As the BRIC nations have become increasingly developed, Sub-Saharan Africa has emerged as the “next big thing,” according to a new report by A.T. Kearney.

Research suggests that the countries within the Sub-Saharan region of Africa will likely grow in potential over the next decades due to a young, fast-growing and connected middle class, many of whom are still discovering their next favorite brands. A.T. Kearney’s “Retail in Africa: Still the Next Big Thing” report, part of the “2015 African Retail Development Index,” looks closely at these consumers and the economies of their home countries to determine the opportunity for retail marketers as a shopping culture emerges.

"For brands, it will be important to establish good relationships with retailers, unless you are a super-premium luxury brand, in which case you have to think about own-store solutions in the premier malls in major metropolitan areas," said Mike Moriarty, a partner in the retail practice of global strategy and management consulting firm A.T. Kearney, Chicago. "Logistics is, and will continue to be, the bottleneck for many brands—and the scale of Africa is daunting.

"One of our clients has 27 stores in Nigeria, but that doesn’t even begin to scratch the surface or begin to fully serve the 190 million Nigerian consumers," he said. "For this type of retailer, then, the question is 'Where next?' There isn’t even a qualified city map of Lagos, let alone sophisticated catchment area data for Lagos, and outside Lagos there is even less helpful insight for retailers or brand-builders.

"Regional players are strong, and consumers like the local connection. So the challenge will be to captivate the consumers’ attention once the market develops, unless you are part of the development. L’Oréal and Unilever, among others, spend a great deal of resources understanding, formulating and tailoring their offer to the African consumer (and Chinese consumer, Brazilian consumer, etc.) Also, many consumers in Africa are well connected on the Internet with their mobile devices, and so they 'get' global brands. Price point is always a challenge, which is why you see small sachets of shampoo and other beauty care items."

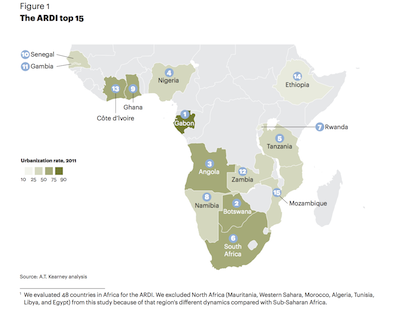

The African Retail Development Index (ARDI) ranks Sub-Saharan African countries on a one to 100 point scale. The higher the ranking, the higher the potential and urgency to enter the country. Countries considered for rankings were preselected based on three criteria -- a country risk of 35 or higher in the euro money country-risk score, population size great than 1.5 million and a GDP per capita of more than $1,000.

ARDI scores are also based, by quarters, on Country and business risk, market size, market saturation and time pressure.

Shopping potential A.T. Kearney’s 2015 ARDI ranks the top 15 African nations according to market attractiveness for retail expansion for both today and the future. As Africa continues to develop, entrance into the market while its retail culture is beginning to blossom may prove beneficial for retailers.

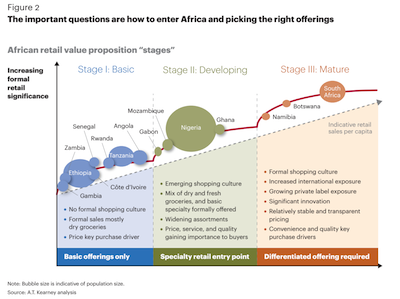

The top 15 countries within the ARDI fall into three stages: basic, developing and mature.

Nigeria and Ghana are often talked about as the nations with the most potential for retail development, but the 2015 ARDI show that “small, dynamic” markets such as Gabon, Botswana and Angola also have diverse options for retail expansion.

Within the index rank, Gabon and Botswana place in the first two spots, respectively. Gabon is considered developing and Botswana mature. Additional countries placed within the top 15, in numerical order, include Angola, Nigeria, Tanzania, South Africa, Rwanda, Namibia, Ghana, Senegal, Gambia, Zambia, Cote d’Ivoire, Ethiopia and Mozambique.

Infographic provided by A.T. Kearney

While eight of the aforementioned countries are considered basic, the remaining seven are either developing or mature markets. Gabon, Nigeria, Ghana and Mozambique are developing and Botswana, South Africa – long referred to as the “gateway” to the African market – and Namibia are considered to be mature marketplaces.

Listed as number one, Gabon has the highest per-capita income levels in Sub-Saharan Africa at approximately $21,000. With 86 percent of its population urbanized, in its capital of Libreville, Gabon presents retail investment opportunities due to its stable middle class environment -- a key element missing in many other countries listed in the ARDI.

A.T. Kearney notes that retailers looking for scale and volume may not select Gabon as their key market, but Gabon holds immense potential for speciality retailers.

