble a luxury brand. A telling sign of this is how paid and subscription-based media have worked to increase ad revenue.

L2 found that millennials are willing to pay for various media namely television, film and music, but only 10 percent show a willingness to pay for news and magazines, a sector where digital competition has been high.

"Unsurprisingly, affluents and millennials consume media more via digital," Ms. Bailey said. "People continue to consume traditional media content but where and how is it consumed (mobile, social) is dependent on age and income."

Publishing firms saw this coming and many focused their efforts on digital channels although that was easier said than done because of the onslaught of mass digital publications that began to come into play. To this effect, print has tried to reposition itself as a luxury product with the New York Times leading this evolution.

Social media has also introduced a new outlet for publishers to garner new readers. For example, L2 found that Condé Nast’s Vogue magazine engaged with social media, Instagram, Twitter and Facebook in this case, 36.2 million times in 2014 between likes, comments, shares, retweets and favored posts.

"Condé Nast does have premium brands among its assets: Its crown jewel Vogue is among the most socially engaged-with magazine brands," Ms. Bailey said. "Yet, it continues to relay on advertising. Digital has also provided an opportunity for The New Yorker to become a global brand.

"The question that remains for Condé Nast is whether it can scale its paying base," she said. "Its attempt at launching a YouTube rival, TheScene.com (see story) is struggling, but the shifts and experimenting suggest Condé Nast is willing to fight rather than fold."

Content from The Scene

Beyond print, television networks such as HBO and media platforms such as Spotify and Netflix have been reinvented as luxury brands. As with any luxury brand, players must have a well-defined brand, premium and exclusive content, strong owned destination, revenue driven by both subscription and advertising and moderate reach.

As with class systems of people, there are also “one percent” brands. L2 found these to be namely Amazon, Apple and ESPN in the media space. Similar to the aforementioned luxury media brands, these three command enormous reach and sophisticated targeting as well as the characteristics.

In 2013, L2′s founder predicted that technology giant Apple will be venturing into luxury categories in the near future to capitalize on enormous profit margins and its pristine brand image at the L2 Forum.

During the “’7′: The Forces Shaping Prestige in 2014″ session, L2’s founder Scott Galloway pointed out that Apple’s acquisition of CEOs from Burberry and Saint Laurent indicates that the brand is forcefully moving toward the luxury sector (see story).

"To win in this new paradigm, a media company must be both a content and a technology company, providing either substantial reach and/or premium content for which consumers are willing to pay," Ms. Bailey said.

"A few select uber-successful companies such as Amazon, Apple and ESPN have managed to do both and generate revenue from two streams," she said. "The report calls them the one percent, which hints at an emerging class system among media companies as not all have the same resources to adapt to digital disruption."

Final Take Jen King, lead reporter on Luxury Daily, New York