Also developing, Nigeria is often talked about as the country with the most potential for retailers due to its huge population of 178 million, the largest in all of Africa. Nigeria is also growing and urbanizing quickly thus it has developed a rising middle and upper class in part because of its oil-rich economy.

Infographic provided by A.T. Kearney

Despite this, Nigeria places at number four, in part because true spending remains low as the “true middle class” is much smaller when compared to the smaller countries that are ranked higher. Also, Nigeria still poses significant business risks due to high entry barriers and consumers’ requirements in pricing, brand and product origins.

Ghana, which places ninth of the ARDI, has a population of 27 million, half of which live in urban areas. While a small market, Ghana is growing and has a large middle class that is highly unsaturated, leaving ample room for brands looking to fill in product and sector gaps.

Compared to its neighbor Nigeria, Ghana does not have the same business risks as its economy has grown steadily and a number of shopping malls have been built around its capital, Accra.

Although Mozambique places fifteenth on the ARDI, the country is still considered developing because of its infrastructure developments driven by energy sectors such as coal. Mozambique’s mining industry is removed from its urban centers, so the impact is not felt within its main urban cities, but consumer spending per capita growth is slowing and urbanization is not increasing thus stalling the retail sector.

As for the mature nations, Botswana, which places as number two on the ARDI, is often used as an example of a successful economy within Africa because of its strong GDP per capita and stable, well-developed economy driven by mineral mining, agriculture and tourism.

Also, Botswana has a well-developed retail sector including shopping mall developments, with four opening in the past three years.

Overall, South Africa is the most developed economy and retail sector in the Sub-Saharan region. South Africa is a saturated market and one of the best places in African to do business due to relative political stability, well maintained infrastructure, high urbanization rates, ample shopping malls and a developed supply chain.

Additionally, the retail sector in South Africa has been boosted by a significant middle and affluent consumer demographic.

Namibia is the final ARDI country to be ranked as mature. Although Namibia has a small population of approximately 2.3 million people, about 40 percent live in urbanized areas where trade is modernized.

Together with its high GDP per capita of just under $11,000, its affluent population make Namibia ideal for speciality retail and upmarket developments.

In regard to consumers within Sub-Saharan Africa, Mr. Moriarty explained that shoppers can be broken down into four categories.

"Consumers who are outside of the branded fast-moving consumer goods marketplace, who don’t generally buy branded products and don’t shop in organized retail stores…and that’s a lot of the Sub-Saharan Africa consumer base.

"The emerging middle class, who buy some branded beauty care or home care products, and will shop at small-format stores and buy national or regional brands for food." he said. "The solid middle class, mostly urban, who shop at regional or global hyper/super markets, buying local/regional/ global branded healthcare/beauty/food and apparel.

"[And finally,] the super rich, a small proportion in most country markets but a sizable absolute number in markets like Nigeria, who buy branded/luxury products from urban malls or duty free stores."

Developing dimensions Talk of emerging markets dominates the luxury arena’s retail conversation. But, while many retail strategists stress the importance of emerging markets, these regions only comprise about 30 percent of the global luxury market, according to a separate report by A.T. Kearney.

In the 2015 “Global Retail Development Index Ranking,” A.T. Kearney released a special feature, “A Look at Luxury,” to understand the rate at which luxury brands are entering emerging markets. After a challenging 2014, which was marked by low economic growth and political instability in many developing areas, luxury brands have adapted expansion strategies to succeed in diverse and evolving landscapes.

After Asia, the countries in Sub-Saharan Africa yield the highest projected growth rate of UHNW individuals among the GRDI’s top 30, although these consumers are starting at a much lower base. An indicator of Sub-Saharan Africa’s budding affluence is that Nigeria’s Champagne sales are second only after France and Angola is one of the most expensive countries for expats (see story).

"Entering each of the BRICs and additional emerging markets takes a different strategy for each region," Mr. Moriarty said. "Each BRIC country is different from all the others. Brazil is well served, and also quite concentrated in São Paolo. Russia is well served in Moscow and St. Petersburg, and everyone else sort of sucks it up and, of course, the recent anti-Western boycotts have created heartache for brand-builders and Russian consumers alike.

"India is trouble—state regulations and restrictions on foreign direct investment create barriers for retailers and brand-builders alike, though the long history of western companies operating in India have allowed them to create many alternate distribution methods and systems (Hindustan Lever is a good example); China is chugging along—the Chinese consumer likes branded things, and likes shopping," he said. "Logistics has gotten better there, but is still unstable and subject to many bad regulations. Even the recent devaluations won’t deter the government’s intention to build up China’s consumer sector—if anything, it almost proves their commitment.

"On a different note, a pundit once said that India is like Mexico and Sub-Saharan Africa combined—and it is an apt comparison: 100 million developing middle class consumers with a billion out-of-market consumers."

Final Take Jen King, lead reporter on Luxury Daily, New York